Why Tax Diversification Strategy High Income Matters

Tax diversification strategy high income is about strategically spreading your investments across different types of accounts to minimize taxes over your lifetime, particularly as a high earner.

Here’s what you need to know at a glance:

- Definition: Allocating assets into taxable, tax-deferred, and tax-free accounts.

- Purpose: Reduce tax burden, increase flexibility, and manage liabilities efficiently.

- Main Components:

- Taxable Accounts: Provide liquidity, subject to annual taxes.

- Tax-Deferred Accounts: Contributions deducted now, but taxed at withdrawal.

- Tax-Free Accounts: Contributions taxed today, tax-free growth and withdrawals.

As high-income earners, taxes significantly impact your wealth—but smart tax diversification can meaningfully reduce this burden, giving you greater flexibility to control future financial outcomes.

I’m David Fritch, and with over 40 years running my own law firm and CPA practice, I’ve helped countless high earners steer complex financial landscapes. Leveraging my experience with tax diversification strategy high income, I guide clients toward maximizing their tax savings and securing long-term financial stability.

Common tax diversification strategy high income vocab:

– advanced tax planning strategies

– wealth management tax planning

– tax planning strategies for high income earners

Understanding Tax Diversification Strategy for High-Income Earners

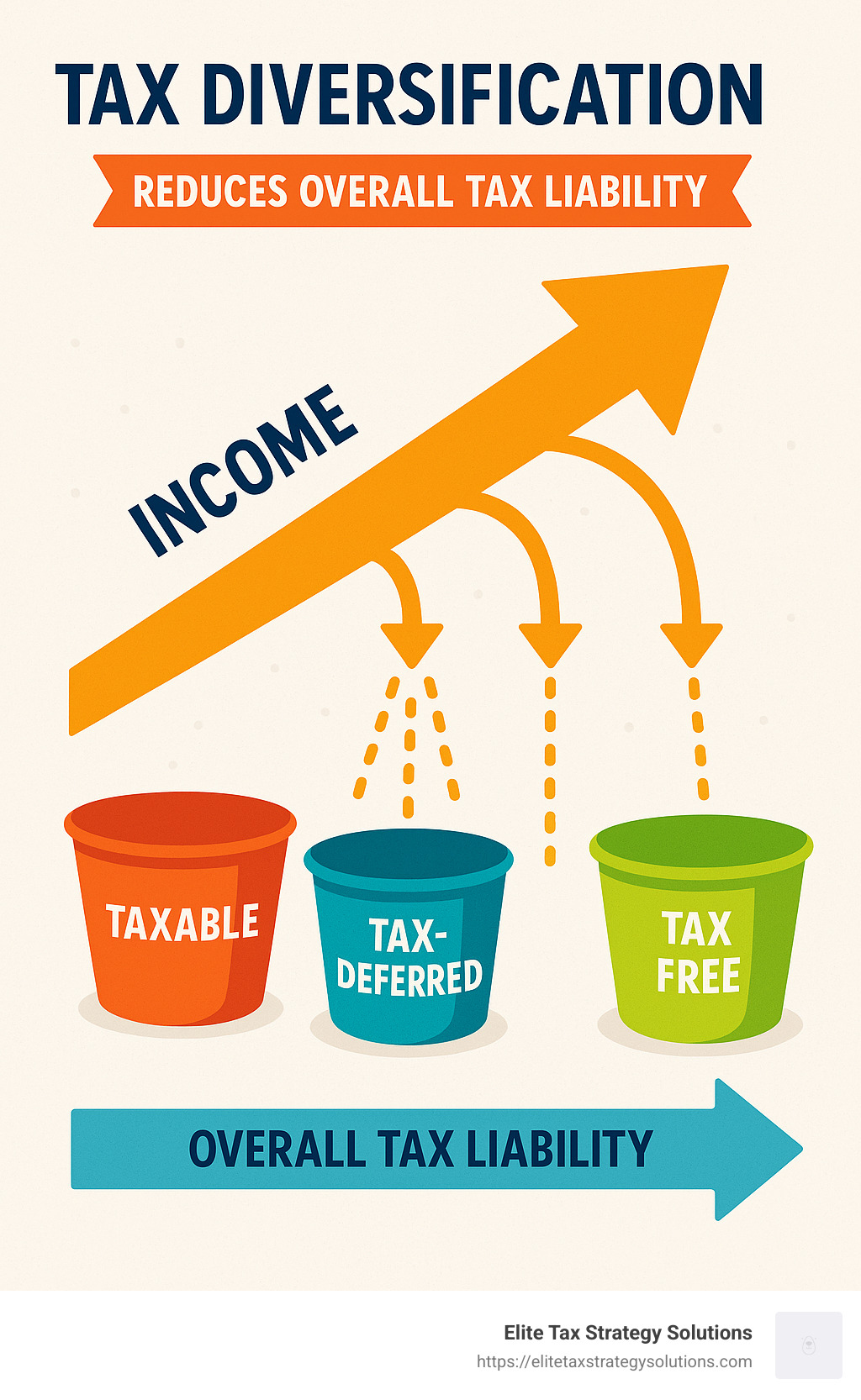

When we talk about a tax diversification strategy high income, we’re really discussing a thoughtful approach to spreading your investments across different types of accounts—each treated differently by the tax code. If you’re a high-income professional, this isn’t just a “nice-to-have”; it’s a must-have tool to avoid getting hammered by progressive tax brackets and losing valuable deductions to phase-outs.

Think of tax diversification as applying the old saying, “Don’t put all your eggs in one basket,” to your tax situation instead of just your investments. We’re all pretty familiar with the idea of diversifying investments among stocks, bonds, real estate—you name it. But smart tax diversification means balancing your money across accounts taxed differently. This mix helps you keep your tax bill lower and gives you more choice and flexibility when it’s time to withdraw your funds.

Tax diversification isn’t simply about cutting your tax bill this year. Instead, it’s about playing the long game—optimizing your overall taxes across your entire lifetime. As a high-income earner, your tax rate might be sky-high right now, but your retirement years could look very different. By planning ahead, you gain flexibility, so you only pay your fair share—and not a cent more.

Tax Diversification vs. Traditional Asset Diversification

At this point, you might wonder, “How is tax diversification different from regular asset diversification?” Glad you asked!

Traditional asset diversification is about managing your investment risk. You spread your money across different kinds of investments—stocks, bonds, real estate—to keep your portfolio balanced and stable. It’s measured by things like portfolio volatility, and you’re aiming to avoid massive swings in value.

But tax diversification? That’s about managing your tax liability. Instead of worrying about investment types, you’re looking at how your money is taxed. You spread your wealth across taxable, tax-deferred, and tax-free accounts like brokerage accounts, 401(k)s, and Roth IRAs. This strategy is measured by your after-tax returns—because when it comes down to it, it’s not just about what you make, but about what you keep.

Here’s an easy comparison to clear things up:

| Traditional Asset Diversification | Tax Diversification |

|---|---|

| Spreads investments across asset classes (stocks, bonds, real estate) | Spreads investments across different tax treatments (taxable, tax-deferred, tax-free accounts) |

| Main goal: Protect against investment risk | Main goal: Reduce your lifetime tax bill |

| Evaluated using portfolio volatility | Evaluated by your after-tax income |

Done right, a solid tax diversification strategy high income can save high earners as much as 20% in lifetime taxes. Pretty significant, right?

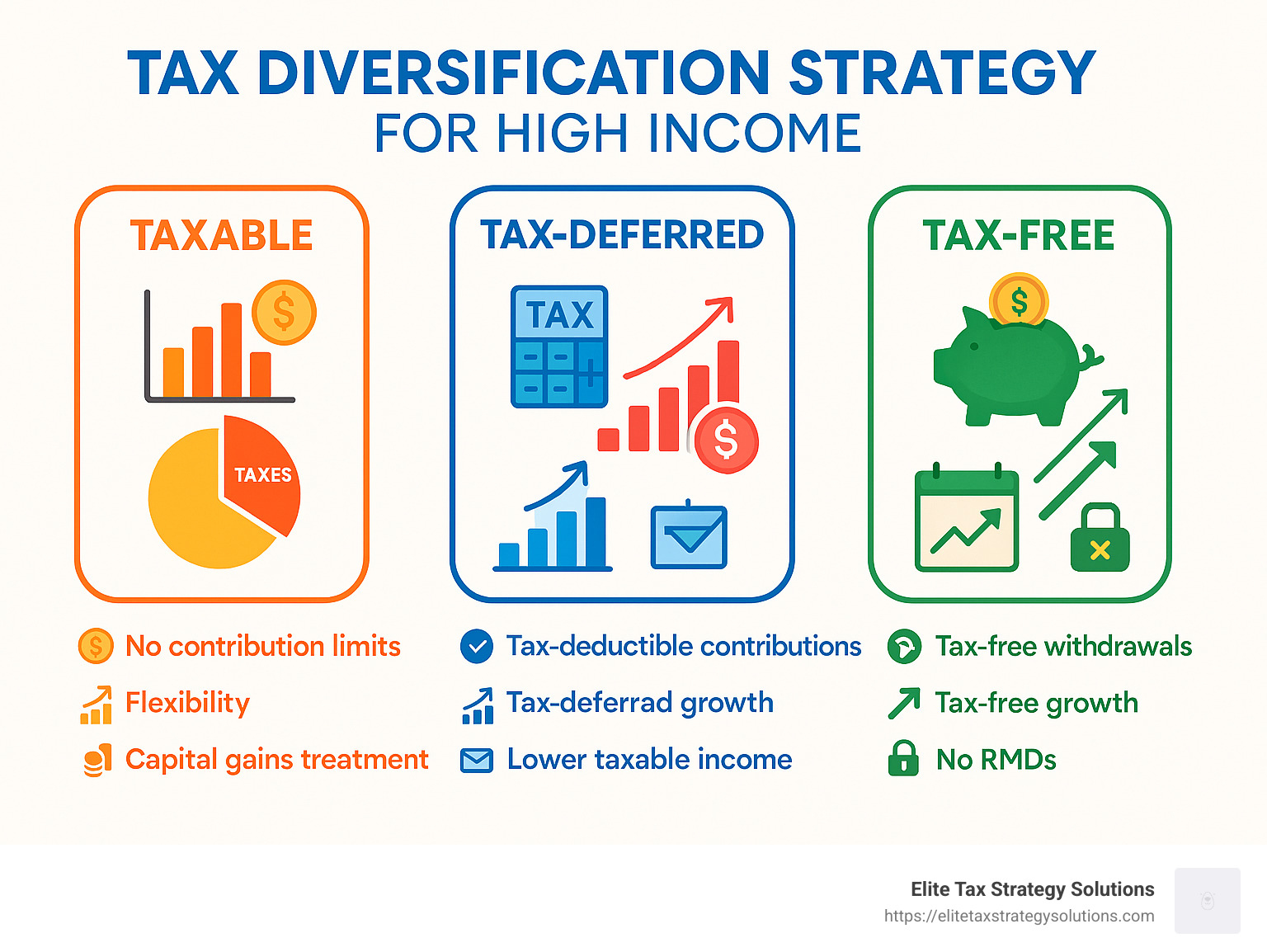

The Three Tax Buckets in Tax Diversification Strategy High Income

To build a well-rounded tax diversification plan, you need to familiarize yourself with three key “tax buckets”: taxable, tax-deferred, and tax-free accounts. Let’s take a closer look at each one.

Taxable accounts are the standard brokerage and investment accounts you open with after-tax dollars. You’ll pay taxes each year on dividends, interest, and capital gains—but the good news is these accounts give you maximum flexibility. They have no early withdrawal penalties, and you can dip into them anytime, at any age. Examples include brokerage accounts, bank accounts, and money market funds. Taxable accounts provide great liquidity and opportunities to jump on investment opportunities without restrictions.

Next up are tax-deferred accounts—like your traditional 401(k), IRA, or SEP IRA. Contributions here reduce your current taxable income, giving you an immediate tax deduction. These accounts grow tax-free, but withdrawals in retirement are taxed as ordinary income. There are some strings attached: withdrawals before age 59½ usually come with penalties, and you’re required to start taking minimum distributions (RMDs) at age 73. Despite those limitations, tax-deferred accounts are powerful tools for compounding your wealth without the drag of annual taxes.

Finally, we have tax-free accounts such as Roth IRAs, Roth 401(k)s, and Health Savings Accounts (HSAs). You fund these with after-tax money—meaning you pay taxes now—but once funded, your money grows and can be withdrawn completely tax-free in retirement. No income tax surprises down the road! Some accounts have income limits or require you to hold funds for a certain number of years to enjoy those tax-free withdrawals. Still, they’re incredibly valuable for high earners looking to minimize their future tax burden.

As financial advisors love to say, “It’s not just what you earn, it’s what you keep.” Tax-free accounts like Roth IRAs or certain life insurance policies let you keep more of your money when it counts—in retirement.

By thoughtfully mixing taxable, tax-deferred, and tax-free accounts, your tax diversification strategy high income gives you incredible flexibility. You gain more control over your future taxes, protect your wealth, and position yourself for maximum financial security and stability.

To learn more, explore our page on advanced tax planning strategies designed specifically for high-income individuals.

Benefits of Tax Diversification for High Earners

Let’s face it, as a high-income earner, taxes can significantly eat away at your hard-earned wealth. With federal tax rates topping out at 37% (and that’s before state taxes!), managing your tax liability is crucial. This is precisely why a smart tax diversification strategy high income is so valuable—it allows you to keep more of what you earn and grow your wealth more efficiently.

One of the standout advantages is potential tax savings. By strategically placing your investments into taxable, tax-deferred, and tax-free accounts, you can greatly reduce your lifetime tax bill. For example, studies have shown that thoughtful tax diversification can extend the lifespan of your retirement portfolio by more than 10% simply by optimizing withdrawals. To put that into perspective, a married couple planning for $150,000 a year in retirement income could potentially lower their federal tax bill by over $11,000 annually just by diversifying their account types. That’s extra money to fund your passions, travel with loved ones, or spoil your grandkids (you know they deserve it!).

Another compelling benefit is the flexibility in retirement withdrawals. Imagine being able to carefully choose which account you’re pulling money from each year, picking the most tax-efficient bucket available. When tax laws change—and let’s be honest, they always do—you have the freedom to adjust your withdrawal strategy accordingly. As one of our clients recently said, “Having different account types gives me the freedom to control my tax situation year by year, rather than being at the mercy of whatever the tax code happens to be when I retire.” Smart move, right?

Additionally, tax diversification provides a valuable form of risk mitigation against future tax law changes. Think of it as your personal tax insurance policy. If taxes go up significantly in the future, you’ll be thankful for those tax-free accounts like Roth IRAs. On the flip side, if tax rates decrease, your tax-deferred accounts will become even more attractive. This ability to adapt to tax changes is especially critical for high earners.

Managing Tax Liabilities Through Tax Diversification Strategy High Income

A thoughtfully crafted tax diversification strategy high income also empowers you to proactively manage your taxes during your highest earning years. When your income peaks, you can significantly reduce your current taxable income by maximizing contributions to tax-deferred accounts, such as Traditional 401(k)s or IRAs. For example, the IRS adjusts 401(k) contribution limits each year, allowing individuals under age 50 to typically set aside tens of thousands of dollars into a Traditional 401(k). Meanwhile, those over 50 can contribute even more with additional “catch-up” amounts. This approach directly lowers today’s tax burden.

At the same time, you can build taxable accounts for liquidity and potential long-term capital gains advantages, as well as use “backdoor Roth” strategies to grow your tax-free assets, even if your income exceeds the thresholds.

When retirement arrives, these diversified accounts shine even brighter. Let’s say you have a year with lower income—it’s the perfect opportunity for Roth conversions or harvesting capital gains at favorable rates. In higher-income years, you might prefer tapping tax-free Roth accounts to avoid pushing yourself into higher tax brackets. Balancing your withdrawals among different account types gives you greater control and keeps your tax bill manageable year after year.

In fact, research on tax-efficient retirement withdrawals confirms that drawing proportionally across taxable, tax-deferred, and tax-free accounts can significantly extend your portfolio’s longevity, compared to a more rigid withdrawal method.

Bottom line? A solid tax diversification strategy doesn’t just help you save money—it provides peace of mind, flexibility, and the ability to adapt to whatever the tax world throws at you next. With proactive planning, you can take charge of your financial future and keep more of your wealth exactly where it belongs—in your hands.

Implementing Tax Diversification Strategies

Implementing a tax diversification strategy high income is a bit like preparing a delicious meal—you need the right ingredients, careful planning, and thoughtful timing to make it truly enjoyable (especially when Uncle Sam joins the table). Let’s walk through how to bring this powerful tax planning strategy into action.

Balancing Contributions Across Accounts

The first step toward effective tax diversification is understanding your income and tax situation—both current and projected. Carefully assess your current marginal tax rate to determine how additional contributions or deductions impact your tax liability now. Then, consider your anticipated future tax situation in retirement—will your tax bracket remain similar, go up, or perhaps drop significantly?

With these factors in mind, prioritize your contributions thoughtfully:

- If you anticipate being in a lower tax bracket later, then it’s smart to prioritize contributions to tax-deferred accounts like Traditional 401(k)s or IRAs. You get immediate tax savings today and the chance to withdraw money at lower rates down the road.

- Expecting your tax bracket to stay high in retirement? Then you might want to lean more toward tax-free accounts such as Roth IRAs or Roth 401(k)s. You pay taxes today but benefit from tax-free growth and withdrawals later—when your tax rate might otherwise sting more.

- Always take full advantage of employer matches on retirement plans—think of this as “free money,” and nobody says no to free money, right?

Regardless of future tax brackets, it’s a wise move for high earners to also build a comfortable cushion in a taxable brokerage account. This provides liquidity, flexibility for emergencies or opportunities, and potential long-term capital gains treatment.

Here’s how a balanced approach might look in practice: contribute enough to your 401(k) to secure your full employer match, max out a Health Savings Account (HSA) if eligible (they offer a triple tax advantage!), leverage a backdoor Roth IRA if your income is too high for traditional contributions, and allocate additional savings to a taxable account, investing in tax-efficient assets.

Roth Conversions as Part of a Tax Diversification Strategy

One of the most powerful moves in your tax diversification strategy high income playbook is the Roth conversion. A Roth conversion involves transferring money from tax-deferred accounts (like traditional IRAs or 401(k)s) into Roth accounts, paying taxes now in exchange for tax-free growth and future withdrawals.

As one tax planning expert wisely said,

“High-income earners can benefit from Roth conversions during lower-income years to reduce future tax liabilities by up to 30%.”

Timing really matters here. Look for strategic opportunities to perform Roth conversions during lower-income years—perhaps between jobs, during early retirement, or when your business income takes a temporary dip. By converting just enough to keep yourself within your current (and ideally lower) tax bracket, you lock in savings and reduce your future tax burden significantly.

Another savvy trick is to perform Roth conversions during market downturns. Converting funds when account values have dropped allows you to transfer more shares at a lower taxable value. When the market rebounds (and it always eventually does), those gains grow tax-free in your Roth account.

At Elite Tax Strategy Solutions, we frequently help our clients identify these key opportunities and implement smart Advanced Tax Strategies like Roth conversion ladders. This proactive approach can be transformative over the long-term, significantly reducing your lifetime tax liability.

Utilizing Taxable, Tax-Deferred, and Tax-Free Accounts

Each account “bucket” has its own unique role within your tax diversification strategy high income—it’s all about using each one strategically to your advantage.

Tax-deferred accounts (like Traditional IRAs or 401(k)s) are your immediate tax-savings friends. They’re ideal for reducing current-year taxable income, especially during peak earning years. Typically, income-producing investments such as bonds or real estate funds—assets generating lots of current taxable income—fit nicely in these accounts. In retirement, withdrawing from tax-deferred accounts first can help fill up lower tax brackets strategically.

On the other hand, tax-free accounts (like Roth IRAs, Roth 401(k)s, and HSAs) are your long-term growth allies. Because these accounts provide tax-free growth and withdrawals, they’re ideal for investments with the highest potential appreciation—think growth stocks or equity ETFs. When retirement comes around, these accounts become particularly valuable in high-income years, helping you avoid jumping into higher tax brackets.

Finally, taxable brokerage accounts offer flexibility and liquidity. They’re perfect for tax-efficient investments like index ETFs, municipal bonds, or long-term buy-and-hold stocks. In retirement, you can employ smart strategies like tax-loss harvesting or taking advantage of lower long-term capital gains rates to keep your taxes manageable.

Imagine withdrawing $250,000 during retirement. If all of it came from a 401(k), you’d end up with around $187,500 after tax (assuming a 25% rate). But if you diversified your withdrawals—taking $125,000 from your 401(k), $75,000 from a taxable account, and $50,000 from a Roth IRA—your after-tax total could jump to approximately $207,500! That’s an extra $20,000 in your pocket, simply by diversifying your account types.

Implementing a thoughtful, proactive tax diversification strategy high income involves understanding your current situation, projecting your future needs, and taking strategic action today. It may seem complex at first, but the payoff—in lower lifetime taxes and greater financial freedom—is definitely worth the effort.

Advanced Tax Planning Strategies Complementing Tax Diversification

While a solid tax diversification strategy high income lays the groundwork for reducing taxes and maximizing your wealth, blending in advanced tax planning techniques can take your savings even further. Let’s dive into some smart strategies that complement your tax diversification approach.

Charitable Giving Strategies

Giving to charity is wonderful—it supports the causes you care about and, as a bonus, can significantly lower your taxes if done strategically. For instance, Donor-Advised Funds (DAFs) let you contribute a larger sum during a high-income year, instantly capturing tax deductions. Then, you can spread charitable donations across multiple years, maximizing tax benefits and flexibility.

If you’re 70½ or older, Qualified Charitable Distributions (QCDs) are another option. You can donate directly from your IRA to your favorite charities, meeting your Required Minimum Distributions (RMDs) without bumping up your taxable income. Not bad for doing something good!

Another powerful tool is the Charitable Remainder Trust. This trust provides you with a stream of income during your lifetime, after which the remaining funds go to charity. You receive an upfront tax deduction and potentially reduce taxable income—a win-win solution.

Let’s say you typically donate about $10,000 each year. Instead, “bunching” multiple years’ donations—say, $50,000—in a single year through a Donor-Advised Fund can help you exceed the standard deduction threshold. This allows for greater immediate tax savings and ensures your generosity goes even further.

Equity Compensation Planning

For high-income earners who receive equity compensation—such as stock options, restricted stock units (RSUs), or Employee Stock Purchase Plans (ESPPs)—careful planning can mean significant tax savings.

Equity compensation often triggers taxes at key moments, such as when Restricted Stock Units vest or when you exercise stock options. Planning these events around your broader tax diversification strategy high income can reduce surprise tax bills. For example, timing the exercising of stock options carefully can help you avoid jumping into a higher tax bracket, saving thousands in unnecessary taxes.

Similarly, understanding the difference between qualifying and disqualifying dispositions with an ESPP can make a substantial impact. Coordinating these choices with your other investments and retirement accounts can help minimize your tax liability and preserve your wealth.

Impact on Estate and Wealth Transfer Planning

An effective tax diversification strategy high income isn’t just about your present-day taxes—it also plays a vital role in estate and wealth transfer planning. After all, the goal is to protect your hard-earned savings for future generations.

One key strategy is lifetime gifting. Each year, the IRS sets an annual gift tax exclusion amount that you can gift per recipient without owing gift taxes. By consistently gifting over time, you gradually transfer wealth tax-free—benefiting your loved ones while reducing your taxable estate.

Another smart method is the use of grantor trusts. For instance, an intentionally defective grantor trust (IDGT) allows you, as the grantor, to pay taxes on trust income while effectively gifting extra value to the beneficiaries tax-free. Likewise, establishing a Grantor Retained Annuity Trust (GRAT) or a Family Limited Partnership (FLP) can help transfer wealth efficiently and reduce the estate taxes owed by your family later on.

Don’t overlook the power of Roth conversions for legacy planning either. Roth IRAs don’t have Required Minimum Distributions for the original owner, giving you flexibility to leave money to heirs who may benefit from decades of tax-free growth.

By thoughtfully integrating these advanced techniques with your tax diversification plan, you’re not just optimizing your current financial picture—you’re laying down a sturdy foundation for generations to come.

Through strategies like these, Elite Tax Strategy Solutions helps you combine proactive planning with your personal and family goals—ensuring you maximize tax savings now, while creating a lasting legacy.

Risks of Not Implementing a Tax Diversification Strategy

When it comes to your financial future, putting all your eggs in one tax basket can be just as risky as investing everything in a single stock. Many high-income professionals I’ve worked with over the years have learned this lesson the hard way.

1. Concentration Risk

Think about concentration risk like this: if you’re caught in a downpour with only one type of rain protection, you’re limited by what that single tool can do. The same applies to your retirement savings.

If you’ve built all tax-deferred accounts (like traditional 401(k)s), you’ll face a tax bill on every dollar you withdraw in retirement. I remember working with a surgeon who had accumulated over $3 million in his 401(k), but when retirement came, he was shocked by how much Uncle Sam claimed from his withdrawals.

With all taxable accounts, you’ll miss years of powerful tax-deferred growth and potentially pay higher annual taxes on dividends and capital gains. And even with all tax-free (Roth) accounts, you may have unnecessarily paid higher taxes during your peak earning years when your tax rate was at its highest.

Tax diversification strategy high income planning helps protect you from these single-basket vulnerabilities.

2. Tax Bracket Management Limitations

Without diverse tax buckets, managing your tax brackets in retirement becomes like trying to drive with the parking brake on—technically possible, but far from optimal.

You might find yourself forced to take larger taxable withdrawals than you actually need for expenses. One retired executive I worked with had to withdraw $150,000 from his IRA to cover $100,000 in expenses because he needed to account for the taxes on the withdrawal itself.

Required Minimum Distributions (RMDs) from large tax-deferred accounts can also push you into higher tax brackets whether you need the money or not. And don’t forget about Medicare premiums—higher reported income can trigger Income Related Monthly Adjustment Amounts (IRMAA), sometimes adding thousands to your annual healthcare costs.

3. Reduced Flexibility for Changing Tax Laws

Tax laws are about as permanent as fashion trends—they’re always changing. Without tax diversification strategy high income planning, you’re more vulnerable when these changes occur.

If tax rates increase in the future (which many financial experts predict) and all your savings are in tax-deferred accounts, you’ll pay those higher rates on every dollar you withdraw. I’ve seen clients caught in this exact situation, watching helplessly as tax changes eroded their carefully saved nest eggs.

Conversely, if the preferential treatment of capital gains is reduced or eliminated and your wealth is primarily in taxable accounts, you could lose a significant tax advantage overnight.

4. Missed Opportunities for Tax-Free Growth

The magic of compound growth is powerful, but tax-free compound growth is even more potent. Without tax-free accounts in your portfolio, you’re missing out on one of the most valuable wealth-building tools available.

Let me share a real story that illustrates this point. Two dentists started practices around the same time with similar incomes. One focused entirely on traditional retirement accounts while the other split her savings between traditional and Roth accounts. After 25 years, the second dentist had nearly $600,000 more in after-tax retirement wealth, despite making identical contributions.

As one of our clients, a physician with a substantial 401(k) balance but no Roth accounts, told me with regret: “I wish I had diversified my tax strategy earlier. Now I’m facing large RMDs that will keep me in the highest tax bracket throughout retirement.”

The truth is, most high-income professionals are excellent at earning money and even saving it—but without proper tax diversification strategy high income planning, they may be unintentionally setting themselves up for unnecessary tax burdens in the future. The good news? It’s rarely too late to start implementing a more balanced approach, even if you’re approaching retirement.

Frequently Asked Questions about Tax Diversification Strategies for High-Income Earners

What is a tax diversification strategy and why is it important for high-income individuals?

Simply put, a tax diversification strategy high income involves spreading your investments across accounts with different tax treatments—these include taxable, tax-deferred, and tax-free accounts. Think of it as creating multiple “buckets” to hold your money, each taxed differently.

Why does this matter so much if you’re a high earner? Well, when you’re making a significant income, you’re likely paying hefty taxes. By having your investments diversified across these buckets, you gain flexibility to manage your tax bill effectively during retirement. You won’t be stuck paying high taxes on every dollar you withdraw.

Another advantage is it helps you steer uncertainty in future tax laws. Imagine tax rates skyrocket right when you’re retiring—ouch! With a well-balanced tax diversification plan, you have the freedom to pivot and draw from the buckets that make the most sense at that moment. Additionally, studies have found that smart tax diversification can potentially extend the longevity of your retirement portfolio by up to 10%.

Benjamin Franklin said, “In this world, nothing is certain except death and taxes.” While we can’t eliminate taxes entirely (sorry!), tax diversification gives high-income earners greater control over how and when they pay taxes, letting you keep more of your hard-earned wealth in the long run.

How can high-income earners implement tax diversification in their financial planning?

Putting together an effective tax diversification strategy high income might seem complicated, but breaking it down makes things clearer. First off, you’ll want to maximize your contributions to tax-advantaged retirement accounts like your 401(k), 403(b), or other employer-sponsored plans. These tax-deferred accounts lower your current taxable income, deferring taxes until retirement when you might be in a lower tax bracket.

Now, if you’re earning too much to directly contribute to a Roth IRA, don’t despair! You can use backdoor Roth strategies—contributing after-tax dollars into a traditional IRA and then converting them immediately to a Roth. If your employer allows it, consider a mega backdoor Roth conversion, which lets you stash even more in tax-free accounts.

Don’t overlook taxable brokerage accounts either. They give you liquidity and flexibility, but you’ll want to focus on tax-efficient investments here—things like index ETFs, municipal bonds, or stocks you intend to hold for the long haul.

Timing Roth conversions strategically during lower-income years can also significantly reduce your future tax liabilities. Keep your eyes peeled for opportunities—maybe you take a sabbatical or decide to semi-retire—to convert traditional IRA or 401(k) funds to a Roth IRA when your income temporarily dips.

If you’re eligible, Health Savings Accounts (HSAs) offer a rare triple-tax benefit: contributions are deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. It’s essentially the unicorn of tax-advantaged accounts!

And if you’re a high earner running your own business or working as an executive, advanced strategies like Cash Balance Plans, Defined Benefit Pension Plans, or Non-Qualified Deferred Compensation can play important roles in your overall tax diversification game plan.

At Elite Tax Strategy Solutions, we offer personalized guidance, helping you strategically balance contributions, execute Roth conversion ladders, and integrate these advanced tax strategies seamlessly into your financial planning.

What are the potential risks of not implementing a tax diversification strategy?

Choosing not to implement a thoughtful tax diversification strategy high income can leave you vulnerable in several key areas.

First, there’s the uncertainty around tax rates. Nobody can predict future tax laws accurately. If all your wealth is concentrated in one type of account, such as traditional tax-deferred retirement accounts, you could face a nasty surprise if tax rates rise significantly in the future. All your withdrawals would then be taxed at these higher rates, directly eating into your retirement nest egg.

Lack of diversification also reduces your flexibility in retirement. Without multiple tax buckets to draw from, you’ll have fewer options for managing tax brackets strategically. This could result in paying more taxes than necessary throughout retirement.

If you’ve built most of your savings in traditional IRAs or 401(k)s, large Required Minimum Distributions (RMDs) can push you into higher tax brackets, even if your spending needs are modest—a frustrating scenario that can be avoided with a balanced diversification strategy.

There’s also the missed opportunity for decades of tax-free compounding growth by neglecting Roth or other tax-free accounts. Over time, that loss of tax-free growth can seriously dent your long-term wealth potential.

Lastly, tax laws change frequently—sometimes drastically. Relying heavily on only one type of tax treatment exposes you to potential negative impacts from future law changes.

I recall a client who had diligently saved over $3 million exclusively in traditional retirement accounts. When retirement arrived, he found himself stuck in the highest tax bracket due to mandatory large RMDs—despite his relatively modest yearly expenses. Proper tax diversification would have offered a smarter and significantly less taxing outcome (pun intended).

Conclusion

Throughout this guide, we’ve explored why a thoughtful tax diversification strategy high income isn’t simply about reducing taxes today—it’s about crafting a long-term plan that keeps more money in your pocket over your lifetime, and even beyond.

“When it comes to wealth, managing taxes isn’t just a task—it’s a strategy.”

High-income earners like you face unique tax challenges. Higher tax brackets, phased-out deductions, and ever-changing tax laws can feel overwhelming. But by strategically balancing your investments across taxable, tax-deferred, and tax-free accounts, you gain crucial flexibility. You can adapt your financial moves to changes in tax legislation, your personal income fluctuations, and other unexpected life events.

The positive impact of this approach can be remarkable. Studies have shown that proper tax diversification can extend the life of your retirement portfolio by more than 10%. Imagine retiring with confidence, knowing your savings will comfortably last. It can also result in potential tax savings of up to 20% by carefully managing how and when you access your accounts. That extra savings can mean more travel, more hobbies—or more money to pass down to your loved ones.

And speaking of loved ones—tax diversification isn’t just about you. It also improves your ability to plan strategically for wealth transfer and estate planning. Utilizing accounts like Roth IRAs or leveraging Roth conversions can mean leaving behind a legacy that is tax-efficient for generations to come.

At Elite Tax Strategy Solutions, this is exactly what we specialize in. We don’t just crunch numbers—we listen, we strategize, and we craft personalized tax plans specifically designed for high-income earners. Our proactive approach goes beyond basic tax preparation. We integrate advanced strategies into your financial planning, ensuring your tax strategy complements your overarching financial goals.

Tax diversification isn’t a “set it and forget it” concept. It’s an ongoing process that should evolve right alongside your life and the ever-shifting tax landscape. Regularly revisiting your approach with qualified professionals is essential to staying ahead and making the most of every opportunity.

So, don’t wait until tax season rolls around again. You deserve a strategic, proactive plan that empowers you to keep more of the money you’ve worked so hard for. To find how we can tailor an effective tax diversification strategy high income and explore other Innovative Tax Planning Services, reach out to our team today.

Together, we’ll create a tax-smart roadmap that protects and grows your wealth—now and in the future.