Why UK High Earners Face Mounting Tax Pressure

Tax reduction strategies for high income earners UK have become more critical than ever as almost 6.5 million people now pay higher or additional rate tax in 2023/24 – a figure that continues rising year on year. With frozen allowances, reduced thresholds, and the additional rate threshold dropping from £150,000 to £125,140 in April 2023, high earners face what experts call “stealth tax traps” that can push effective rates as high as 60%.

Quick Answer: Top Tax Reduction Strategies for UK High Earners

- Pension contributions – Up to £60,000 annual allowance with potential 60% effective relief

- Salary sacrifice schemes – Reduce both income tax and National Insurance

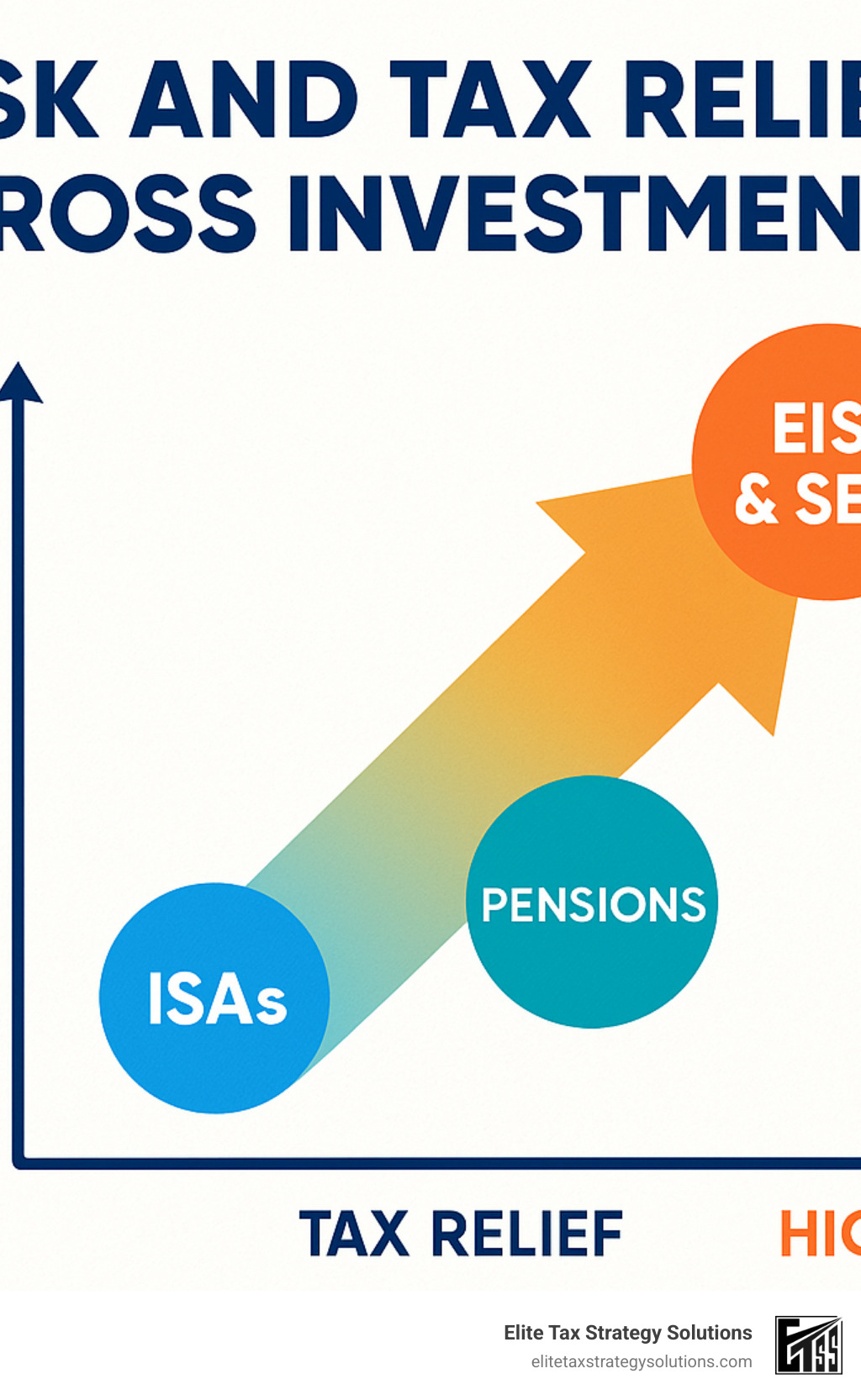

- ISAs – £20,000 annual allowance for tax-free growth

- VCT/EIS/SEIS investments – 30-50% income tax relief on qualifying investments

- Gift Aid donations – Claim higher-rate relief while supporting charity

- Capital gains planning – Use £3,000 allowance and spousal transfers

The challenge isn’t just the headline rates. Between £100,000 and £125,140, you lose £1 of personal allowance for every £2 earned, creating an unofficial 60% marginal rate that catches many off guard. As one financial expert noted: “It’s time to shine the spotlight on a wrinkle in the tax code that catches out a lot of unsuspecting people every year.”

Your situation demands proactive planning. The days of simply accepting higher tax bills are over – strategic action can save tens of thousands annually while building long-term wealth.

I’m David Fritch, and over 40 years of managing my own CPA practice and law firm, I’ve specialized in developing tax reduction strategies for high income earners UK and similar jurisdictions. Through Elite Tax Strategy Solutions, I’ve helped clients with substantial incomes steer complex regulations while maximizing their after-tax wealth through proven, compliant strategies.

Easy tax reduction strategies for high income earners uk word list:

– extra medicare tax for high earners

– tax diversification strategy high income

– tax planning for high salaried employees

The 2024/25 UK High Earner Tax Landscape

If you’re earning a good salary in the UK, you’ve probably noticed your tax bill getting heavier each year. Tax reduction strategies for high income earners UK have become essential because the tax landscape has shifted dramatically against high earners.

Let’s start with the basics. For 2024/25, your personal allowance remains frozen at £12,570 – the same as it’s been since 2021. This might sound stable, but it’s actually a stealth tax increase because inflation has eroded its real value.

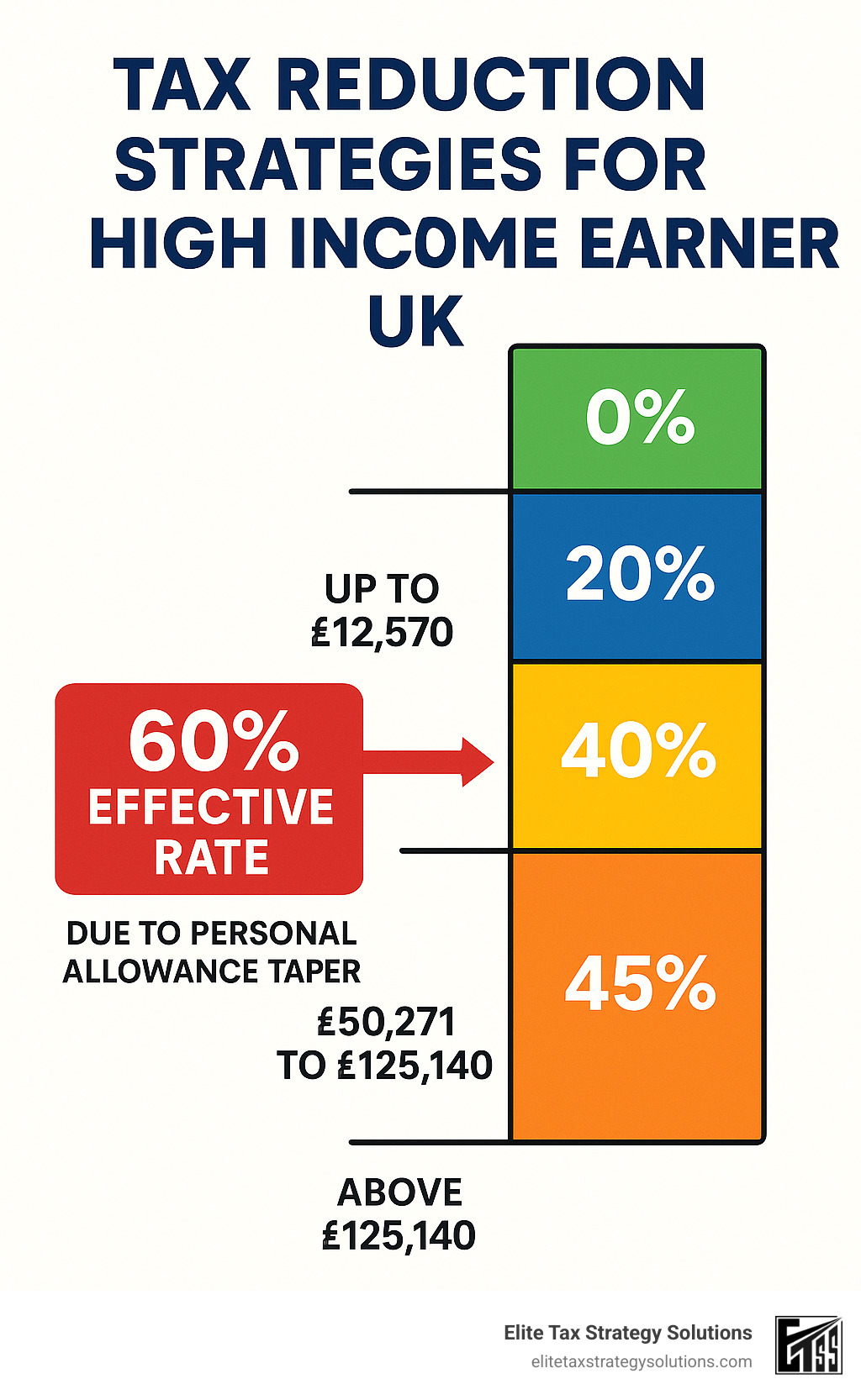

Here’s how the current income tax rates stack up:

| Income Band | Tax Rate | Income Range |

|---|---|---|

| Personal Allowance | 0% | Up to £12,570 |

| Basic Rate | 20% | £12,571 to £50,270 |

| Higher Rate | 40% | £50,271 to £125,140 |

| Effective Rate (60% trap) | 60% | £100,000 to £125,140 |

| Additional Rate | 45% | Above £125,140 |

The numbers tell a stark story. UK income tax receipts have jumped from £193.7 billion in 2020/21 to over £270 billion in 2023/24. That’s not just economic growth – it’s frozen allowances and lower thresholds pulling more people into higher tax bands.

The additional rate threshold dropped from £150,000 to £125,140 in April 2023, creating an even steeper tax cliff. National Insurance adds another layer, with rates of 2% on earnings above £50,270, meaning you’re often paying both higher income tax and National Insurance simultaneously.

But the real shock comes in that middle band between £100,000 and £125,140, where things get genuinely painful.

Understanding the 60% Tax Trap

The 60% tax trap isn’t an official tax rate – it’s an unintended consequence that catches thousands of high earners off guard every year. This effective rate kicks in because of how the personal allowance gets clawed back.

Here’s the brutal math. Let’s say you’re earning £105,000 and get a £1,000 bonus:

You’ll pay 40% tax on that £1,000 bonus, which equals £400. But here’s the kicker – you also lose £500 of your personal allowance (£1 for every £2 earned over £100,000). That lost allowance gets taxed at 40% too, adding another £200 to your bill.

Total tax on your £1,000 bonus: £600. That’s a 60% effective rate.

This trap affects the entire band from £100,000 to £125,140, where your personal allowance gradually disappears. By the time you reach £125,140, you’ve lost your entire personal allowance and face the additional 45% rate on earnings above that threshold.

The impact is significant. Around 792,000 taxpayers now find themselves caught in this band, with many paying an average of £621 extra annually compared to previous thresholds.

Personal Allowance Taper Mechanics

The personal allowance taper operates on what HMRC calls your “adjusted net income” – essentially your total income minus certain deductions like pension contributions and Gift Aid donations. This is where smart planning becomes crucial.

The mechanics are precise: for every £2 of adjusted net income over £100,000, you lose £1 of personal allowance. Your allowance disappears completely when your adjusted net income hits £125,140.

If you’re employed through PAYE, HMRC usually adjusts your tax code automatically to account for this taper. You might notice your tax code changing from 1257L to something much lower, or even becoming a “K code” if you’ve lost your entire allowance.

However, if you have variable income, bonuses, or multiple income sources, you’ll likely need to complete a self-assessment return. This ensures HMRC calculates your tax correctly and allows you to claim back any overpayments.

The good news? Understanding these mechanics is the first step toward implementing effective tax reduction strategies for high income earners UK that can help you avoid or minimize this trap entirely.

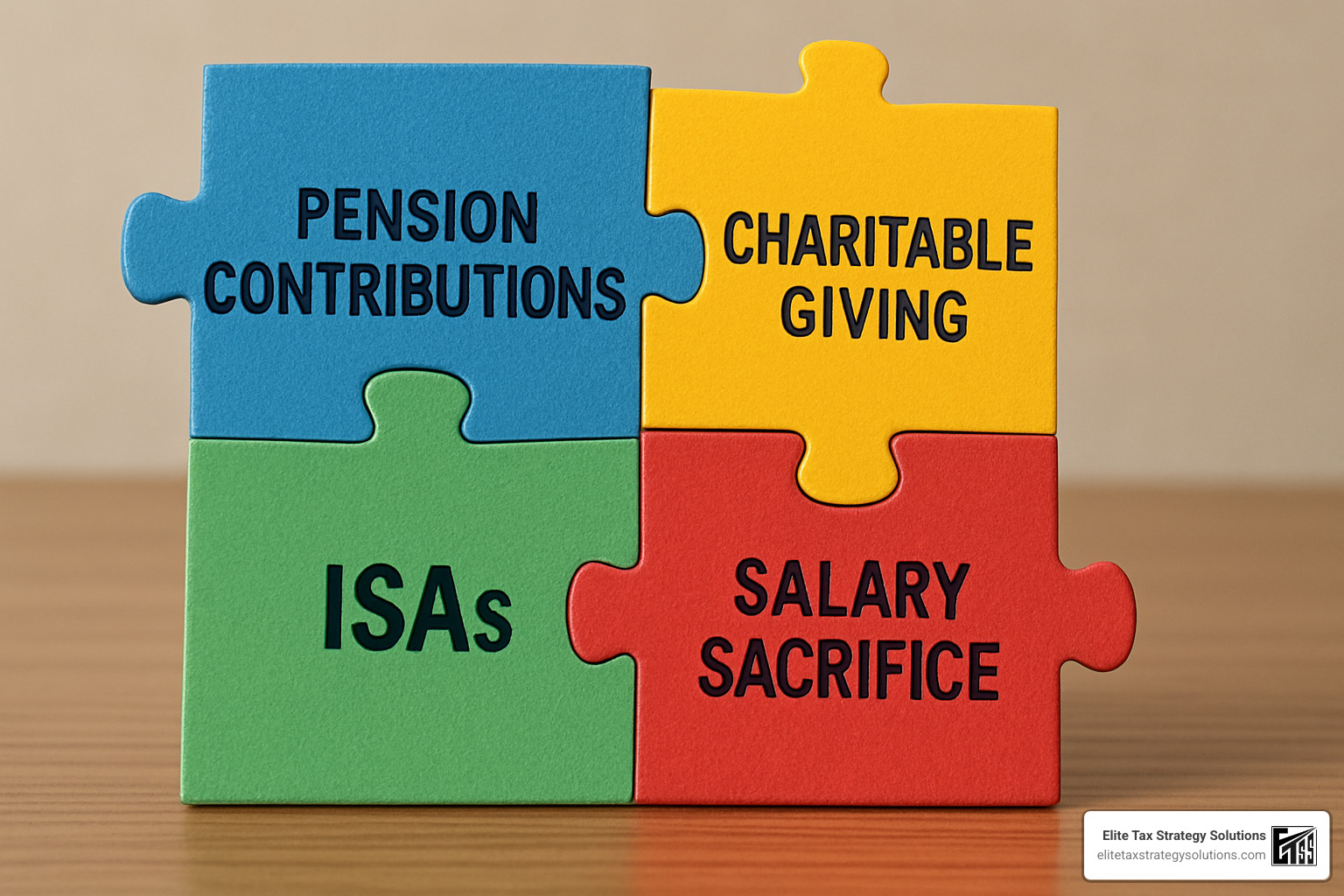

Tax Reduction Strategies for High Income Earners UK

Think of effective tax reduction strategies for high income earners UK like assembling a jigsaw puzzle – each piece works together to create the complete picture. The most successful high earners don’t rely on just one approach. Instead, they combine multiple strategies to create a comprehensive plan that tackles both immediate tax reduction and long-term wealth building.

The beauty lies in how these strategies complement each other. Your pension contributions might reclaim your personal allowance, while salary sacrifice schemes reduce your National Insurance burden. ISAs shelter your investment growth, and charitable giving supports causes you care about while delivering tax relief. When orchestrated properly, these techniques can save you tens of thousands annually.

Let’s explore how each piece fits into your overall Best Tax Saving Strategies for High Income Earners puzzle.

Pension Contributions: Core of tax reduction strategies for high income earners UK

Your pension represents the heavyweight champion of tax reduction strategies. With the annual allowance boosted from £40,000 to £60,000 for 2023/24, you now have even more room to maneuver.

Here’s what makes pensions so powerful: you get immediate tax relief at your marginal rate, whether that’s 20%, 40%, or 45%. But for those caught in the 60% trap between £100,000 and £125,140, pension contributions can effectively restore your personal allowance, delivering what amounts to 60% tax relief.

Let me show you exactly how this works. Imagine you’re earning £110,000 and decide to contribute £20,000 to your pension. Your taxable income drops to £90,000, which brings you back below the £100,000 threshold. Suddenly, you’ve reclaimed your full personal allowance. You receive 40% tax relief on the contribution (£8,000), but the real magic happens when you factor in the restored allowance – your total benefit reaches £12,000, which is effectively 60% relief.

The carry-forward rule adds another layer of opportunity. You can reach back three years to use any unused annual allowances, potentially allowing contributions of up to £200,000 in a single year if you have the unused capacity. This becomes particularly valuable during bonus years or when you’ve had a significant pay rise.

Don’t forget that your pension grows tax-free while you’re building it, and you can take 25% as a tax-free lump sum when you retire. It’s like getting a head start in a race where everyone else begins several steps behind.

For deeper insights into maximizing these benefits, our Tax Planning Strategies for High Income Earners guide explores strategies custom to different income levels.

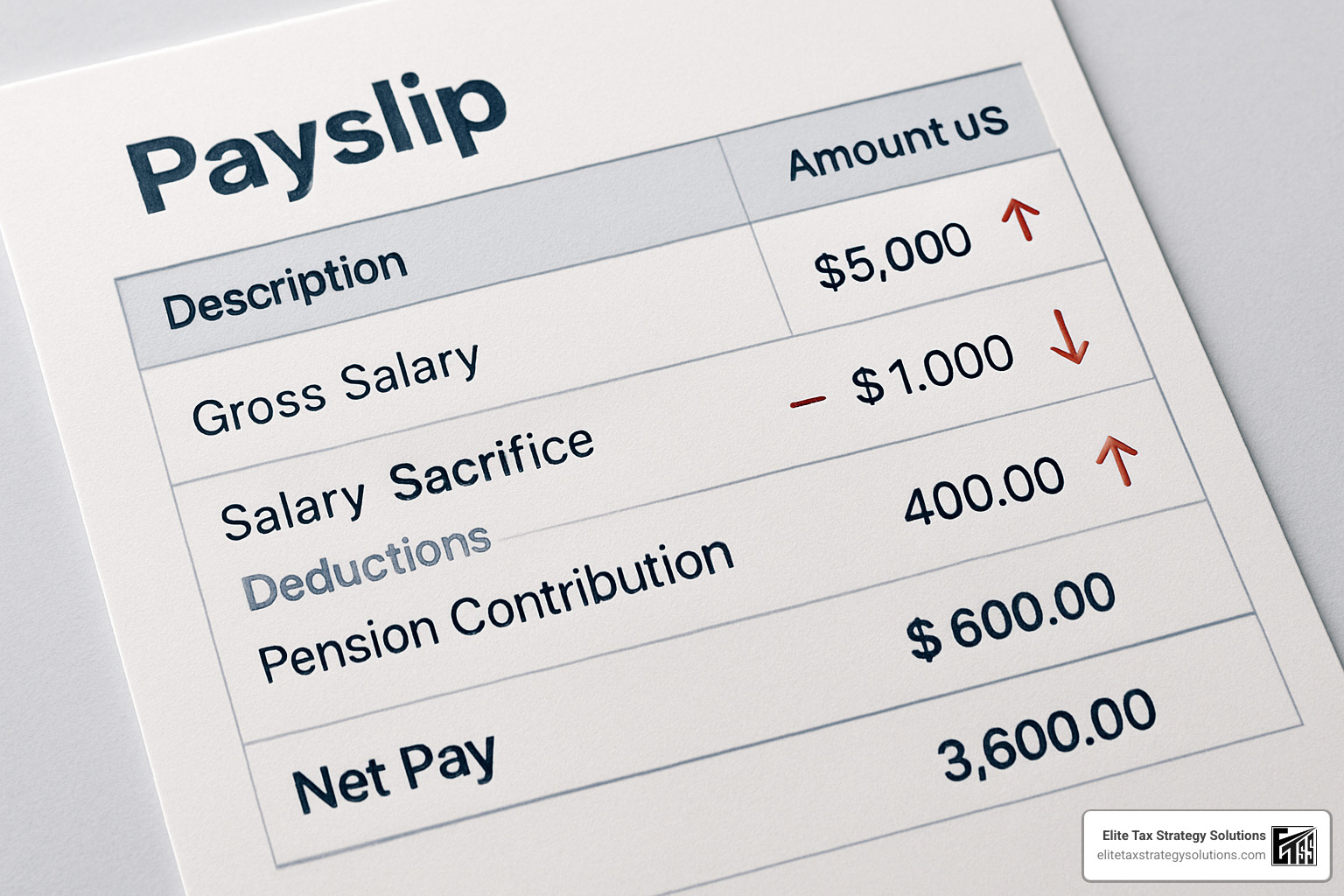

Salary Sacrifice & Benefit Flexing

Salary sacrifice offers something unique – it’s the only strategy that reduces both your income tax and National Insurance contributions. While pension contributions only tackle income tax, salary sacrifice actually reduces your gross salary, creating dual savings that compound your benefits.

The concept is neatly simple. You agree to reduce your salary in exchange for benefits provided by your employer. Popular options include electric vehicles (offering significant tax savings plus environmental benefits), cycle-to-work schemes for bikes up to £1,000, additional pension contributions, and extra annual leave purchased with pre-tax pounds.

What makes this particularly attractive is that both you and your employer save on National Insurance. Many forward-thinking employers share these savings with employees through improved pension contributions or other benefits, creating additional value beyond the immediate tax savings.

However, there’s an important caveat to consider. Salary sacrifice reduces your gross salary for other purposes too – mortgage applications, life insurance calculations, and statutory benefits all use your reduced salary figure. Make sure your new salary level still supports your financial commitments before diving in.

The key is finding the right balance. Our Tax Diversification Strategy for High Income guide shows you how to weave salary sacrifice into your broader income optimization strategy without creating unintended consequences.

ISAs & Investments: diversified tax reduction strategies for high income earners UK

Don’t underestimate the humble ISA. While the £20,000 annual allowance might seem modest compared to pension limits, ISAs offer something pensions can’t – complete flexibility. You can access your money anytime without penalties, restrictions, or tax implications.

Think of ISAs as your financial Swiss Army knife. They provide complete tax-free growth on capital gains and dividends, have no lifetime limits (meaning you can build substantial wealth over time), and offer inheritance benefits where surviving spouses can inherit additional ISA allowances.

A game-changing update from April 2024 allows you to contribute to multiple ISAs of the same type within a single tax year. This flexibility makes it easier to diversify across different providers and investment strategies without the previous restrictions.

For higher-rate taxpayers, stocks and shares ISAs typically deliver more value than cash ISAs because they shelter dividend income that would otherwise face punishing tax rates of 33.75% (higher rate) or 39.35% (additional rate). With the dividend allowance slashed to just £500 for 2024/25, ISAs quickly become essential for any dividend-generating investments.

Consider exploring Innovative Finance ISAs for peer-to-peer lending and alternative investments, though remember these carry higher risks and should represent only a small portion of your overall portfolio.

High-Risk, High-Reward: VCTs, EIS & SEIS

For those comfortable with higher risk, government-backed investment schemes offer some of the most generous tax incentives available. These aren’t for everyone, but they can be incredibly powerful when used strategically.

Venture Capital Trusts (VCTs) provide 30% income tax relief on investments up to £200,000 annually, plus tax-free dividends and no capital gains tax on disposal. The catch? You must hold the shares for five years to retain the reliefs.

Enterprise Investment Scheme (EIS) steps things up with 30% income tax relief on investments up to £1 million annually (£2 million for knowledge-intensive companies). But here’s where it gets interesting – EIS also offers capital gains tax deferral on existing gains and loss relief if investments fail. It’s like having a safety net while reaching for higher returns.

Seed Enterprise Investment Scheme (SEIS) offers the most generous relief at 50% on investments up to £200,000 annually, though with correspondingly higher risks as you’re investing in very early-stage companies.

These schemes work particularly well in combination with other strategies. You could realize capital gains to fund EIS investments, deferring the gains tax while claiming income tax relief – essentially getting paid by the tax system to diversify your portfolio.

But let’s be honest about the risks. Many early-stage companies fail, and your capital is genuinely at risk. These investments should complement a diversified portfolio, not replace it. Our Tax Efficient Investments guide provides detailed frameworks for assessing these risks.

The GCV guide to tax-efficient investing offers additional insights into structuring these investments effectively.

Charitable Giving & Gift Aid

Charitable giving through Gift Aid creates a rare win-win-win situation. You support causes you care about, the charity receives extra funding, and you get tax relief. It’s one of the few strategies where doing good genuinely pays.

Here’s how the magic works: when you donate through Gift Aid, the charity receives an extra 25% from the government as basic rate relief. But as a higher-rate taxpayer, you can claim back the difference between your tax rate and the basic rate.

Let’s make this concrete. If you make a £100 Gift Aid donation as a higher-rate taxpayer, it actually costs you £75 after claiming £25 relief, but the charity receives £125 (your £100 plus the government’s £25 top-up). Additional-rate taxpayers can reclaim even more – 31.25% of their donation.

The carry-back option adds strategic flexibility. You can allocate donations to the previous tax year, which proves invaluable for tax planning around variable income or particularly good years.

There’s even an inheritance tax angle. Charitable gifts are exempt from IHT, and if you leave at least 10% of your estate to charity, the IHT rate reduces from 40% to 36% on the rest.

For detailed guidance on claiming Gift Aid relief, the official information can be found here.

Capital Gains & Dividend Allowance Tactics

With the capital gains tax annual exemption slashed to just £3,000 for 2024/25 and the dividend allowance cut to £500, every pound of these allowances becomes precious. The key is making sure neither goes to waste.

For capital gains planning, focus on using your annual allowance by realizing £3,000 of gains each year, even if you’re not selling permanently. Spousal transfers let you use both allowances, while bed and ISA strategies involve selling investments to realize gains, then repurchasing within ISAs for future tax-free growth.

Dividend planning requires similar precision. Hold dividend-paying investments within ISAs where possible, ensure both spouses use their £500 allowances, and consider the timing of dividend payments around the tax year-end.

The dramatic reduction in these allowances makes tax-free wrappers like ISAs and pensions even more valuable. What once seemed like generous allowances now require careful planning to maximize their benefit.

Avoiding Hidden Charges & Cliffs

High earners face numerous “cliff edges” where small increases in income trigger disproportionate tax increases or benefit losses. Understanding and avoiding these traps is crucial for effective tax planning. Our Tax Optimization Strategies provide comprehensive guidance on navigating these complex thresholds.

Mitigate High Income Child Benefit Charge

The High Income Child Benefit Charge creates a particularly harsh cliff edge for families. Child Benefit is gradually withdrawn when the highest earner’s adjusted net income exceeds £60,000, disappearing entirely at £80,000.

For a family with two children receiving £1,934 annually in Child Benefit:

– At £60,000 income: Full benefit retained

– At £70,000 income: 50% of benefit clawed back (£967)

– At £80,000 income: 100% of benefit clawed back (£1,934)

The effective marginal tax rate in this band can exceed 50% when combined with higher-rate tax. However, pension contributions can reduce your adjusted net income below the £60,000 threshold, preserving the full benefit.

Pension Taper & Annual Allowance Pitfalls

High earners with income over £260,000 face a tapered annual allowance that reduces from £60,000 to as little as £10,000. This taper operates on “threshold income” and “adjusted income,” creating complex calculations that can catch unwary taxpayers.

The taper reduces the annual allowance by £1 for every £2 of adjusted income over £260,000. This means:

– At £260,000: Full £60,000 allowance

– At £310,000: £35,000 allowance

– At £360,000: £10,000 minimum allowance

Employer contributions count toward these limits, so high earners with generous employer pension schemes need careful monitoring to avoid annual allowance charges.

Loss of Savings & Dividend Allowances

Higher-rate taxpayers lose their personal savings allowance (reduced to £500) and face higher tax rates on dividend income. The starting rate for savings (0% on up to £5,000 of savings income) is also unavailable to higher-rate taxpayers.

This makes tax-efficient wrappers even more valuable for protecting savings and investment income from tax.

Advanced Planning, Risk Management & Professional Advice

When your income reaches six figures, tax planning stops being a once-a-year exercise and becomes an ongoing strategy that requires careful coordination. The difference between good planning and great planning can literally save you tens of thousands of pounds annually. But here’s the thing – advanced tax reduction strategies for high income earners UK often involve timing, risk assessment, and sophisticated techniques that benefit enormously from professional guidance.

Think of it this way: you wouldn’t perform surgery on yourself, even if you’d read all the medical textbooks. Tax planning at high income levels involves similar complexity and precision. Our Advanced Tax Strategies are designed specifically for these nuanced situations.

Using Carry Forward & Timing Income

The pension carry-forward rules create some of the most powerful opportunities for high earners, especially when your income varies significantly from year to year. You can reach back three years and use any unused annual allowances, which means in the right circumstances, you could contribute up to £200,000 in a single year.

This becomes particularly valuable during bonus years when a large payment pushes you deep into higher tax brackets. Rather than watching HMRC take 40% or even 60% of that bonus, you can shelter significant portions through strategic pension contributions. I’ve seen clients save £30,000 or more in tax on a single large bonus using this approach.

Share option exercises present another golden opportunity. When options vest, they often create substantial taxable income in one go. By using carry-forward allowances, you can smooth this income over multiple years from a tax perspective, dramatically reducing the overall tax burden.

The key is aligning your pension contributions with income spikes rather than spreading them evenly. Sometimes deferring bonuses to the following tax year makes sense, especially if it keeps you below certain thresholds or allows time to organize larger pension contributions.

Assessing Risk in EIS/VCT/SEIS

Let’s be honest about EIS, VCT, and SEIS investments – they offer fantastic tax reliefs, but they’re not for everyone. The 30% to 50% income tax relief can look incredibly attractive when you’re facing a large tax bill, but these investments come with real risks that can wipe out those tax savings and more.

High failure rates are simply part of the territory with early-stage companies. Statistics show that a significant percentage of start-ups fail within five years. You’re essentially betting on companies that may not even exist in a few years’ time.

Liquidity constraints mean your money is tied up for several years minimum. Unlike stocks and shares that you can sell tomorrow if needed, EIS and VCT investments require patience and the ability to leave that money untouched.

The concentration risk also deserves serious consideration. Even well-diversified EIS funds typically hold fewer companies than a traditional investment portfolio. If a particular sector hits trouble, it can impact multiple holdings simultaneously.

That said, these investments can work brilliantly as part of a balanced approach. The key is treating them as exactly what they are – high-risk investments that happen to have tax benefits, not tax shelters that happen to be investments. Most financial advisers recommend limiting these to 5-10% of your total investment portfolio.

When to Seek Specialist Advice

There comes a point where DIY tax planning reaches its limits. Career changes often trigger this need – moving from employment to self-employment, joining a company with complex share schemes, or relocating internationally all create situations where specialist knowledge becomes invaluable.

HMRC enquiries definitely fall into the “get professional help immediately” category. While most enquiries are routine, having experienced representation can mean the difference between a quick resolution and a lengthy, stressful investigation.

Complex investment decisions involving large capital gains, business disposals, or international portfolios also benefit from specialist input. The interaction between different taxes and reliefs can create unexpected outcomes that only experienced professionals spot.

At Elite Tax Strategy Solutions, we’ve learned that the most successful tax planning happens when clients engage with professionals proactively, not reactively. Regular reviews ensure you’re always positioned optimally for changing circumstances and new opportunities.

As experts note in their analysis on How you can beat the 60% tax trap, the UK tax system’s complexity means professional guidance often pays for itself many times over through the opportunities and pitfalls it helps you identify.

The goal isn’t just to minimize this year’s tax bill – it’s to build a comprehensive strategy that optimizes your financial position for decades to come.

Frequently Asked Questions about High-Earner Tax Planning

Let’s address the most common questions I hear from clients about tax reduction strategies for high income earners UK. These are the concerns that keep high earners awake at night – and the answers that help them sleep better.

What income triggers the 60% tax trap?

The dreaded 60% effective tax rate kicks in when your income hits £100,000 and continues until you reach £125,140. It’s like a hidden tax landmine that catches many successful professionals completely off guard.

Here’s what actually happens: for every £2 you earn above £100,000, you lose £1 of your personal allowance while still paying 40% tax on that extra income. The math is brutal – you’re effectively paying 60% tax on every pound in this band.

Think of it this way: if you get a £1,000 bonus when you’re earning £110,000, you’ll pay £400 in income tax on the bonus itself, plus another £200 when your reduced personal allowance gets taxed. That’s £600 out of your £1,000 – a 60% hit.

The good news? This trap is completely avoidable with the right planning. Pension contributions are your best friend here, as they can pull your income back below £100,000 and restore your full personal allowance.

How much can I safely contribute to my pension each year?

For 2024/25, you can contribute up to £60,000 annually or 100% of your UK earnings – whichever is lower. But there’s a catch if you’re a very high earner.

If your income exceeds £260,000, the annual allowance starts shrinking. It reduces by £1 for every £2 of income above this threshold, bottoming out at just £10,000 when your income hits £360,000. This taper can catch high earners by surprise, especially those with generous employer pension schemes.

The carry-forward rule adds real power to your planning. You can sweep up unused allowances from the previous three tax years, potentially allowing contributions of £200,000 or more in a single year if you have sufficient earnings and unused allowances.

I often see clients use this strategically during bonus years or when exercising share options. The key is having professional guidance to ensure you don’t accidentally breach the rules and trigger penalty charges.

Are VCTs and EIS worth the risk for tax savings?

This is where the conversation gets interesting – and where many people get seduced by the impressive tax relief numbers without fully understanding what they’re signing up for.

VCTs offer 30% income tax relief and tax-free dividends, while EIS can provide 30% relief (sometimes 50% for SEIS) plus capital gains deferral. On paper, these look fantastic. In reality, they’re high-risk investments in early-stage companies where failure rates are significant.

I tell my clients to think of these investments as “tax relief with a side of venture capital” rather than the other way around. The tax benefits are real, but you could lose your entire investment if the underlying companies fail.

My rule of thumb? These should represent no more than 5-10% of your total investment portfolio, and only after you’ve maximized safer options like pensions and ISAs. You should be comfortable losing every penny you invest – if that thought makes you uncomfortable, stick to the safer strategies.

The sweet spot is often for clients who’ve already maxed out their pension contributions and ISAs, have emergency funds sorted, and genuinely want exposure to early-stage British businesses. The tax relief then becomes a nice bonus rather than the primary motivation.

Conclusion & Your Next Step

The journey through tax reduction strategies for high income earners UK reveals a landscape that’s both challenging and full of opportunity. Yes, you’re facing stealth taxes, frozen allowances, and that brutal 60% trap between £100,000 and £125,140. But you’re also equipped with powerful tools to fight back.

The most successful high earners don’t rely on just one strategy. They weave together pension contributions that can deliver 60% effective relief, salary sacrifice schemes that slash both income tax and National Insurance, and ISAs that shelter £20,000 annually from the taxman’s reach. For those comfortable with higher risk, VCT and EIS investments can provide 30-50% upfront relief, while Gift Aid donations let you support causes you care about while reducing your tax bill.

But here’s the thing – the UK tax system never stands still. What saved you thousands last year might not work this year. The additional rate threshold dropped from £150,000 to £125,140 with little fanfare. Allowances keep shrinking. New cliff edges appear seemingly overnight.

This isn’t a “set it and forget it” situation. Your tax strategy needs regular attention, just like your investment portfolio or your career development. The most expensive mistake high earners make? Assuming their accountant will handle everything. Most accountants are excellent at compliance but don’t specialize in proactive tax optimization for complex situations.

At Elite Tax Strategy Solutions, we’ve built our practice around one simple truth: high earners need specialized expertise. Over four decades, I’ve seen too many successful professionals hand over massive tax bills that could have been avoided with proper planning. Our approach goes beyond basic compliance – we create comprehensive strategies that align with your career trajectory, investment goals, and family circumstances.

The mathematics are compelling. If you’re earning £120,000 and implementing just the core strategies we’ve discussed, you could easily save £10,000-£15,000 annually. Over a decade, that’s £100,000-£150,000 staying in your pocket instead of going to HMRC. Add in the compound growth on those savings, and you’re looking at a substantial difference in your long-term wealth.

The window for action is now. Tax planning works best when you implement strategies before you need them, not after your accountant presents you with a shocking tax bill. The earlier in the tax year you start, the more options you have.

Ready to take control of your tax situation? Elite Tax Strategy Solutions offers comprehensive reviews that examine every aspect of your financial picture. We don’t just look at this year – we plan for your entire financial journey. Our expertise in Innovative Tax Planning means you’ll always be ahead of the curve, not scrambling to catch up.

Your success deserves a tax strategy that matches your ambition. Don’t let another year pass watching your hard-earned income disappear into avoidable tax bills. The best time to start optimizing your tax position was yesterday. The second-best time is today.