Why Smart Tax Planning Advice Makes All the Difference

Tax planning advice that actually works doesn’t have to be boring or overwhelming. Here’s what you need to know right now:

Essential Tax Planning Actions:

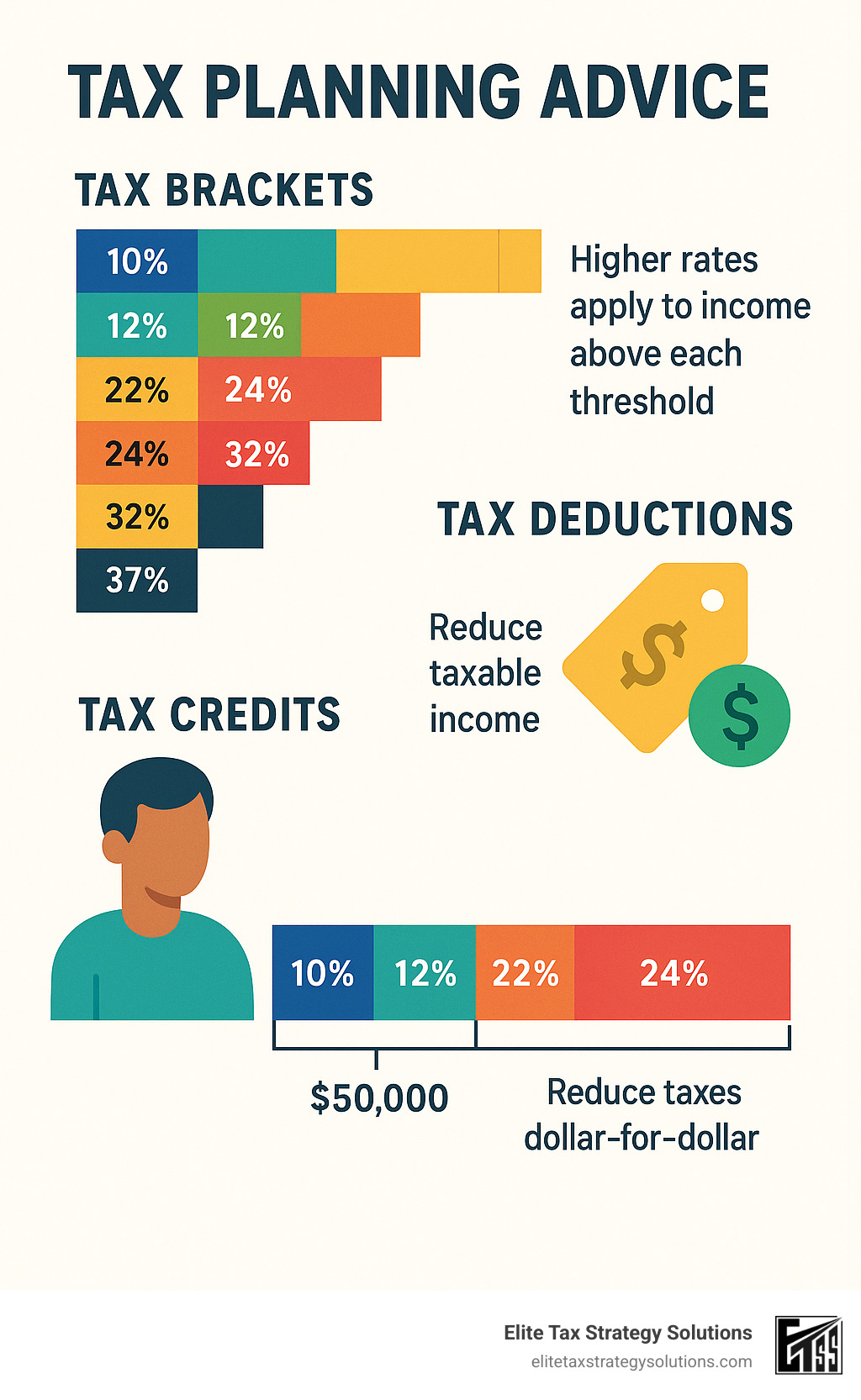

– Understand your tax bracket – You only pay higher rates on income above each threshold

– Maximize deductions vs. credits – Deductions reduce taxable income, credits reduce taxes dollar-for-dollar

– Use tax-advantaged accounts – 401(k), IRA, HSA contributions can slash your current tax bill

– Time your income and expenses – Bunch deductions, harvest losses, manage capital gains timing

– Keep proper records – Save tax documents for at least 3 years (6 years if you underreport income by 25%+)

– Adjust withholding – Use Form W-4 to avoid big tax bills or get more cash in your paycheck

Most people think tax planning happens once a year during filing season. That’s backwards. The smartest tax moves happen throughout the year – adjusting your paycheck withholding in January, maxing out retirement contributions by December, and timing investment sales to minimize capital gains.

The stakes are higher than ever. With the Tax Cuts and Jobs Act set to expire in 2025, tax rates could jump significantly. Plus, the IRS underpayment penalty interest rate sits at 7% – making mistakes expensive.

I’m David Fritch, and I’ve spent 40 years helping high-income earners and small business owners steer complex tax regulations through my CPA practice and law firm. My experience delivering personalized tax planning advice has shown me that the right strategies can save clients thousands while reducing stress and ensuring compliance.

Must-know tax planning advice terms:

– tax-efficient estate planning

– tax planning for real estate investors

– financial stability planning

Understand the U.S. Tax Landscape

The U.S. tax system is like puzzle pieces that fit together in a specific way. Once you see how these pieces connect, smart tax planning advice becomes much clearer.

The biggest myth? That you pay your highest tax rate on every dollar you earn. This misunderstanding leads to poor financial decisions and missed opportunities.

How the Progressive Tax System Works

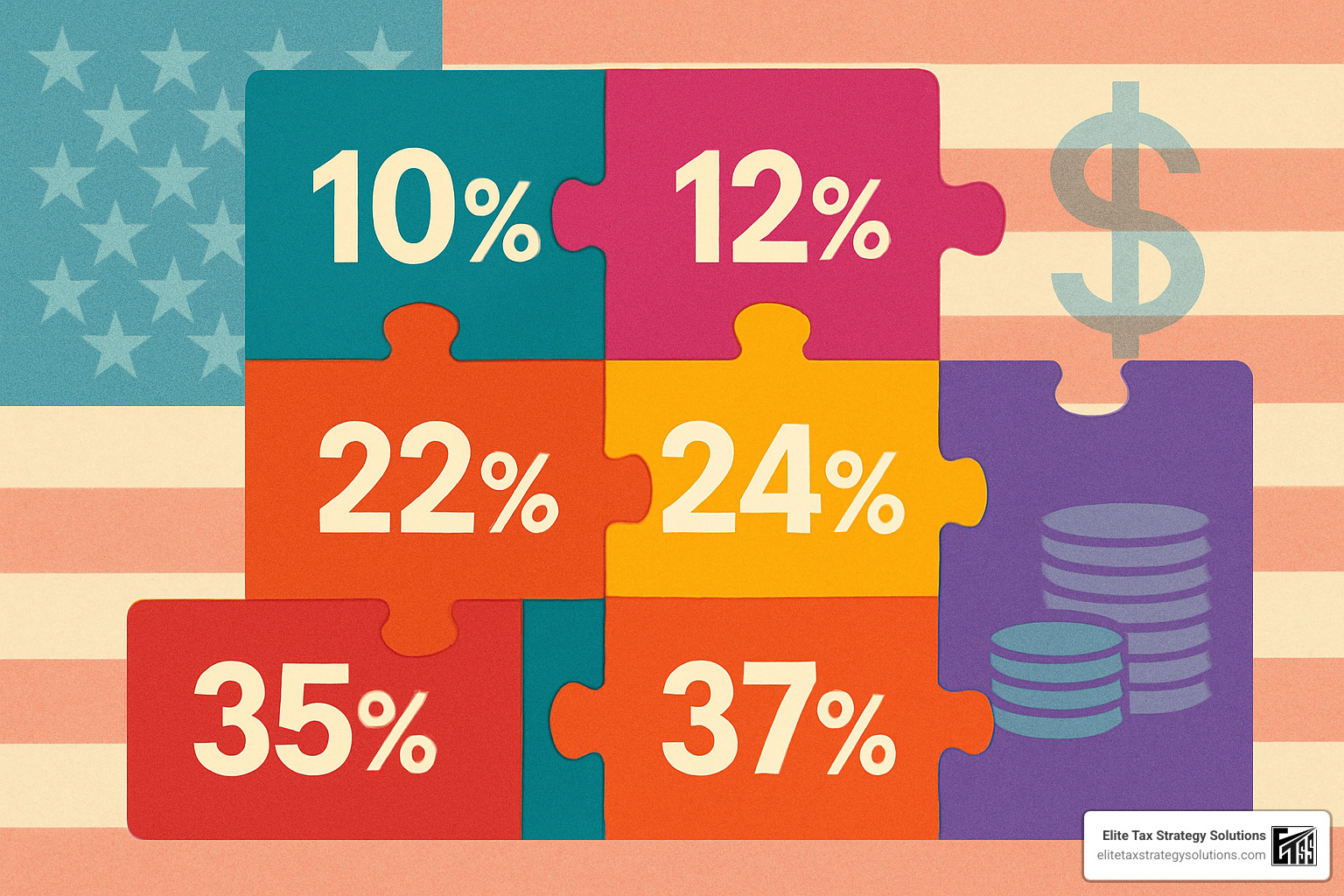

Think of the progressive tax system as a series of buckets, each with its own tax rate. We have seven federal income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. You fill up the lower buckets first, and only pay higher rates on income that spills into higher buckets.

Let’s make this real with an example. Say you’re single with $50,000 in adjusted gross income (AGI). You don’t get hit with 22% on all fifty thousand dollars. Instead:

The first $11,600 gets taxed at 10%. Then income from $11,601 to $35,500 gets taxed at 12%. Only the remaining portion up to $50,000 faces the 22% rate.

This chunking system means your marginal tax rate (the rate on your last dollar earned) is different from your effective tax rate (what you actually pay overall). Your effective rate will always be lower than your marginal rate.

Deductions vs. Credits—Why They Matter

Tax deductions and credits both put money back in your pocket, but they work completely differently.

Tax deductions shrink your taxable income before calculating what you owe. There are above-the-line deductions that reduce your AGI (like IRA contributions) and itemized deductions that you list on Schedule A. If you’re in the 24% bracket and claim a $1,000 deduction, you save $240 in actual taxes.

Tax credits work like dollar-for-dollar coupons against your tax bill. A $1,000 credit saves you exactly $1,000, no matter what bracket you’re in. That’s why credits are usually more valuable than deductions.

Credits come in two flavors: refundable credits can actually put money in your pocket even if you owe no tax, while non-refundable credits can only reduce your tax bill to zero.

Standard Deduction or Itemize?

Every year, you face this choice: take the standard deduction or itemize your expenses. For 2024, the standard deduction amounts are $14,600 for single filers, $29,200 for married filing jointly, and $21,900 for head of household.

The math is simple: itemize only if your total itemized deductions on Schedule A exceed these amounts. Your biggest itemized deductions typically include state and local taxes (remember the $10,000 SALT cap), mortgage interest, charitable contributions, and medical expenses over 7.5% of your AGI.

| Filing Status | Standard Deduction 2024 | When to Consider Itemizing |

|---|---|---|

| Single | $14,600 | Itemized deductions exceed $14,600 |

| Married Filing Jointly | $29,200 | Itemized deductions exceed $29,200 |

| Head of Household | $21,900 | Itemized deductions exceed $21,900 |

Once you know how brackets, deductions, and credits actually work, you can start making moves that save real money.

Year-Round Tax Planning Advice

Here’s the most valuable tax planning advice you’ll get: stop thinking about taxes as something you deal with once a year. The smartest taxpayers make moves throughout the year that save them serious money come April.

Think of it like tending a garden. You don’t wait until harvest time to water your plants – you nurture them all season long. Your taxes work the same way. Small adjustments made consistently throughout the year can yield big savings when it’s time to file.

According to scientific research on proactive planning, taxpayers who plan year-round consistently achieve better outcomes than those who scramble at tax time.

Tune-Up Your Paycheck Early

Your Form W-4 might be the most underused tool in your tax-saving toolkit. Most people fill it out once when they start a job and never touch it again. Big mistake.

Start each January by visiting the IRS Tax Withholding Estimator. This free tool helps you find the sweet spot where you’re not overpaying throughout the year (giving the government an interest-free loan) or underpaying and facing penalties.

The underpayment penalty kicks in if you owe $1,000 or more at filing time. But you can avoid it by meeting the safe-harbor rules. Pay either 90% of this year’s tax or 100% of last year’s tax (110% if your prior-year adjusted gross income topped $150,000).

Life changes? Update your W-4. Got married, divorced, had a baby, or landed a new job? These events all affect your optimal withholding.

Super-Charge Tax-Advantaged Accounts

Tax-advantaged accounts are like getting a discount on your taxes. The government literally encourages you to save money by giving you tax breaks.

Your 401(k) is your first stop. For 2025, you can stash away up to $23,500. If you’re 50 or older, add another $7,500 in catch-up contributions. The SECURE 2.0 Act gives people aged 60-63 even higher catch-up limits – up to $34,750 total.

IRAs give you more options. Traditional IRAs might let you deduct your contributions now and pay taxes later. Roth IRAs flip this – you pay taxes now but withdraw everything tax-free in retirement.

Health Savings Accounts are the triple crown of tax advantages. You get a deduction when you contribute, your money grows tax-free, and you withdraw it tax-free for medical expenses. For 2025, you can contribute up to $4,300 for individual coverage or $8,550 for family coverage. Add $1,000 more if you’re 55 or older.

529 plans help with education costs. While you don’t get a federal tax deduction, many states offer tax breaks. You can contribute up to $19,000 per beneficiary in 2025 without gift tax issues.

For more detailed strategies on maximizing these accounts, check out our Tax Planning Tips.

Tactical Timing: Harvest, Bunch & Defer

Smart timing can turn ordinary financial moves into tax-saving strategies.

Tax-loss harvesting turns your investment losses into tax savings. When you sell investments at a loss, you can offset gains elsewhere in your portfolio. You can use up to $3,000 of net losses each year to reduce your ordinary income. Any extra losses carry forward to future years.

Just watch out for the wash-sale rule – you can’t buy back the same or substantially similar investment within 30 days, or the IRS disallows the loss.

Bunching deductions works when your itemized deductions hover around the standard deduction amount. Instead of claiming similar deductions each year, bunch two years’ worth of charitable contributions, medical expenses, or other deductions into one year.

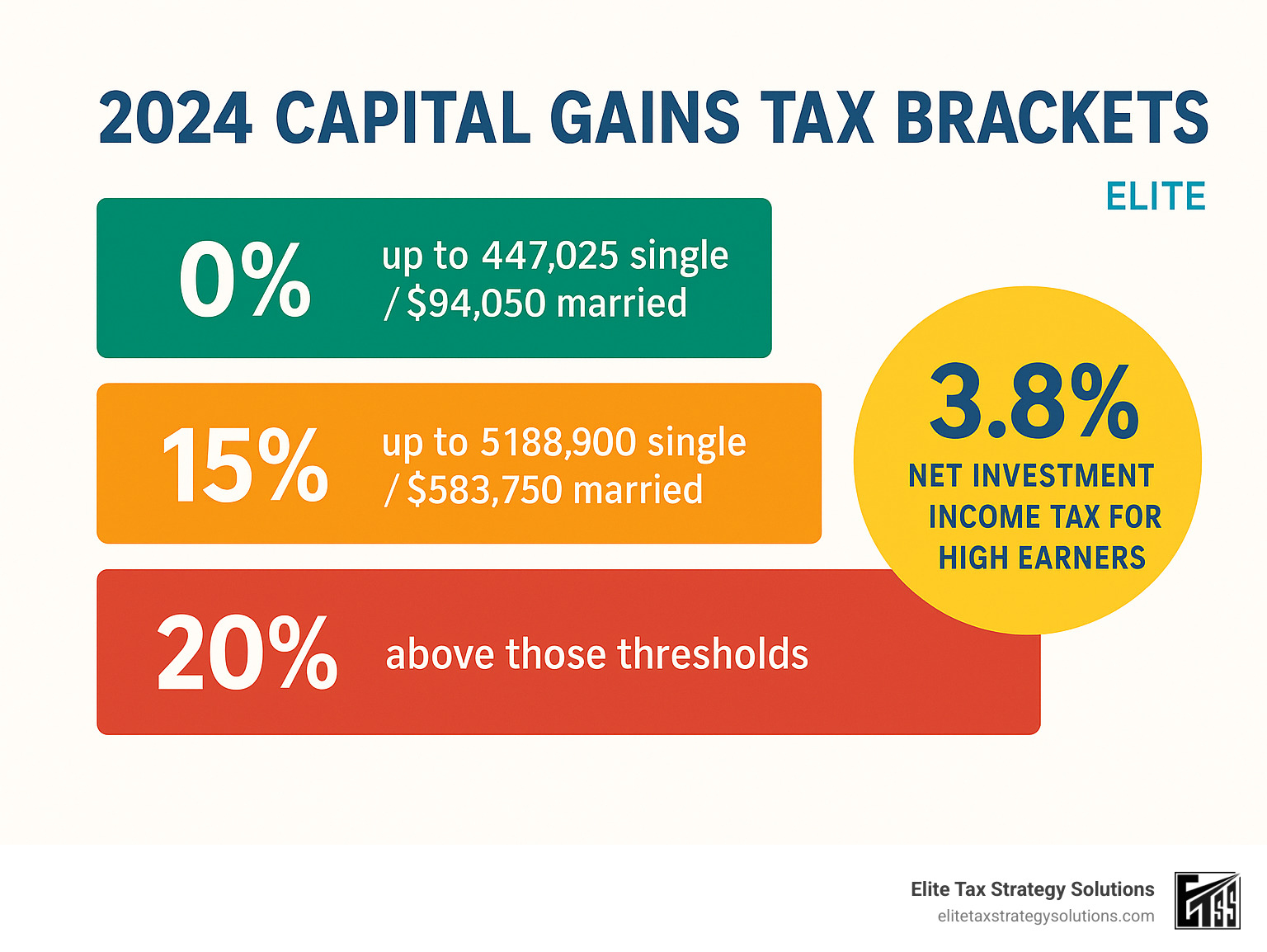

Capital gains timing matters more than most people realize. If your taxable income keeps you in the 0% long-term capital gains bracket (up to $47,025 for single filers in 2024), you can sell profitable investments and pay zero federal tax on the gains.

The key to all these strategies? Planning ahead. December 31st comes whether you’re ready or not. Start thinking about these moves in the fall, so you have time to execute them properly.

Smart Strategies to Reduce Tax Liability

Think of tax planning like chess – every move affects your next opportunity. The strategies in this section can save you thousands, especially if you’re earning six figures or running a business. Let’s explore the moves that separate smart taxpayers from those who pay more than they should.

Manage Investments & Capital Gains Like a Pro

Your investment strategy and tax strategy should work together, not against each other. The difference between smart and careless investment timing can cost you thousands in unnecessary taxes.

The most important rule? Hold investments for more than one year whenever possible. Long-term capital gains get preferential tax rates of 0%, 15%, or 20% depending on your income. Sell too early, and you’ll pay ordinary income tax rates up to 37% on short-term gains.

Here’s where it gets interesting: single filers with taxable income up to $47,025 (and married couples up to $94,050) pay 0% on long-term capital gains in 2024. This creates a golden opportunity to sell winning investments and reset your basis without paying federal taxes.

Municipal bonds offer another smart play for high earners. The interest is generally exempt from federal taxes and may avoid state taxes if you live in the issuing state. Just watch out – some municipal bond income can trigger the Alternative Minimum Tax.

Be careful about mutual fund distributions, especially in December. Buying a fund right before it makes a capital gains distribution is like volunteering to pay someone else’s tax bill. Check distribution dates before making large purchases.

For deeper investment tax planning advice, check out our comprehensive Tax Planning Strategies guide.

Retirement Withdrawals & Required Minimum Distributions

Once you hit age 73, the IRS forces your hand with Required Minimum Distributions from traditional retirement accounts. Miss an RMD, and you’ll face a 25% penalty on the amount you should have withdrawn. Get it fixed quickly, and the penalty drops to 10% – still painful, but better.

Qualified Charitable Distributions offer a brilliant workaround if you’re 70½ or older. You can send up to $105,000 annually directly from your IRA to charity. This satisfies your RMD requirement without adding to your taxable income – essentially making your charitable giving tax-free.

Roth conversion ladders work especially well during lower-income years. You’ll pay tax on the conversion amount now, but all future growth and withdrawals become tax-free. Think of it as paying taxes at today’s known rates instead of tomorrow’s unknown (and potentially higher) rates.

The SECURE 2.0 Act has expanded catch-up contribution limits and added flexibility for retirement distributions. These changes create new opportunities for strategic planning, especially for those approaching or in retirement.

Gifting & Estate Moves Before 2026

The clock is ticking on some major tax benefits. When the Tax Cuts and Jobs Act expires after 2025, the federal estate tax exemption will likely drop from $13.61 million per person to around $5-6 million. That’s a massive change that demands action now.

Annual gifting remains one of the simplest strategies. You can give $18,000 per recipient in 2024 ($36,000 for married couples) without touching your lifetime exemption. With multiple children and grandchildren, this adds up quickly.

Donor-advised funds let you have your cake and eat it too. Make a large charitable contribution this year to maximize your deduction, then distribute the money to charities over time. You get the immediate tax benefit while maintaining control over when and where the money goes.

The step-up in basis rule creates interesting planning opportunities. Assets held until death receive a “step-up” to fair market value, eliminating capital gains tax for heirs. This might influence whether you sell appreciated assets now or hold them for your beneficiaries.

Don’t wait until 2025 to start planning. The best estate strategies take time to implement properly. Learn more in our Benefits of Tax Planning resource.

Recordkeeping, Compliance & Professional Help

Think of good recordkeeping as your financial insurance policy. It’s not the most exciting part of tax planning advice, but it’s what protects you when the IRS comes knocking – and saves you money when it’s time to file.

I’ve seen too many clients scramble during tax season, frantically searching through shoeboxes of receipts or trying to recreate business expenses from memory. Don’t be that person. A little organization throughout the year saves massive headaches later.

What to Keep & How Long

The IRS audit window isn’t as scary as people think, but you need to understand the rules. Generally, the IRS has three years to audit your return from the filing date. However, if you underreport income by more than 25%, that window extends to six years. And if there’s fraud involved or you never filed? There’s no time limit at all.

Your W-2s and 1099s are obvious keepers – these income documents form the backbone of your return. Bank and investment statements provide backup for interest, dividends, and capital gains reporting. Receipts for deductible expenses might seem tedious to save, but they’re gold during an audit.

Charitable contribution documentation deserves special attention. For donations under $250, a receipt works fine. But larger gifts require written acknowledgment from the charity. And if you donated property worth more than $500? You’ll need detailed records of what you gave and when.

Home purchase and improvement records should be kept for as long as you own the property, plus three years after you sell. These records help establish your basis and can save thousands in capital gains taxes down the road.

Consider going digital with your storage. Scanning documents and storing them securely in the cloud protects against loss and makes everything searchable.

Sidestep Penalties & Interest

The IRS penalty structure can turn a manageable tax bill into a financial nightmare. Right now, the underpayment penalty interest rate sits at 7% – that’s higher than many credit cards charge.

Underpayment penalties hit when you don’t pay enough tax throughout the year. If you expect to owe $1,000 or more at filing, you need to make quarterly estimated payments or increase your withholding. The safe-harbor rules I mentioned earlier are your best protection here.

Late filing penalties are particularly brutal – 5% of unpaid taxes per month, up to 25%. Here’s a pro tip: file your return even if you can’t pay the full amount. The late payment penalty is only 0.5% per month, much better than the filing penalty.

Don’t forget about the Alternative Minimum Tax (AMT). While fewer people face AMT after the 2017 tax changes, high earners should still watch for exposure, especially when exercising stock options or claiming large state tax deductions.

When to Seek Professional Tax Planning Advice

Some tax situations are perfect for DIY approaches. Others? Not so much. Knowing when to call in professional help can save you thousands and help you sleep better at night.

Major life events create both opportunities and pitfalls. Getting married, divorced, having children, changing jobs, or retiring all trigger tax implications that aren’t obvious. A professional can help you steer these transitions and avoid costly mistakes.

Business ownership brings complexity that goes way beyond personal tax returns. Entity selection, compensation strategies, and succession planning all require specialized knowledge. The wrong choice early on can cost you for years.

Stock options and equity compensation create unique challenges around timing exercises, managing AMT exposure, and long-term planning. I’ve seen people lose tens of thousands by exercising options at the wrong time.

Real estate investments involve their own maze of rules. Rental property depreciation, 1031 exchanges, and real estate professional status elections can significantly impact your taxes – but only if handled correctly.

Cross-border situations are particularly tricky. Foreign income reporting, international asset disclosure, and expatriation rules carry severe penalties for mistakes. The compliance requirements are complex, and the IRS takes violations seriously.

At Elite Tax Strategy Solutions, we focus on proactive tax planning rather than just compliance. Our approach involves year-round planning to help high earners and business owners maximize their tax savings while staying compliant. Learn more about our Proactive Tax Planning services.

The key is recognizing when your situation has moved beyond basic tax preparation into true tax planning territory. If you’re asking yourself whether you need professional help, you probably do.

Frequently Asked Questions about Tax Planning Advice

What is tax planning advice and why does it matter?

Tax planning advice is professional guidance that helps you legally minimize your tax burden while keeping your financial goals on track. Think of it as having a GPS for your money – instead of wandering around hoping you don’t hit a pothole, you get clear directions to your destination.

Here’s what makes it different from just filing your taxes: tax planning advice looks ahead instead of backward. Your tax preparer deals with what already happened last year. A tax planner helps you make smart moves before they show up on next year’s return.

The numbers speak for themselves. Good planning can save you thousands annually – sometimes tens of thousands if you’re a high earner or business owner. But it’s not just about the money you save. It’s about the stress you avoid when you know you’re handling everything correctly.

Most people think tax planning is just for the wealthy. That’s not true. Whether you’re maxing out your 401(k), timing when to sell investments, or figuring out if you should itemize deductions, you’re already doing tax planning. Professional advice just makes sure you’re doing it well.

When should I seek professional tax planning advice?

The short answer? When your tax situation keeps you up at night or when you suspect you’re leaving money on the table.

Life gets complicated fast. You start with a simple W-2, then suddenly you’re married with kids, own rental property, have stock options, and your brother-in-law wants you to invest in his startup. Each change creates new tax implications.

Here are the big red flags that scream “get professional help”: You’re consistently writing big checks to the IRS at filing time, or you’re getting refunds so large they could fund a vacation. Both situations mean your withholding is off, and that’s just the tip of the iceberg.

Business ownership changes everything. The moment you have employees, multiple income streams, or significant business assets, you need someone who understands the rules. The penalties for getting it wrong aren’t just expensive – they can be business-ending.

Stock options and equity compensation are another major trigger. These create unique tax situations that most people (and many tax preparers) don’t fully understand. The timing decisions alone can save or cost you thousands.

Moving between states or dealing with international income? Don’t even think about handling that yourself. The compliance requirements are complex, and the penalties for mistakes are severe.

How can tax planning advice reduce my investment taxes?

Investment taxes can eat up a huge chunk of your returns if you’re not careful. The good news? Smart planning can dramatically reduce what you owe.

Asset location is one of the most powerful strategies most people never hear about. It’s not just what you invest in – it’s where you hold those investments. Put your tax-hungry investments (like bonds or REITs) in tax-advantaged accounts like your 401(k). Keep your tax-efficient investments (like index funds) in taxable accounts.

Tax-loss harvesting sounds complicated, but it’s actually pretty straightforward. When investments lose value, you sell them to “harvest” the loss. This loss can offset gains from other investments, potentially saving you thousands in taxes. The key is doing it systematically throughout the year, not just scrambling in December.

Timing is everything when it comes to realizing gains and losses. If you’re in a lower tax bracket this year (maybe you took time off or had a career transition), it might make sense to realize some gains while you’re in the 0% capital gains bracket.

For high earners, municipal bonds can be a game-changer. The interest is typically exempt from federal taxes, and if you buy bonds from your home state, you might avoid state taxes too.

The biggest mistake people make is trying to optimize taxes without considering their overall investment strategy. Tax planning advice helps you coordinate everything so you’re not saving pennies on taxes while losing dollars on poor investment decisions.

Conclusion

Smart tax planning advice comes down to one simple truth: it’s not about finding sneaky loopholes or pushing boundaries. Instead, it’s about understanding how the system works and making informed decisions that legally keep more money in your pocket.

The strategies we’ve walked through together can genuinely save you thousands each year. More importantly, they give you peace of mind knowing you’re handling your taxes the right way. No more scrambling at the last minute or wondering if you missed something important.

Here’s what really matters: the best tax planning happens throughout the year, not just when April rolls around. Start with the fundamentals – figure out your actual tax bracket, max out those tax-advantaged accounts, and keep your paperwork organized. Once you’ve got those basics down, you can add more sophisticated moves as your financial picture gets more complex.

The tax world keeps changing, and that’s especially true right now. With the Tax Cuts and Jobs Act provisions ending in 2025, we’re looking at some significant shifts ahead. Taking action now positions you to handle whatever comes next.

At Elite Tax Strategy Solutions, we’ve guided hundreds of high earners and business owners through exactly these kinds of planning decisions. Our clients appreciate our thorough, year-round approach because it means they’re never caught off guard by tax surprises.

The truth is, the best time to start planning was yesterday. The second-best time is right now. Whether you tackle these strategies on your own or partner with a professional, taking that first step today creates benefits that compound for years to come.

Your financial future deserves more than reactive tax preparation. It deserves proactive planning that works with your goals, not against them.

Ready to see what comprehensive planning can do for your specific situation? Our Comprehensive Tax Planning services are designed to give you exactly that kind of personalized guidance.