Tax planning for high salaried employees is essential for maintaining and growing wealth. High-salaried employees, like senior executives, doctors, and engineers, face significant tax burdens due to their higher earnings. Here’s a quick guide to help you understand the basics:

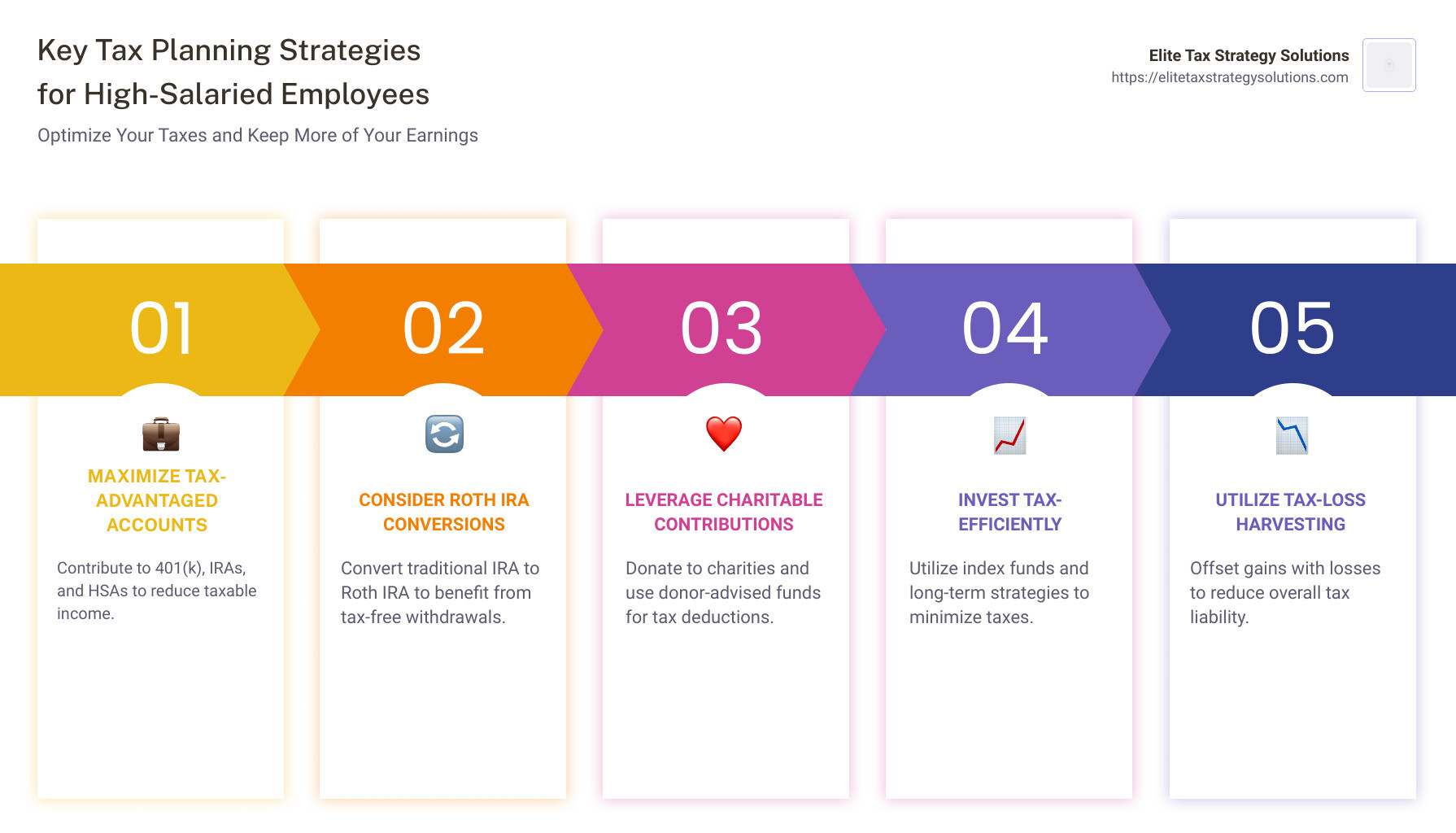

- Maximize tax-advantaged accounts like 401(k) and IRAs.

- Consider Roth IRA conversions despite income limitations.

- Leverage charitable contributions for immediate deductions.

- Invest tax-efficiently using index funds and long-term strategies.

- Use tax-loss harvesting to offset gains and reduce overall tax bills.

“It’s not what you make but what you keep that counts,” is a saying that perfectly encapsulates why tax planning is so crucial for high-salaried employees. Despite having fewer tax benefits compared to business owners, high-salaried employees can still use various strategies to minimize tax liabilities and maximize net income.

I’m David Fritch. With 40 years of experience as a CPA and tax advisor, I’ve helped numerous high-income earners optimize their tax strategies. My goal is to simplify the complex world of tax planning and help you keep more of what you earn.

Know your tax planning for high salaried employees terms:

– advanced tax planning strategies

– financial planning for high income earners

– tax advice for high earners

Understanding High Income and Tax Brackets

When it comes to tax planning for high salaried employees, understanding the IRS definitions and tax brackets is crucial. Let’s break it down:

IRS Definition of High-Income Earners

The IRS classifies high-income earners as those who fall into the top three tax brackets. For single filers, this means earning more than $191,951 in taxable income. For married couples filing jointly, the threshold is $383,901. If you’re in these brackets, you’re considered a high-income earner.

Tax Brackets and Marginal Tax Rates

Tax brackets determine the rate at which your income is taxed. The U.S. tax system is progressive, which means higher earnings are taxed at higher rates. Here’s a simplified look at the tax brackets relevant to high-income earners:

- $191,951 – $243,725: Taxed at 32%

- $243,726 – $609,350: Taxed at 34%

- Over $609,350: Taxed at 37%

Your marginal tax rate is the rate at which your last dollar of income is taxed. For example, if your taxable income is $250,000, your marginal tax rate is 34%. However, not all your income is taxed at this rate. Only the income over $243,726 is taxed at 34%; the rest is taxed at the lower rates of the preceding brackets.

Alternative Minimum Tax (AMT)

The Alternative Minimum Tax (AMT) is a parallel tax system designed to ensure that high-income earners pay a minimum amount of tax. The AMT disallows many deductions and exemptions that are available under the regular tax system.

For instance, if your income exceeds certain thresholds, you may be subject to the AMT. This system recalculates your income tax after adding back certain deductions. If the AMT results in a higher tax bill than the regular tax calculation, you pay the AMT amount.

Why This Matters

Understanding these tax brackets and the AMT is essential for high-income earners to optimize their tax planning strategies. By knowing where you stand, you can make informed decisions to minimize your tax liability.

In the next section, we’ll dive into strategies to reduce your taxable income, including maximizing tax-advantaged accounts and utilizing charitable contributions effectively.

Strategies to Reduce Taxable Income

When it comes to tax planning for high salaried employees, there are several effective strategies to reduce your taxable income. Let’s explore some of the best options.

Maximize Tax-Advantaged Accounts

401(k) and Roth 401(k)

Contributing to a 401(k) or Roth 401(k) can significantly reduce your taxable income. For 2024, the maximum contribution limit for a 401(k) is $23,000. If you’re over 50, you can take advantage of catch-up contributions, adding an extra $7,500. Traditional 401(k) contributions are made pre-tax, lowering your taxable income, while Roth 401(k) contributions are made post-tax, allowing for tax-free withdrawals in retirement.

IRA, SEP-IRA, and Solo 401(k)

Individual Retirement Accounts (IRAs) offer another avenue for tax savings. Traditional IRAs reduce your taxable income now, while Roth IRAs offer tax-free growth and withdrawals. For self-employed individuals, SEP-IRAs and Solo 401(k)s are excellent options. SEP-IRAs allow for contributions up to the lesser of 25% of your net earnings or $66,000 for 2024. Solo 401(k)s offer even more flexibility, combining the benefits of a traditional 401(k) and a profit-sharing plan.

HSA and FSA

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) are also powerful tools. HSAs are triple tax-advantaged: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. For 2023, you can contribute up to $7,750 for a family. FSAs allow you to save up to $3,050 pre-tax in 2023, though they follow a “use it or lose it” policy.

Roth IRA Conversions

Backdoor Roth IRA and Mega Backdoor Roth IRA

High-income earners often can’t contribute directly to a Roth IRA due to income limits. However, you can still convert a traditional IRA to a Roth IRA through a process known as a backdoor Roth IRA. This involves making non-deductible contributions to a traditional IRA and then converting it to a Roth IRA. A mega backdoor Roth IRA allows even higher contributions by using after-tax contributions in a 401(k) plan that can be rolled over to a Roth IRA.

Pro-Rata Rule

Be aware of the Pro-Rata rule, which requires you to consider all your traditional IRAs when converting to a Roth IRA. This means the amount converted will be taxed proportionally to your pre-tax and post-tax contributions.

Charitable Contributions

Donor-Advised Funds

Setting up a donor-advised fund allows you to make a charitable contribution, receive an immediate tax deduction, and then distribute the funds to charities over time. This is particularly useful for high-income earners looking to bunch donations to exceed the standard deduction threshold.

Appreciated Assets

Donating appreciated assets like stocks or real estate can provide a double tax benefit. You avoid capital gains tax on the appreciation and receive a charitable deduction for the fair market value of the asset.

Charitable Remainder and Lead Trusts

Charitable Remainder Trusts (CRTs) and Charitable Lead Trusts (CLTs) offer more complex strategies. CRTs provide an income stream to you or a beneficiary for a specified period, with the remainder going to charity. CLTs, on the other hand, provide payments to a charitable organization for a set period, with the remaining assets going to your heirs.

Tax-Efficient Investments

Index Funds and ETFs

Investing in index funds and exchange-traded funds (ETFs) can be more tax-efficient than actively managed funds. These funds typically generate fewer taxable events, such as capital gains distributions.

Asset Location

Strategically placing different types of investments in various accounts can minimize your tax liability. For example, place tax-inefficient investments in tax-advantaged accounts and tax-efficient investments in taxable accounts.

Long-Term Capital Gains and Tax-Exempt Municipal Bonds

Holding investments for over a year qualifies you for long-term capital gains tax rates, which are lower than short-term rates. Additionally, investing in tax-exempt municipal bonds can provide tax-free interest income.

Tax-Loss Harvesting

Offset Gains

Tax-loss harvesting involves selling investments at a loss to offset gains elsewhere in your portfolio. This can reduce your overall tax liability. If your capital losses exceed your capital gains, you can use the excess losses to offset up to $3,000 of other income and carry forward any remaining losses to future tax years.

Wash-Sale Rules

Be mindful of wash-sale rules, which prevent you from buying back the same or substantially identical securities within 30 days of selling them at a loss. Violating these rules can disqualify your tax deduction.

By implementing these strategies, you can effectively reduce your taxable income and optimize your tax situation.

In the next section, we’ll dive into advanced tax planning techniques, including business ownership and deductions, real estate investments, and deferred compensation plans.

Advanced Tax Planning Techniques

Business Ownership and Deductions

Owning a business can provide significant tax benefits. Let’s explore some key strategies:

Home Office Deductions

If you run a business from home, you might be eligible for home office deductions. To qualify, your home office must be your principal place of business and used regularly and exclusively for work. You can deduct a portion of your mortgage interest, utilities, and other home-related expenses.

Business Expenses

Many expenses related to running your business can be deducted. This includes costs like office supplies, software, and even a portion of your internet bill. Keeping detailed records is crucial to maximize these deductions.

Restructuring Entities

Choosing the right business structure can impact your tax liability. For instance, restructuring from a sole proprietorship to an S Corporation can reduce self-employment taxes. Consult with a tax professional to determine the best structure for your business.

Retirement Plans for Self-Employed

Self-employed individuals can set up retirement plans like SEP-IRAs or Solo 401(k)s. These plans offer higher contribution limits than traditional IRAs, allowing you to save more for retirement while reducing your taxable income.

Real Estate Investments

Investing in real estate offers various tax advantages:

Mortgage Interest Deduction

If you own property, you can deduct the interest paid on your mortgage. For mortgages taken out after December 15, 2017, interest on up to $750,000 in principal is tax-deductible.

Depreciation Deduction

The IRS allows you to deduct a portion of your property’s cost each year as depreciation. This applies even if the property appreciates in value. This deduction is only available for properties used for business or income-generating activities.

1031 Exchange

A 1031 exchange lets you defer capital gains taxes by reinvesting the proceeds from the sale of one investment property into another like-kind property. This can be a powerful tool for real estate investors looking to grow their portfolios without immediate tax consequences.

Deferred Compensation Plans

Deferring your income can help you manage your tax liability more effectively:

Deferred Compensation

Deferred compensation plans allow you to defer a portion of your salary into a tax-advantaged account. This income is not taxed until you receive it, typically in retirement when you might be in a lower tax bracket.

Stock Options

Stock options provide another avenue for deferring income. You can choose when to exercise these options, allowing you to control when the associated income is recognized. This can be particularly useful in high-income years.

Bonuses and Year-End Income

If you anticipate a high-income year, consider deferring bonuses or additional income to the following year. This can help smooth out your taxable income over multiple years and potentially reduce your overall tax rate.

SALT Deductions

State and local taxes (SALT) can take a significant bite out of your income. Here are some strategies to mitigate this:

Itemizing Deductions

To claim SALT deductions, you need to itemize your deductions on your federal tax return. This allows you to deduct up to $10,000 in state income taxes, property taxes, and certain local taxes from your federal taxable income.

State Tax Planning

Some states offer tax credits, deductions, or incentives for specific activities, such as investing in certain industries or supporting renewable energy initiatives. Additionally, contributing to a 529 plan for education expenses might offer state tax benefits, depending on your state’s rules.

By leveraging these advanced tax planning techniques, high-salaried employees can significantly reduce their tax liabilities and optimize their financial situations.

In the next section, we’ll address frequently asked questions about tax planning for high-salaried employees.

Frequently Asked Questions about Tax Planning for High-Salaried Employees

How to reduce taxes as a high-income earner?

Donating Low Cost Basis Stock

One effective way to reduce your tax burden is by donating appreciated stocks. Instead of selling the stocks and paying capital gains tax, you can donate them directly to a charity. You get a tax deduction for the full market value of the stock, and the charity avoids paying capital gains tax.

Contributing to a Donor-Advised Fund

A donor-advised fund (DAF) allows you to make charitable contributions, receive an immediate tax deduction, and then distribute the funds to charities over time. This is particularly useful in years when you have higher-than-normal income. You get the deduction now and can decide later which charities to support.

Stacking Future Charitable Donations

If you plan to make charitable donations over several years, consider “bunching” them into a single year. This can push you over the standard deduction threshold, allowing you to itemize and get a bigger tax break. For example, instead of donating $10,000 each year for three years, donate $30,000 in one year.

How to avoid the 32% tax bracket?

Contribute to Retirement Plans

Maximizing contributions to employer-sponsored retirement plans like a 401(k) or a traditional IRA can significantly reduce your taxable income. For 2024, you can contribute up to $22,500 to your 401(k), and those over 50 can make an additional $7,500 in catch-up contributions.

Avoid Selling Too Many Assets in One Year

If you have investments, be mindful of selling too many in a single year, which could push you into a higher tax bracket. Spread the sales over multiple years to manage your taxable income more effectively.

Time Your Income and Business Expenses

If you have control over your income and expenses, such as bonuses or business expenses, consider timing them to manage your taxable income. For example, defer receiving a bonus to the following year if you expect to be in a lower tax bracket.

Pay Deductible Expenses and Make Contributions in High-Income Years

If you expect your income to fluctuate, try to pay deductible expenses and make charitable contributions in years when your income is higher. This can help lower your taxable income for those high-earning years.

How do high-income earners pay no tax?

Investment Income

High-income earners often focus on generating investment income rather than wages. Investment income, such as dividends and capital gains, is often taxed at lower rates than ordinary income.

Long-Term Capital Gains

Investing in assets held for over a year can qualify you for long-term capital gains tax rates, which are lower than ordinary income tax rates. The maximum federal tax rate for long-term capital gains is 20%, compared to the top ordinary income tax rate of 37%.

Qualified Dividends

Investing in companies that pay qualified dividends can also reduce your tax burden. Qualified dividends are taxed at the lower capital gains rates, rather than ordinary income rates. To qualify, dividends must be paid by a U.S. corporation or a qualified foreign corporation and meet certain holding period requirements.

0 Percent Rate for Certain Taxable Income

Some high-income earners manage their portfolios to take advantage of the 0% capital gains tax rate on the first $89,250 of taxable income for married couples filing jointly (as of 2024). This involves careful planning and a solid understanding of the tax code.

By implementing these strategies, high-salaried employees can effectively reduce their tax liabilities and maximize their take-home pay.

In the next section, we’ll summarize the importance of proactive tax planning and how Elite Tax Strategy Solutions can help you achieve your financial goals.

Conclusion

In summary, proactive tax planning is not just a luxury but a necessity for high-salaried employees. Earning a substantial income often means facing higher tax rates, but with careful planning and strategic actions, you can significantly reduce your tax burden and maximize your wealth.

Key Takeaways:

- Understand Your Tax Bracket: Knowing where you stand helps in making informed decisions.

- Maximize Tax-Advantaged Accounts: Use 401(k)s, IRAs, HSAs, and FSAs to reduce taxable income.

- Leverage Roth Conversions: Explore backdoor and mega backdoor Roth IRAs.

- Charitable Contributions: Use donor-advised funds and bunching donations to maximize deductions.

- Tax-Efficient Investments: Focus on index funds, ETFs, and long-term capital gains.

- Advanced Techniques: Consider business ownership, real estate investments, and deferred compensation plans.

Proactive tax planning allows you to keep more of what you earn, ensuring that your hard work translates into long-term financial stability. The strategies discussed are not one-size-fits-all; they need to be custom to your unique financial situation.

At Elite Tax Strategy Solutions, we specialize in providing personalized tax planning services for high earners. Our comprehensive approach ensures that you are always ahead of the curve, leveraging over 100 custom tax-saving strategies to optimize your financial health.

Ready to take control of your tax planning? Contact us today to schedule a consultation and find how we can help you achieve your financial goals.