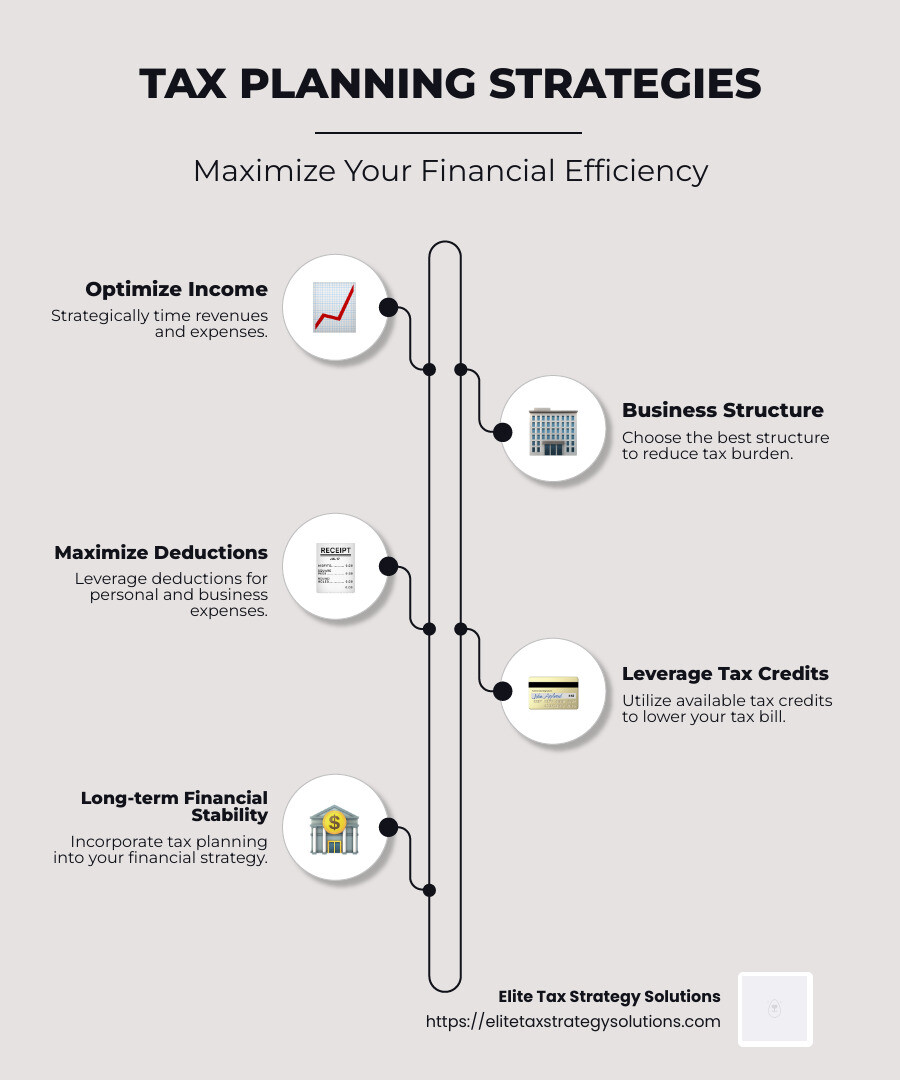

Tax planning strategies are key tools that can pave the way to financial success, whether you’re a high-income earner or a small business owner. Implementing the right strategies can minimize your tax liabilities and maximize your deductions, giving you greater control over your finances. Here’s a quick glimpse at what smart tax planning can do:

- Optimize taxable income by timing revenues and expenses strategically

- Choose the best business structure to reduce overall tax burden

- Maximize deductions for both business and personal expenses

- Leverage tax credits to lower your tax bill

Navigating the complexities of tax regulations might seem daunting, but the payoff is worth it. By incorporating effective tax planning into your financial strategy, you can not only cut down on tax stress but also improve your long-term financial stability.

My name is David Fritch. With 40 years of experience in tax planning and financial advisory, I have dedicated my career to helping clients like you steer complex tax scenarios with ease. At Elite Tax Strategy Solutions, we offer custom tax planning strategies to align with your specific financial goals. Let me guide you through the intricacies of tax planning strategies for optimal financial outcomes.

Tax planning strategies basics:

– Comprehensive tax planning

– Tax management services

– Tax risk management

Understanding Tax Planning Strategies

Tax planning is like a puzzle. To solve it, you need to fit together different pieces—tax efficiency, financial analysis, and retirement plans.

Tax Efficiency:

Imagine having a map to steer the tax maze. That’s what tax efficiency is. It’s about making sure every part of your financial plan works together to pay the least tax possible. It’s not about avoiding taxes but about paying what you owe—no more, no less.

For example, consider strategic income management. This means timing your income and expenses smartly. If you expect to be in a lower tax bracket next year, you might defer some income until then. It’s like shifting your earnings to a time when taxes won’t bite as hard.

Financial Analysis:

Financial analysis is the flashlight that helps you see through the fog of numbers. It involves looking at your entire financial situation—income, expenses, investments—and figuring out where you can save on taxes.

Consider business structure optimization. Are you a sole proprietor? Maybe switching to an LLC or S Corporation could save you money. Each business setup has different tax perks and pitfalls. A good analysis will show you the best path.

Retirement Plans:

Retirement plans are like planting seeds for your future. Contributing to plans like a traditional IRA or a 401(k) can reduce your taxable income now, while your savings grow tax-deferred. For instance, in 2023, you could contribute up to $6,500 to an IRA, lowering your taxable income by that amount.

And don’t forget about tax gain-loss harvesting. This is a strategy where you sell investments at a loss to offset gains elsewhere. It’s like balancing a scale, so you end up paying less tax on your investment earnings.

By understanding these tax planning strategies, you can make informed decisions that align with your financial goals. It’s about being proactive, not reactive. And remember, the tax landscape changes often, so staying updated is crucial.

Next, we’ll dive into how these strategies apply specifically to individuals and businesses.

Top Tax Planning Strategies for Individuals

When it comes to tax planning for individuals, there are several key strategies that can help you minimize your taxable income and maximize your savings. Let’s break down some of the most effective tax planning strategies for individuals.

Income Reduction

Reducing your taxable income is a fundamental part of tax planning. One way to achieve this is by contributing to retirement accounts. For instance, putting money into a 401(k) or traditional IRA can significantly lower your taxable income. In 2024, you can contribute up to $23,000 to a 401(k), and if you’re 50 or older, you can add an extra $7,500. This means less income is subject to taxes now, while your retirement savings grow over time.

Another way to reduce income is through strategic income management. This involves timing your income and expenses to fall in years when you’re in a lower tax bracket. For example, if you expect a pay cut or a job change that will lower your income next year, consider deferring some income to that year.

Tax Deductions

Tax deductions are expenses you can subtract from your taxable income, reducing the amount of income that is subject to tax. These include things like mortgage interest, student loan interest, and charitable donations. If you’re self-employed, you can also deduct home office expenses and business-related travel costs.

A clever technique is bunching deductions, where you combine deductible expenses into one tax year to exceed the standard deduction threshold. This way, you can itemize in one year and take the standard deduction the next, maximizing your tax savings over time.

Tax Credits

Tax credits are even more valuable than deductions because they reduce your tax bill dollar-for-dollar. Some common credits include the Earned Income Tax Credit (EITC) and the Child Tax Credit. Unlike deductions, credits directly decrease the amount you owe, making them a powerful tool in your tax strategy.

For business owners, there are specific credits like the Work Opportunity Tax Credit, which can provide significant savings. Make sure to explore all available credits to ensure you’re not leaving money on the table.

Retirement Accounts

Retirement accounts are not just for saving for the future—they’re also a smart tax strategy. Contributions to traditional IRAs and 401(k)s can lower your taxable income now. Meanwhile, Roth IRAs offer tax-free withdrawals in retirement, which can be beneficial if you expect to be in a higher tax bracket later.

You have until the tax deadline to make contributions for the previous year, giving you extra time to plan and maximize your tax benefits.

By focusing on these tax planning strategies, you can effectively manage your finances and work towards a more secure financial future. Each strategy requires careful consideration and planning, but the potential savings make it worth the effort.

Next, we’ll explore how businesses can leverage similar strategies to optimize their tax outcomes.

Tax Planning Strategies for Businesses

Businesses, like individuals, can benefit greatly from strategic tax planning strategies. Here’s how you can optimize your business’s tax situation through careful planning.

Business Structure

Choosing the right business structure is crucial. Whether you’re a sole proprietorship, partnership, LLC, S corporation, or C corporation, each structure has its own tax implications.

For example, an LLC offers flexibility and can be taxed as a sole proprietorship, partnership, or corporation. This can help reduce self-employment taxes. An S corporation can provide tax benefits by allowing you to pay yourself a salary and take the rest as dividends, potentially lowering your overall tax burden. Periodically review your business structure to ensure it aligns with your financial goals.

Income Management

Strategic income management involves timing your revenue and expenses to optimize your tax position. If you anticipate being in a lower tax bracket next year, consider deferring income to that year. Conversely, if you expect higher taxes in the future, you might accelerate income and defer expenses.

For instance, if you own a consulting business, you could delay invoicing until January to push income into a lower-tax year. This kind of planning can significantly impact your tax liability.

Deductions

Maximizing deductions is a fundamental tax planning strategy for businesses. Track and document all eligible business expenses carefully. This includes office supplies, travel expenses, and even the mileage on your business vehicle.

Consider using the bunching strategy for deductions. By grouping expenses into one year, you can exceed the standard deduction and itemize, leading to greater tax savings.

Tax Credits

Tax credits are powerful tools for reducing your tax liability. Unlike deductions, which lower your taxable income, credits reduce your tax bill directly.

Explore credits related to business activities, such as the Work Opportunity Tax Credit or the Disabled Access Credit. These can provide substantial savings. It’s important to understand and leverage these credits effectively to ensure you’re maximizing your tax benefits.

By focusing on these tax planning strategies, businesses can optimize their tax outcomes and improve their financial health. Next, we’ll dig into advanced tax techniques that can further refine your tax strategy.

Advanced Tax Techniques

When it comes to refining your tax strategy, advanced techniques can play a crucial role. Let’s explore some of these strategies: capital gains, tax-loss harvesting, Roth conversion, and charitable contributions.

Capital Gains

Capital gains occur when you sell an asset for more than you paid for it. Managing these gains effectively can help reduce your tax bill. Long-term capital gains (from assets held for over a year) are taxed at a lower rate than short-term gains. This means holding onto investments for the long term can be beneficial.

For instance, if you have $10,000 in long-term capital gains and $10,000 in long-term capital losses, the losses can offset the gains, resulting in no tax liability for that year. The IRS allows you to offset up to $3,000 of capital losses against ordinary income each year, with the remainder carried forward to future years.

Tax-Loss Harvesting

Tax-loss harvesting is a strategy where you sell investments that have declined in value to offset gains elsewhere in your portfolio. This can help reduce your taxable income. However, be cautious of the wash sale rule. This rule disallows the tax deduction if you buy the same or a “substantially identical” investment within 30 days before or after the sale.

Imagine you have a stock that has decreased in value. By selling it at a loss, you can use that loss to offset other gains. If you want to stay invested, consider purchasing a similar, but not identical, stock to avoid the wash sale rule.

Roth Conversion

Converting a traditional IRA to a Roth IRA can be a strategic move, especially if your assets have declined in value. During a Roth conversion, you pay taxes on the converted amount now, potentially at a lower rate if your asset values are down. Future withdrawals from the Roth IRA will be tax-free, allowing any appreciation to grow tax-free.

For example, if you convert when your IRA balance is low, you may pay less in taxes. Plus, any future growth in the Roth IRA won’t be taxed upon withdrawal, providing a long-term tax advantage.

Charitable Contributions

Donating to charity can also be a strategic tax move. If you itemize deductions, charitable contributions can reduce your taxable income. Consider bunching your charitable donations into one year to exceed the standard deduction threshold and maximize your tax benefits.

For instance, if you typically give $5,000 annually, you might give $10,000 every other year. This way, you can itemize in the year you bunch your donations and take the standard deduction in the alternate years.

These advanced tax planning strategies can significantly impact your financial success. Next, we’ll address some frequently asked questions about tax planning strategies.

Frequently Asked Questions about Tax Planning Strategies

What are the three basic strategies to use in planning for taxes?

When planning for taxes, there are three basic strategies you should consider:

-

Income Reduction: Lowering your taxable income is a key strategy. You can do this by contributing to retirement accounts like a 401(k) or an IRA. These contributions can reduce your taxable income today and help you save for the future.

-

Deductions: Deductions reduce the amount of your income that’s subject to tax. Common deductions include mortgage interest, student loan interest, and medical expenses. Keep track of your expenses and consult a tax professional to maximize your deductions.

-

Tax Credits: Credits directly reduce the amount of tax you owe, making them very valuable. Look into credits like the Earned Income Tax Credit or the Child Tax Credit to see if you qualify. These can significantly decrease your tax bill.

How do LLC owners avoid taxes?

LLC owners often use the pass-through entity structure to avoid double taxation. Here’s how it works:

-

Pass-Through Entity: Profits from the LLC are passed directly to the owners’ personal tax returns. This means the business itself isn’t taxed, only the individual owners are. This avoids the double taxation that C corporations face.

-

S Corporation Election: LLCs can choose to be taxed as an S Corporation. This allows owners to take a salary and receive dividends. The salary is subject to payroll taxes, but dividends are not. This can reduce overall tax liability.

Both strategies can help LLC owners minimize their taxes while keeping the business structure flexible. Consulting with a tax advisor can help determine which option is best for your specific situation.

What is a qualified tax planning strategy?

A qualified tax planning strategy is one that aligns with your long-term financial objectives and considers your unique financial situation. Here are some key elements:

-

Long-term Objectives: Your tax strategy should support your broader financial goals, whether it’s saving for retirement, buying a home, or funding education. Align your tax moves with these goals for maximum benefit.

-

Financial Considerations: Consider your current and expected future income, potential changes in tax laws, and your risk tolerance. These factors will influence the best strategies for you.

-

Expert Guidance: Tax laws change frequently, so working with a professional can ensure your strategy remains effective and compliant.

These strategies are about more than just saving money today; they’re about setting yourself up for financial success in the future. By understanding and implementing these tax planning strategies, you can work towards achieving your financial goals.

Conclusion

At Elite Tax Strategy Solutions, we believe that proactive tax optimization is key to achieving financial stability. Our team is dedicated to helping clients steer the complexities of tax regulations with personalized strategies custom to their unique needs.

Tax planning is not just about reducing your tax bill today—it’s about setting the stage for long-term financial success. By implementing tax planning strategies like income reduction, maximizing deductions, and utilizing tax credits, you can effectively manage your tax liabilities while working towards your financial goals.

Our approach is thorough and proactive. We stay ahead of changes in tax laws and economic conditions to ensure our clients are always in the best position. Whether you’re a high-income earner or a small business owner, our services are designed to align with your broader financial objectives.

For those looking to optimize their tax situation, consider seeking expert guidance. Our team is here to provide the insights and strategies you need to make informed decisions. By integrating tax planning with your overall financial strategy, you can achieve greater stability and success.

Explore how our services can benefit you by visiting our Tax Planning for Small Businesses page, and take the first step towards a more secure financial future.