The True Cost of Taxes on Your Investments

Tax-efficient investments are investments that minimize your tax burden, helping you keep more of your returns. Understanding these strategies can significantly impact your wealth over time.

Quick Guide to Tax-Efficient Investing:

| Strategy | Tax Benefit | Best For |

|---|---|---|

| Index ETFs | Low turnover, minimal capital gains distributions | Taxable accounts |

| Municipal bonds | Federal tax-exempt interest, potentially state tax-exempt | High tax brackets |

| Tax-managed funds | Actively minimize distributions and taxable events | Long-term investors |

| Health Savings Accounts | Triple tax advantage: deductible contributions, tax-free growth, tax-free withdrawals | Medical expenses |

| 529 Plans | Tax-free growth for education expenses | College/K-12 savings |

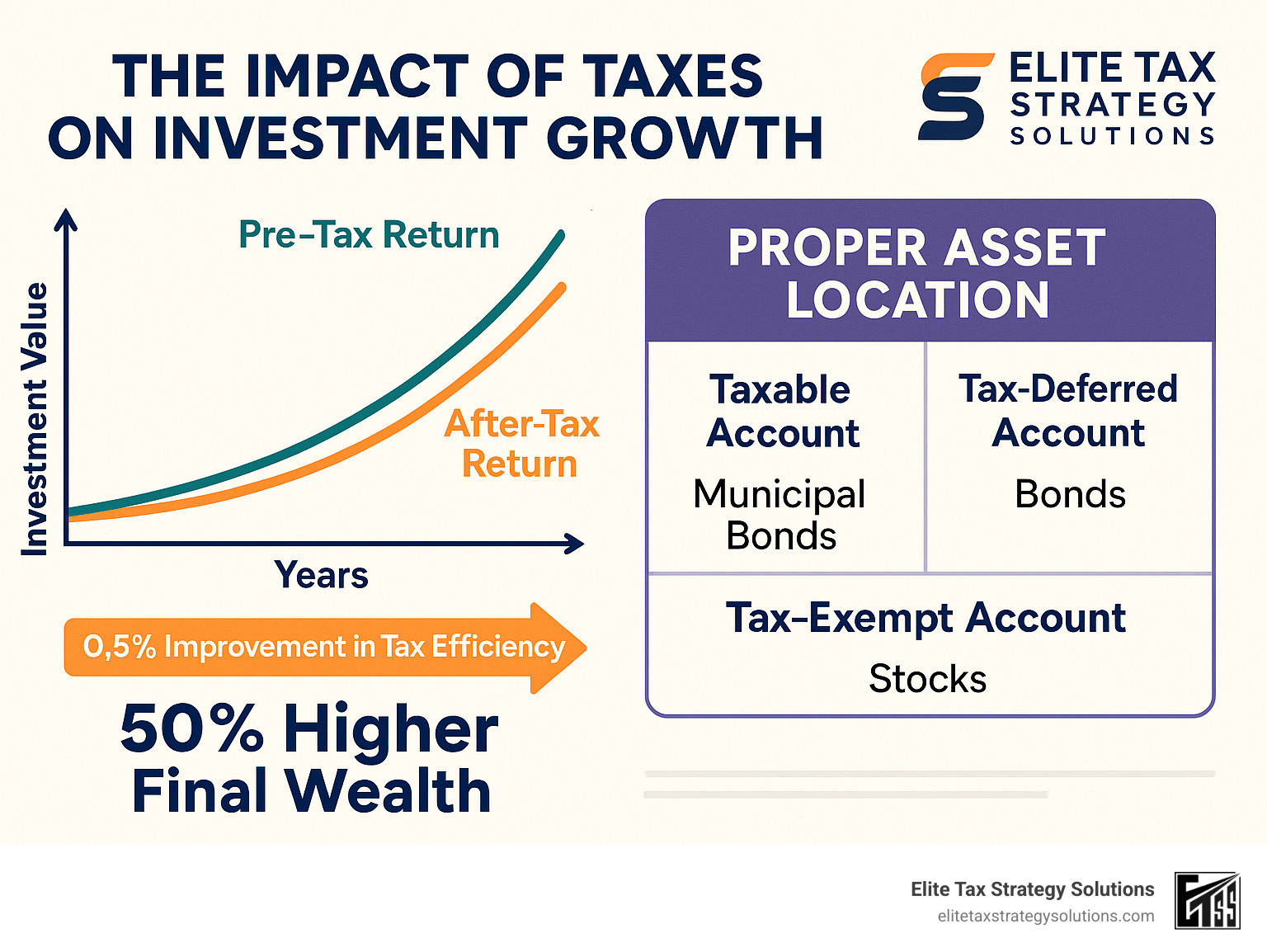

Every investment has costs, but taxes can sting the most. Studies show that the average U.S. equity mutual fund loses about 1.8% of its annual return to taxes. Over decades, this tax drag can reduce your final wealth by 50% or more.

Think about that: half your potential retirement savings could end up going to the government simply because of tax-inefficient investing choices.

Why is this happening? Because many investors focus exclusively on pre-tax returns while ignoring the impact of:

- Short-term capital gains (taxed up to 40.8%)

- Ordinary income from interest (taxed up to 37%)

- Dividend distributions (taxed up to 23.8%)

- Account location mistakes (putting the wrong investments in the wrong accounts)

I’m David Fritch, a CPA with over 40 years of experience helping clients implement tax-efficient investments to maximize their wealth, including 20 years as a Registered Investment Advisor specializing in tax-optimized portfolio strategies.

Key terms for tax-efficient investments:

– tax-efficient estate planning

– advanced tax strategies

– maximize tax savings

Understanding the Foundations of Tax-Efficient Investing

When it comes to growing your wealth, it’s not just about what you earn—it’s about what you keep. That’s where tax-efficient investing comes into play. Think of it as smart money management that helps you hang onto more of your hard-earned returns instead of sending them to Uncle Sam.

The math behind tax efficiency is straightforward but eye-opening. Imagine two investments: Fund A earns 10% but loses 3% to taxes, while Fund B earns 9% but only loses 1% to taxes. Which is better? Fund B actually puts more money in your pocket with its 8% after-tax return compared to Fund A’s 7%.

Now, let’s talk about the magic of compounding. Over 30 years, money growing at 7% annually will multiply about 7.6 times. Bump that up to 8%, and you’ll see it grow 10 times—that’s 32% more money in your retirement fund! Small tax savings today can mean a dramatically different lifestyle tomorrow.

Different types of investment income face very different tax treatments:

– Interest and short-term gains get taxed like your paycheck—up to a whopping 37%

– Qualified dividends and long-term gains enjoy lower rates of 0%, 15%, or 20%

– If you’re a high earner, add another 3.8% Medicare surtax on investment income

“I’ve seen clients shocked when they realize they could have hundreds of thousands more in retirement just by being tax-smart with their investments,” says our senior advisor at Elite Tax Strategy Solutions. “It’s often the missing piece in their financial puzzle.”

What Are Tax-Efficient Investments and Why Do They Matter?

Tax-efficient investments work hard to keep the tax collector’s hands out of your pockets. They do this in several clever ways:

They don’t churn through holdings constantly, triggering taxable events. They favor income that gets preferential tax treatment. Some, like ETFs, have structural advantages over their mutual fund cousins. Others, like municipal bonds, offer income that’s partially or completely tax-exempt.

Why should you care? Because while you can’t control market ups and downs, you absolutely can control how taxes impact your returns. It’s one of the few guaranteed ways to improve your investment performance.

Here’s a real-life wake-up call: A client in the top tax bracket held a well-performing large-blend mutual fund for a decade. Despite never selling a single share, they lost about 13% of their total return to taxes! This happened simply because the fund had to distribute gains and income each year.

There’s also a wonderful behavioral benefit to tax-efficient investing. When you understand the tax bite that comes from frequent trading, you’re more likely to stay the course with your investments—and patient investors historically earn better returns than those who constantly jump in and out of the market.

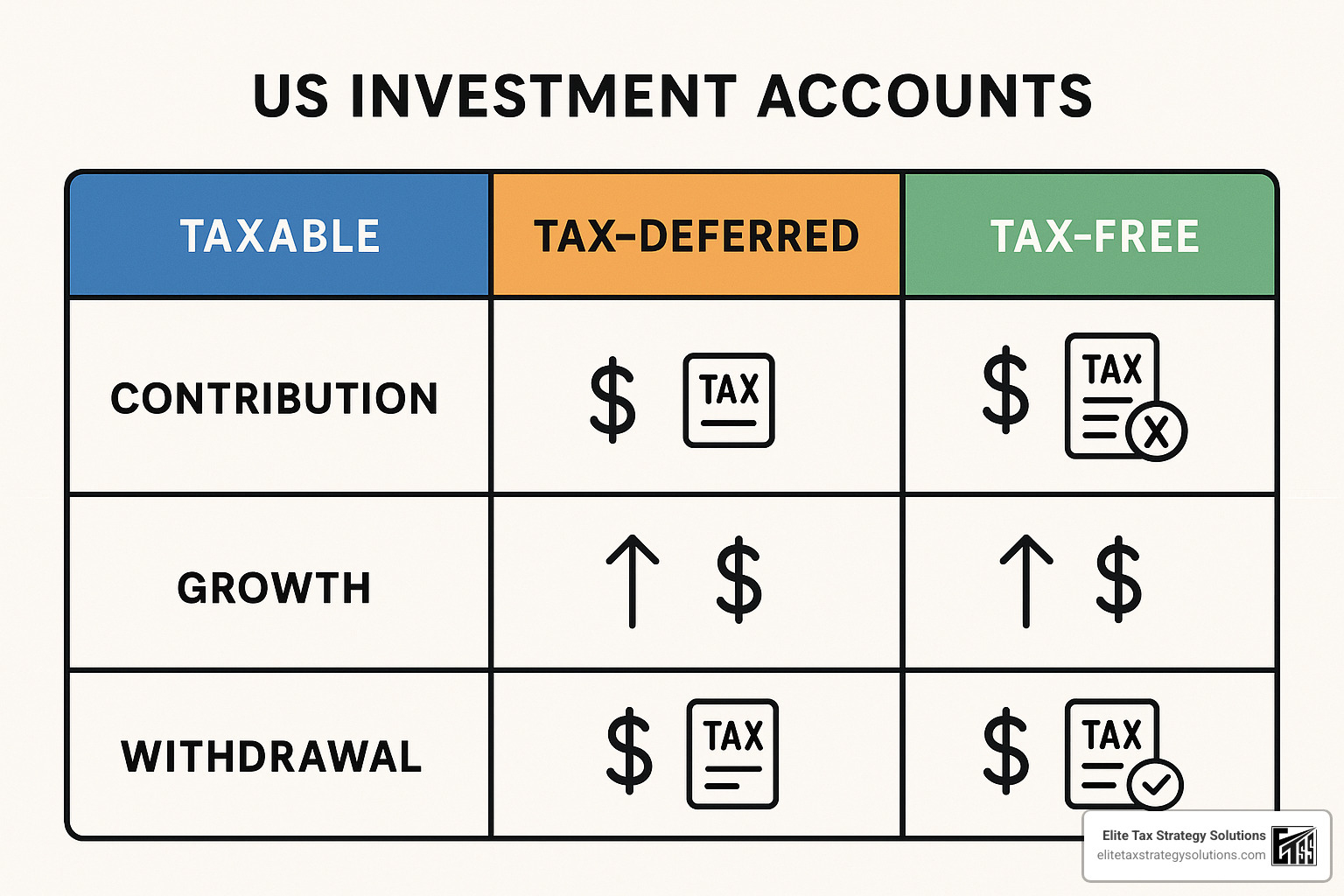

Comparing Account Types: Taxable, Tax-Deferred, Tax-Free

Where you hold your investments matters just as much as what you invest in. Let’s explore your main options:

Taxable Accounts (Brokerage)

These everyday investment accounts offer flexibility but no special tax breaks. You fund them with after-tax dollars, pay taxes on dividends and interest annually, and owe capital gains tax when you sell winners. The silver linings? No contribution limits, no withdrawal penalties, and heirs get a “step-up” in basis at your death (potentially wiping out years of gains for tax purposes).

Tax-Deferred Accounts (Traditional IRA, 401(k))

These retirement workhorses let you invest with pre-tax dollars, giving you an immediate tax break. Your money grows without annual tax bills, but eventually, you’ll pay ordinary income tax on every dollar you withdraw. For 2024, you can contribute up to $23,000 to a 401(k) ($30,500 if you’re 50+) and $7,000 to an IRA ($8,000 if 50+). Just remember that Required Minimum Distributions kick in at age 73.

Tax-Free Accounts (Roth IRA, Roth 401(k))

The darlings of the tax planning world, Roth accounts offer no upfront tax break but provide completely tax-free growth and withdrawals in retirement. They have the same contribution limits as their traditional counterparts. Roth IRAs have no RMDs during your lifetime, while Roth 401(k)s do unless you roll them over to a Roth IRA.

“Choosing the right account type is like picking the perfect soil for different plants,” explains our tax planning team. “Each account creates a unique tax environment where certain investments will flourish better than others.”

By understanding these tax foundations, you’re already ahead of most investors. The next step is learning which specific investments work best in each account type—and that’s exactly what we’ll cover in the following sections.

Top Tax-Efficient Investments for Taxable Accounts

When it comes to investing in taxable accounts, not all investments are created equal. Some options are naturally more tax-friendly than others, helping you keep more of your hard-earned returns. Let’s explore the investments that can help minimize your tax burden while maximizing your after-tax wealth.

Index Funds & ETFs as Tax-Efficient Investments

If you’re looking for truly tax-efficient investments, index funds and ETFs should be at the top of your list, especially for taxable accounts. Their tax advantages come from several smart design features:

Index funds follow a “buy and hold” approach by simply tracking market indexes rather than trying to beat them. This results in much lower turnover—meaning fewer buy and sell transactions that trigger capital gains. While active managers might completely reshape their portfolios annually, most index funds make only minimal adjustments.

“The difference in tax bills can be striking,” notes one of our clients who switched from active funds to ETFs. “My annual investment-related tax bill dropped by nearly 40% after making the switch, and ironically, my returns actually improved!”

ETFs take tax efficiency even further through their unique structure. When investors sell ETF shares, they’re typically selling to other investors on an exchange—not redeeming from the fund itself. This means the fund rarely needs to sell underlying securities to meet redemptions, avoiding the capital gains that mutual funds often distribute to all shareholders.

Morningstar research consistently shows that index funds and ETFs have significantly lower tax-cost ratios compared to actively managed funds. This means more of your return stays in your pocket rather than going to the IRS.

Vanguard cleverly patented a unique “ETF share class” structure that extends these tax benefits to their traditional index funds, making them particularly attractive options for tax-conscious investors.

For deeper understanding of how these funds work, the SEC provides comprehensive information on mutual funds, including their tax treatment.

Municipal Bonds and Bond Funds for High Brackets

For investors in higher tax brackets, municipal bonds offer a compelling tax advantage: interest income that’s generally exempt from federal income taxes. If you buy bonds issued by your home state, that interest is typically exempt from state and local taxes too—a true “triple-tax-free” investment.

To properly evaluate municipal bonds against their taxable counterparts, you need to calculate the “tax-equivalent yield”:

Tax-Equivalent Yield = Tax-Free Yield ÷ (1 – Your Federal Tax Rate)

For example, if a muni bond yields 3% and you’re in the 37% federal tax bracket, its taxable equivalent would be 4.76%—meaning a taxable bond would need to yield nearly 5% to match the muni’s after-tax return!

“Municipal bonds often look unimpressive until you factor in their tax benefits,” explains our fixed-income specialist. “For clients in the 32% bracket or higher, munis frequently outperform taxable bonds on an after-tax basis, despite their seemingly lower yields.”

Be aware that some municipal bond interest may be subject to the Alternative Minimum Tax (AMT), and bond quality varies significantly between issuers. Municipal bond funds offer convenient diversification but may include bonds from multiple states, potentially diluting state tax benefits.

For comprehensive information about municipal bonds and their tax treatment, visit Investor.gov’s bond resource page.

Treasuries, I Bonds, and Series EE Bonds

U.S. Treasury securities offer another avenue for tax-smart fixed income investing, with their own unique advantages:

Treasury Bonds, Notes, and Bills generate interest that’s exempt from state and local taxes (though still subject to federal tax). This makes them particularly attractive for residents of high-tax states like California, New York, or New Jersey.

I Bonds are currently one of the most compelling tax-efficient investments available. They’re currently paying 5.27% (as of 2024), with interest that’s exempt from state and local taxes. Even better, you can defer federal taxes until redemption—potentially decades later. They also offer inflation protection by adjusting their rates semi-annually based on CPI changes.

“I recommended that a client move her emergency fund from a high-yield savings account to I Bonds,” shares one of our advisors. “Not only did she earn a higher rate, but she saved on state taxes and deferred federal taxes for years—significantly enhancing her overall return.”

I Bonds can be purchased electronically through TreasuryDirect.gov (up to $10,000 per person annually) and up to an additional $5,000 in paper form through your tax refund.

Series EE Bonds offer a unique guarantee: they double in value if held for 20 years, equivalent to a 3.5% annual return. They enjoy the same tax advantages and purchase limits as I Bonds, making them worth considering for long-term goals.

Tax-Managed Funds & Personalized Indexing

For investors seeking more sophisticated tax management, tax-managed funds and personalized indexing solutions represent the cutting edge of tax-efficient investments.

Tax-managed funds are actively managed with tax efficiency as a primary objective. Their managers employ various techniques to minimize tax impact: they keep turnover low, strategically harvest losses to offset gains, favor stocks with qualified dividends, and carefully choose which specific shares to sell when rebalancing.

While these funds typically have higher expense ratios than index funds, their tax savings can more than make up the difference for investors in higher tax brackets.

Direct indexing (also called personalized indexing) takes tax efficiency to an entirely new level. Instead of buying a fund that tracks an index, you own the individual stocks directly, enabling personalized tax management:

“Direct indexing can harvest tax losses that are 1-2% higher annually than what’s possible with ETFs alone,” explains our investment team. “For our high-income clients, this extra tax alpha can offset capital gains from other investments or even reduce ordinary income by up to $3,000 annually.”

Beyond tax-loss harvesting, direct indexing allows you to exclude specific companies based on your values, transition tax-efficiently from concentrated positions, and optimize charitable giving with appreciated securities.

These sophisticated strategies are becoming increasingly accessible to more investors thanks to technology improvements and reduced trading costs. To learn more about implementing these advanced approaches, visit our Tax Optimization Strategies page.

Proven Strategies to Slash Your Investment Tax Bill

Looking to keep more of your investment returns? Beyond just choosing tax-friendly investments, how you manage your portfolio can dramatically reduce what you owe Uncle Sam. Let me share some strategies that have helped our clients save thousands in taxes each year:

Asset Location of Tax-Efficient Investments

Think of asset location as giving each investment its perfect home. It’s not about changing what you own—just where you keep it to minimize taxes.

The basic recipe works like this:

– Keep your tax-inefficient investments (like bonds, REITs, and active funds) in tax-advantaged accounts

– Place your tax-efficient investments (index ETFs, municipal bonds) in taxable accounts

– Save your Roth accounts for investments with the highest growth potential

I like to explain this to clients using a simple framework:

First, decide on your overall investment mix (maybe 60% stocks, 40% bonds). Then, categorize each investment by how tax-friendly it is. Fill your IRAs and 401(k)s with your least tax-efficient holdings first. For international stocks, consider keeping them in taxable accounts to claim the foreign tax credit. Your Roth accounts are perfect for investments you expect to grow the most. Finally, use your taxable accounts for anything that’s naturally tax-efficient.

I remember working with a couple who had a $1 million portfolio split between stocks and bonds, with $600,000 in a taxable account and $400,000 in IRAs. By simply moving all their bonds to the IRAs and keeping only stock ETFs in their taxable account, we boosted their after-tax return by about 0.4% annually. That small change could add over $200,000 to their retirement savings over 20 years!

For a deeper dive into this strategy, the Bogleheads wiki on tax-efficient fund placement is an excellent resource.

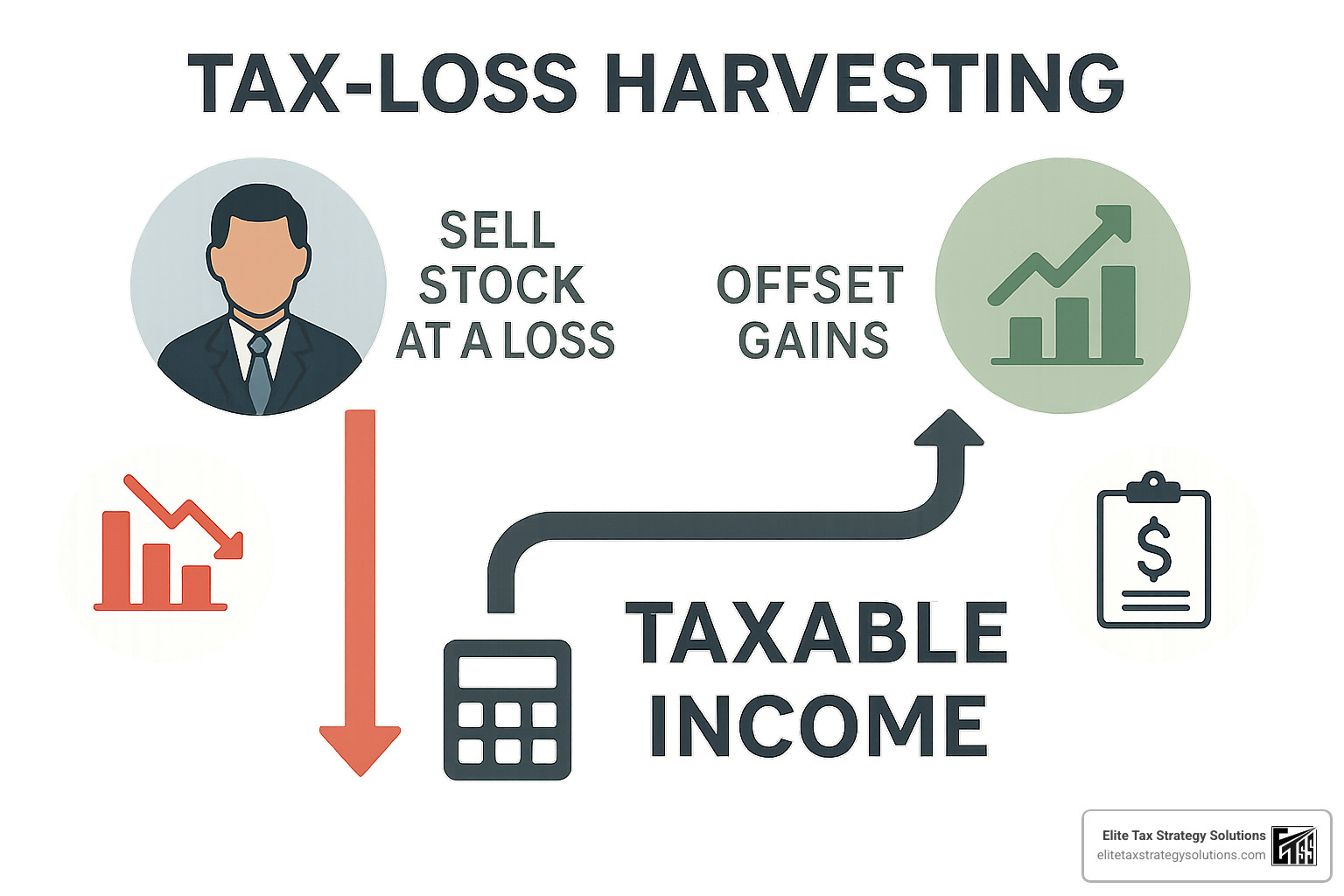

Year-Round Tax-Loss Harvesting Essentials

Tax-loss harvesting is like finding silver linings in market downturns. When investments drop in value, you can sell them to realize losses that offset capital gains and up to $3,000 of ordinary income each year. Any leftover losses can be carried forward indefinitely—like a tax-savings coupon that never expires.

Just watch out for the wash-sale rule! If you buy a “substantially identical” investment within 30 days before or after selling at a loss, the IRS won’t let you claim that loss. To stay invested while avoiding this trap, you might sell an S&P 500 fund and buy a total market fund instead.

While many investors only think about harvesting losses in December, market dips throughout the year create opportunities. I recommend checking quarterly for harvesting possibilities. Many robo-advisors now offer this service automatically, monitoring for opportunities daily.

One of my favorite client success stories involved harvesting over $45,000 in losses during a market correction last year. Those losses offset gains from a business sale, saving approximately $10,000 in taxes immediately, with plenty left over for future years.

Long-Term vs Short-Term: Holding Period Implications

Patience pays when it comes to investment taxes. The difference between short-term and long-term capital gains rates is dramatic:

If you hold investments for a year or less, gains are taxed at ordinary income rates—up to 37%, plus the 3.8% Medicare surtax for high earners. That’s a potential tax bite of 40.8%!

But hold those same investments for just over a year, and the maximum tax rate drops to 23.8% (20% plus the 3.8% surtax). Even better, if your taxable income is under $44,625 (single) or $89,250 (married filing jointly) in 2024, you might qualify for the 0% long-term capital gains rate.

I tell clients to imagine a clock attached to every investment. When that clock hits 366 days, your potential tax rate nearly halves. This mental image helps resist the urge to trade frequently—which is usually better for your returns anyway!

Charitable Giving with Appreciated Securities

If you’re charitably inclined, giving appreciated securities instead of cash is like getting an extra tax break for free.

Here’s how it works: Instead of selling a long-term appreciated stock and donating the cash, give the stock directly to charity. You’ll get a tax deduction for the full market value and completely avoid capital gains tax on the appreciation.

For example, let’s say you want to donate $10,000 to your favorite charity. You could give cash, or you could donate stock worth $10,000 that you bought years ago for $4,000. By donating the stock:

– You get the same $10,000 charitable deduction

– You avoid paying capital gains tax on the $6,000 gain

– The charity still receives the full $10,000 value

Donor-Advised Funds (DAFs) offer even more flexibility. You can contribute appreciated assets now for an immediate tax deduction, then recommend grants to charities over time. This is particularly useful for “bunching” multiple years of donations in high-income years.

For those over 70½, Qualified Charitable Distributions (QCDs) allow you to transfer up to $100,000 annually directly from an IRA to qualified charities. This counts toward your Required Minimum Distribution but isn’t included in your taxable income—a better deal than taking the distribution and then donating.

One of my clients saved over $35,000 in taxes by donating highly appreciated stock to establish a donor-advised fund during a particularly high-income year. This maximized their itemized deduction when it provided the most value, while supporting their favorite charities over several years.

For more sophisticated charitable strategies, check out our Advanced Tax Planning Strategies page.

Special Accounts for Ultra Tax Efficiency

When it comes to supercharging your tax efficiency, certain specialized accounts offer benefits that go beyond what traditional investment accounts can provide. Let’s explore these powerful options that could potentially save you thousands in taxes over your lifetime.

Health Savings Accounts: Triple Tax Advantage

I like to call Health Savings Accounts (HSAs) the “unicorns” of the tax world because they offer something truly magical: a triple tax advantage that you simply won’t find anywhere else.

Here’s what makes HSAs so special:

- Tax-deductible contributions that reduce your current taxable income

- Tax-free growth on all investments inside the account

- Tax-free withdrawals for qualified medical expenses at any time

For 2024, you can contribute up to $4,150 for individual coverage ($5,150 if you’re 55 or older) or $8,300 for family coverage ($9,300 if you’re 55+).

To qualify for this tax trifecta, you’ll need to be enrolled in a high-deductible health plan with a minimum deductible of $1,600 for individuals or $3,200 for families, and maximum out-of-pocket limits of $8,050 (individual) or $16,100 (family).

Here’s an insider tip that many people miss: While HSAs are designed for healthcare costs, they have a secret identity as stealth retirement accounts. Once you turn 65, you can withdraw HSA funds for any purpose by simply paying ordinary income tax—just like a traditional IRA—with no penalties.

“We often see clients paying medical bills out-of-pocket while letting their HSA investments grow tax-free,” says our healthcare planning specialist. “One client accumulated over $80,000 in his HSA over ten years, creating a tax-free medical expense fund for retirement when healthcare costs typically skyrocket.”

529 College & K-12 Savings Plans

As a parent or grandparent, few things feel better than helping the young people in your life get a great education. 529 plans make this financially smarter with impressive tax benefits:

Your contributions grow completely tax-free when used for qualified education expenses. Many states also offer immediate tax deductions or credits for your contributions—like getting an instant return on your investment.

The flexibility of these plans might surprise you. You can change beneficiaries within your family if one child doesn’t need all the funds, and you can now use up to $10,000 per year for K-12 tuition, not just college expenses.

For those with substantial means, 529 plans offer an attractive gift tax advantage: you can front-load five years of gifts at once—up to $85,000 per beneficiary in 2024—without affecting your lifetime gift tax exemption.

Recent legislation has made 529 plans even more versatile:

– Unused 529 funds can now be rolled over to Roth IRAs (subject to certain limits)

– Qualified expenses have expanded to include registered apprenticeship programs

– You can use up to $10,000 (lifetime limit) for student loan repayment

One of our clients at Elite Tax Strategy Solutions leveraged their state’s generous 529 tax credit program and effectively received a 20% immediate return on their education savings. By maximizing contributions for their three grandchildren, they saved over $3,000 in state taxes while building tax-free education funds—a true win-win.

Managing RMDs and Roth Conversions

Retirement account planning isn’t just about accumulation—it’s also about smart distribution strategies that can save you thousands in taxes.

Thanks to the SECURE 2.0 Act, Required Minimum Distributions (RMDs) now begin at age 73 (up from 72), and this age will increase to 75 in 2033. These mandatory withdrawals apply to traditional IRAs, 401(k)s, and other tax-deferred accounts. Missing an RMD can be costly—the penalty is 25% of the amount you should have withdrawn.

One powerful strategy to reduce future RMDs is strategic Roth conversions. By converting traditional IRA assets to Roth IRAs, you’re essentially choosing to pay taxes now at current rates rather than gambling on what future tax rates might be. This creates multiple benefits:

Tax-free growth continues inside your Roth account for as long as you want (no RMDs!), tax-free withdrawals give you more flexibility in retirement, and your heirs will receive a tax-free inheritance if they inherit your Roth IRA.

At Elite Tax Strategy Solutions, we use what we call a Break-Even Tax Rate (BETR) analysis to determine if Roth conversions make mathematical sense for each client’s unique situation.

“We look for windows of opportunity,” explains our retirement specialist. “For instance, we worked with a couple who retired at 62 but wouldn’t start Social Security until 67. Those five years represented a golden opportunity for partial Roth conversions at lower tax brackets. By strategically filling up the 12% and 22% brackets during those years, we estimated lifetime tax savings of approximately $120,000.”

This approach, called “income smoothing,” is like filling potholes in your tax road—using low-income years to absorb taxable events that would otherwise hit you when your income is higher.

Common Mistakes That Sabotage Tax Efficiency

We’ve all been there—making well-intentioned investment decisions that end up costing us at tax time. After helping thousands of clients optimize their portfolios, I’ve seen the same tax pitfalls trip up even sophisticated investors time and again.

Excessive trading and turnover is perhaps the most common misstep. That temptation to frequently buy and sell can trigger short-term capital gains taxed at your higher ordinary income rates—potentially more than 40% for high earners! Morningstar research confirms what we see in practice: investor returns often trail fund returns by 1-2% annually, largely due to poorly timed trades with nasty tax consequences.

“I remember one client who thought he was being proactive by frequently adjusting his portfolio,” shares our senior advisor. “When we analyzed his tax returns, we finded he’d paid over $12,000 in unnecessary taxes from short-term gains. Simply adopting a buy-and-hold strategy with tax-efficient investments like index ETFs dramatically improved his after-tax returns.”

The “buying the dividend” mistake catches many investors by surprise. Purchase a mutual fund just before its distribution date, and you’ll immediately receive a taxable distribution—even though the fund’s share price drops by the same amount. You’re essentially prepaying taxes on someone else’s gains! Always research distribution schedules before making purchases in taxable accounts, especially during December when year-end distributions are common.

Asset location errors can silently drain your returns for years. I’ve seen countless portfolios with bonds sitting in taxable accounts while index ETFs occupy IRAs—exactly backward from optimal placement. The solution isn’t complicated: follow proper asset location principles by keeping tax-inefficient investments (bonds, REITs, high-turnover funds) in IRAs while holding tax-efficient ETFs and municipal bonds in taxable accounts.

Speaking of municipal bonds, placing them in IRAs is a surprisingly common mistake that completely negates their tax advantage. Since traditional IRA withdrawals are taxed as ordinary income regardless of what generated that money, the tax-exempt nature of municipal bond interest is completely wasted. Always hold municipal bonds exclusively in taxable accounts.

State and local taxes often fly under the radar. While investors focus on federal tax implications, state taxes can add significantly to your overall burden. This is especially true in high-tax states like California, New York, and New Jersey, where combined rates can approach 50%. Consider state tax treatment when selecting investments and account types—strategies like in-state municipal bonds can provide meaningful savings.

“One new client came to us after realizing they had been holding municipal bonds in their IRA for years while their taxable account was full of high-turnover, high-dividend funds,” recalls our tax planning team. “Simply swapping these positions improved their tax efficiency dramatically without changing their overall asset allocation.”

While tax-loss harvesting gets plenty of attention, neglecting strategic gain harvesting can be equally costly. Investors in the 0% long-term capital gains bracket (taxable income under $44,625 single/$89,250 married in 2024) can realize gains completely tax-free—essentially resetting their cost basis. Similarly, those with carryover losses can strategically realize gains that won’t increase their tax bill.

The foreign tax credit oversight is particularly frustrating for us to see. When you hold international investments in taxable accounts, you may qualify for a U.S. tax credit for foreign taxes paid. This valuable credit is completely lost when these investments are held in IRAs. For many investors, holding international funds in taxable accounts makes more mathematical sense despite the dividend taxation.

The good news? Most of these mistakes can be corrected with thoughtful portfolio restructuring. At Elite Tax Strategy Solutions, we regularly identify and remedy these issues through our comprehensive portfolio reviews—often finding tax savings that more than cover our planning fees in the first year alone.

Frequently Asked Questions About Tax-Efficient Investments

What makes an investment “tax-efficient”?

When clients ask me what makes an investment truly tax-efficient, I explain it’s like having a car that doesn’t leak fuel—you simply keep more of what you’ve earned.

Tax-efficient investments minimize your tax burden through several key characteristics. First, they typically have low turnover, meaning there’s minimal buying and selling of underlying securities. Think of this as fewer taxable events being triggered throughout the year.

The type of income generated matters tremendously too. Investments producing qualified dividends (taxed at lower rates) rather than ordinary income can save you thousands over time. This is why many of our clients at Elite Tax Strategy Solutions pivot toward equity ETFs rather than corporate bond funds in their taxable accounts.

“The difference between paying 37% versus 15% on your investment income is life-changing over decades,” as I often tell clients during our planning sessions.

Structural advantages also play a crucial role. ETFs use a mechanism called in-kind redemptions that helps them avoid distributing capital gains to shareholders—a distinct advantage over traditional mutual funds. Meanwhile, tax exemptions like those offered by municipal bonds can provide income completely free from federal (and sometimes state) taxes.

Finally, the best tax-efficient investments give you control over timing. When you hold individual stocks long-term, you decide when to realize gains or losses—unlike mutual funds that might distribute gains regardless of your personal situation.

How do I decide which assets go in which accounts?

Placing investments in their optimal accounts—what we call asset location—can be just as important as what you invest in. I like to think of it as putting each plant in the soil where it will thrive best.

For your tax-deferred accounts like Traditional IRAs and 401(k)s, focus on investments that would otherwise create the biggest tax headaches:

– Bonds and fixed income that generate ordinary income

– REITs with their higher dividend distributions

– Actively managed funds that tend to realize gains frequently

– Any investment you might need to sell before reaching long-term status

Your Roth accounts should house your growth superstars. Since Roth growth is never taxed, this is where your highest-potential investments belong. I recently helped a client reorganize their portfolio, moving their aggressive small-cap and emerging markets funds into their Roth IRA. “It’s like giving your race horses the best track,” I explained.

For taxable brokerage accounts, emphasize naturally tax-efficient investments like:

– Index ETFs with their minimal distributions

– Tax-managed funds specifically designed to reduce tax impact

– Municipal bonds (which would waste their tax advantage in an IRA)

– Individual stocks you plan to hold for years

– International investments that can use foreign tax credits

“Your specific financial situation might call for adjustments to these guidelines,” I always remind clients during our strategy sessions. “Your tax bracket, time horizon, cash flow needs, and overall wealth picture all influence the optimal arrangement for your investments.”

When should I harvest losses, and what are wash-sale rules?

Tax-loss harvesting is like finding silver linings in market clouds—turning temporary downturns into tax advantages. But timing matters.

The best opportunities for harvesting losses typically arise during market corrections or significant downturns. However, don’t wait for major market events. Regular portfolio reviews can reveal individual positions showing losses worth capturing.

Other prime harvesting moments include when you’re already rebalancing your portfolio, when you’ve realized capital gains elsewhere that need offsetting, or simply before year-end to reduce your current year’s tax bill.

One client called me last October after selling a rental property with substantial gains. We immediately reviewed her portfolio and identified several underwater positions, harvesting enough losses to offset a significant portion of her real estate gains.

The wash-sale rule is the critical guardrail you need to understand. This IRS rule prevents you from claiming a tax loss if you purchase a “substantially identical” security within 30 days before or after selling an investment at a loss. It’s designed to prevent purely tax-motivated transactions without actual economic impact.

To steer this rule while maintaining your investment strategy:

- Replace the sold security with something similar but not identical (like swapping a Vanguard S&P 500 fund for a Fidelity total market fund)

- Wait 31 days before repurchasing your original investment

- Remember the rule applies across all accounts—including IRAs and even your spouse’s accounts

“Market volatility doesn’t follow a calendar,” I often remind clients. “While December gets all the attention for tax planning, some of our most successful harvesting has happened during unexpected market drops in spring and summer months.”

At Elite Tax Strategy Solutions, we’ve found that proactive, year-round attention to tax-loss opportunities typically yields 1-2% better after-tax returns compared to only harvesting in December. That’s real money staying in your pocket rather than going to the IRS.

Conclusion & Next Steps

Let’s be honest – tax-efficient investing isn’t the most exciting topic at dinner parties. But as we’ve seen throughout this guide, it might be one of the most important conversations for your financial future.

Think about this: Two investors with identical portfolios and returns can end up with dramatically different wealth simply because one paid attention to tax efficiency while the other didn’t. That difference isn’t just pocket change – it could mean hundreds of thousands of extra dollars in your retirement account.

I’ve worked with clients who were brilliant at picking investments but were unknowingly losing 20-30% of their returns to unnecessary taxes. Small changes to their approach – like switching from mutual funds to ETFs in taxable accounts – made enormous differences over time.

Remember these powerful strategies we’ve covered:

The investment vehicles you choose matter tremendously. Tax-efficient investments like ETFs and index funds can dramatically reduce your annual tax burden without sacrificing returns.

Where you hold each investment can be just as important as what you own. Your bonds probably belong in your IRA, while your ETFs likely belong in your taxable account – this strategic placement can boost your after-tax returns significantly.

Tax-loss harvesting isn’t just a year-end chore but an ongoing opportunity. Markets provide windows for tax savings throughout the year if you’re paying attention.

Specialized accounts like HSAs offer incredible triple-tax advantages that are simply too good to ignore for those who qualify.

The way you give to charity can transform both your tax situation and the impact of your generosity when done thoughtfully with appreciated securities.

At Elite Tax Strategy Solutions, we see tax efficiency not as a standalone strategy but as a crucial piece of your complete financial picture. While the principles in this guide apply broadly, your optimal approach depends on your unique situation – your income, your time horizon, your specific goals, and your personal values.

Our team specializes in creating personalized tax roadmaps that don’t just look at this year’s tax return but at your lifetime tax picture. We work one-on-one with clients to develop strategies that evolve as tax laws change and as your life circumstances shift.

I often tell clients that investment returns are largely outside their control – markets will do what markets do. But how much of those returns you get to keep? That’s something we can influence through thoughtful planning.

With the right approach to tax-efficient investments, you can potentially add years of additional retirement income or significantly increase what you leave to heirs or charitable causes you care about.

Ready to stop giving Uncle Sam more than his fair share of your investment returns? Visit our Comprehensive Financial Planning page to learn how we can help you keep more of what you earn through personalized tax-efficient investment strategies.

After all, it’s not just what your investments earn that matters – it’s what you get to keep.