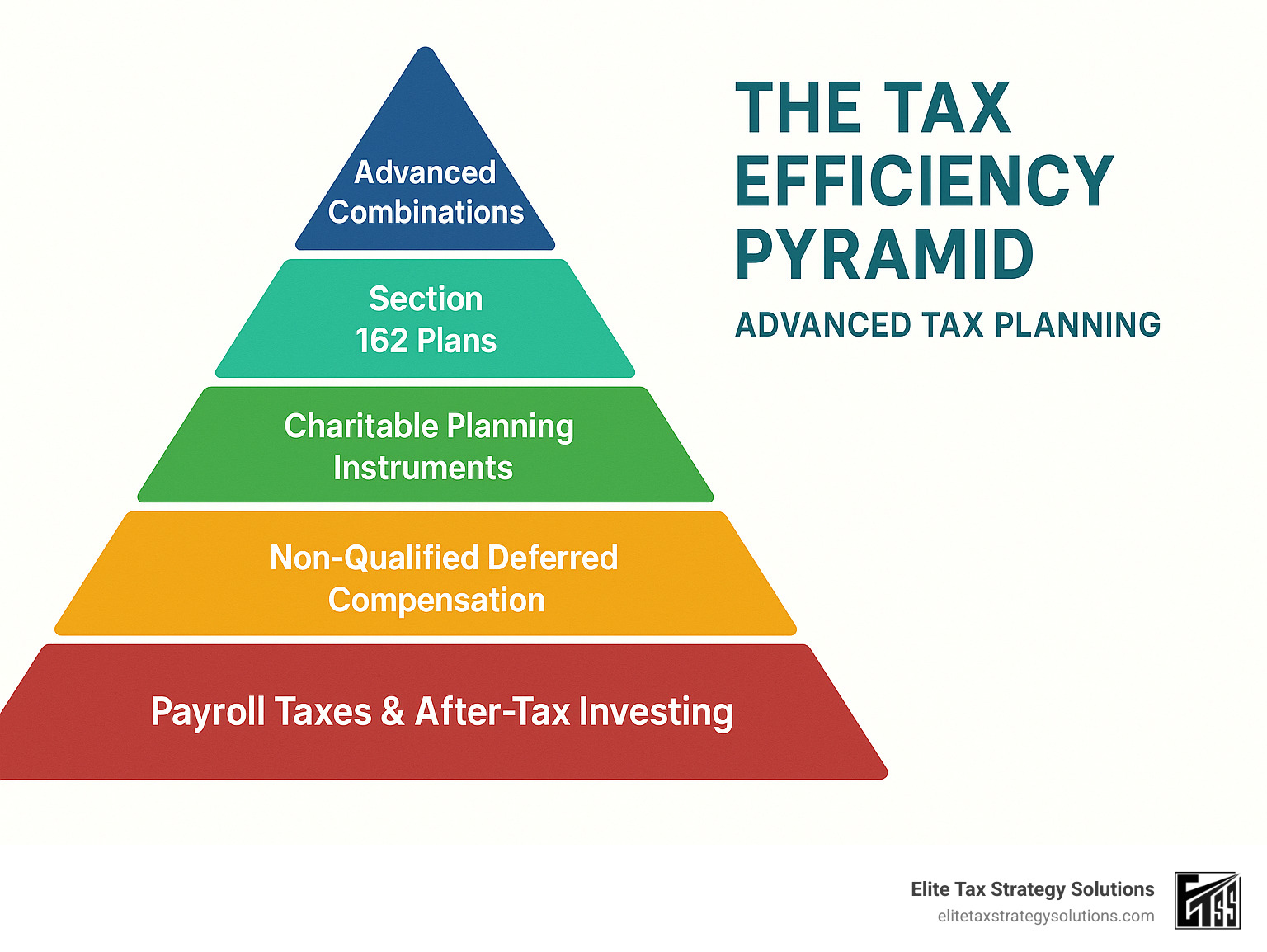

The Tax Efficiency Pyramid: Beyond Basic Planning

Advanced tax planning is a proactive, strategic approach to legally minimizing your tax burden through sophisticated techniques that go far beyond basic tax preparation. Unlike simple tax filing, advanced planning involves year-round strategy implementation to maximize after-tax wealth.

What is Advanced Tax Planning?

* A comprehensive approach focused on legally reducing tax liability

* Involves strategic timing of income, deductions, and investments

* Requires forward-looking analysis of multiple tax years

* Integrates business, investment, retirement, and estate strategies

* Aims to maximize after-tax wealth rather than just meeting compliance

For high-income earners and business owners, the difference between basic tax preparation and advanced tax planning can mean hundreds of thousands—or even millions—of dollars in tax savings over time. As one tax expert noted in our research, “$500,000 invested after tax drag grows to just $662,287 versus $5,031,328 with tax-efficient vehicles over 30 years.”

The most successful individuals view tax planning as an active wealth-building strategy rather than a once-yearly compliance chore. When marginal tax rates often exceed 50% (combining federal, state, and surtaxes), advanced planning becomes essential for preserving wealth.

Key strategies often include:

- Income timing and shifting to lower tax brackets

- Tax-efficient retirement vehicles beyond basic 401(k)s

- Strategic use of trusts for wealth transfer

- Charitable giving structures that provide tax and income benefits

- Business entity optimization to minimize self-employment taxes

I’m David Fritch, a CPA with 40 years of experience implementing advanced tax planning strategies for high-income clients and small business owners through my firm Elite Tax Strategy Solutions. My background as both a tax professional and former registered investment advisor gives me unique insights into integrating tax and wealth strategies.

Basic advanced tax planning vocab:

– financial stability planning

– tax-efficient investments

– tax planning for real estate investors

Why Go Beyond Basic Tax Prep?

Think of advanced tax planning as preventative healthcare for your finances. While tax preparation simply reports what already happened (often when it’s too late to change anything), true planning shapes your financial decisions throughout the year to legally minimize what you owe.

This distinction matters now more than ever before. High earners today face a perfect storm of tax challenges: marginal rates that can exceed 50% when you combine federal and state taxes, the additional 3.8% Net Investment Income Tax that kicks in over $200,000, and the looming sunset of the Tax Cuts and Jobs Act in 2026 that could significantly raise rates.

Plus, if you’re building wealth for future generations, the current estate tax exemption of $13.61 million is scheduled to drop dramatically to around $7 million in 2026 – potentially exposing millions more of your assets to taxation.

The True Cost of “Reactive” Filings

When you settle for reactive tax preparation instead of proactive planning, the costs are both substantial and often invisible.

Tax drag silently erodes your investment returns year after year. Without proper planning, you might be paying taxes annually on gains that could have grown tax-deferred or even tax-free in the right vehicles. Over decades, this difference can be staggering – as much as $4.3 million on a $500,000 investment over 30 years, according to our analysis.

Bracket creep happens when unmanaged income pushes you into higher tax brackets unnecessarily. Without year-round planning, you might miss opportunities to time income recognition or deductions strategically.

Many powerful tax strategies require implementation well before December 31st. By the time you’re sitting with your tax preparer in April, those opportunities have already vanished – leaving you with a larger tax bill and the frustrating knowledge that you could have paid less with proper planning.

And let’s not forget about penalty exposure – reactive approaches often lead to estimated tax penalties that could have been easily avoided.

Who Needs This Level of Attention?

While everyone benefits from some tax planning, advanced tax planning delivers its most impressive results for certain groups:

High-income earners making over $200,000 annually face progressive tax rates and additional surtaxes that make planning essential. The difference between good and great tax planning at this income level often means tens of thousands in annual tax savings.

Business owners, especially those with S corporations or pass-through entities, have unique opportunities to structure compensation, retirement plans, and business expenses in tax-advantaged ways. The right entity structure alone can save substantial self-employment taxes.

Real estate investors benefit enormously from strategic planning around depreciation, 1031 exchanges, and opportunity zone investments. Without proper guidance, these investors often pay far more in taxes than legally required.

Those with complex investments like stock options, RSUs, or private equity need specialized planning to manage vesting schedules, alternative minimum tax implications, and optimal exercise timing.

Ultra-high-net-worth families with estates exceeding $5 million face potentially massive estate tax exposure without proper succession planning strategies.

At Elite Tax Strategy Solutions, we’ve found that clients typically need to have incomes above $200,000 or net worth exceeding $5 million to realize the greatest benefits from comprehensive tax planning for high earners. If you fall into any of these categories, basic tax preparation simply isn’t enough to protect your hard-earned wealth.

Advanced Tax Planning Strategies That Slash Income, Capital Gains & Estate Taxes

Now let’s explore the strategies that can dramatically reduce your tax burden across multiple dimensions. These advanced tax planning techniques work together to create a comprehensive approach to tax minimization.

Income-Shifting & Bracket Management with Family Entities

Imagine being able to redirect some of your income to family members who are in lower tax brackets. That’s exactly what properly structured family entities allow you to do.

With Family Limited Partnerships (FLPs), you can gift limited partnership interests to family members while maintaining control as the general partner. Similarly, Family Limited Liability Companies (FLLCs) provide this benefit along with additional liability protections that many business owners appreciate.

This approach to income splitting can lead to substantial savings. For example, a business owner earning $600,000 annually might save over $30,000 each year by thoughtfully distributing income among family members through an FLLC structure.

Just be careful about the “kiddie tax” – the IRS isn’t naive! This rule taxes unearned income of children under 19 (or 24 for full-time students) at the parents’ higher rate.

Our Tax Planning for Businesses services can help you steer these family entity structures with proper documentation and implementation.

“Forever-Roth” Game Plan: Conversions & Mega-Backdoor Tactics

There’s something magical about Roth accounts – they grow tax-free and provide tax-free withdrawals. That’s why I call them “forever” accounts in my practice.

Roth conversion timing is an art form. Converting traditional IRAs to Roth IRAs during years when your income dips or when the market takes a temporary downturn can save you thousands in conversion taxes. I’ve helped business owners with fluctuating incomes strategically convert portions of their traditional IRAs during lower-income years, securing future tax-free growth while minimizing the conversion tax hit.

The Mega-backdoor Roth strategy allows you to contribute after-tax dollars to a 401(k) and then immediately roll them to a Roth. And unlike traditional retirement accounts, Roth IRAs have no required minimum distributions, allowing your money to grow tax-free for life – or even for generations if part of an estate plan.

Capital Gains Control: Installment Sales, 1031 Exchanges & QSBS

When it comes to managing capital gains, timing and structure are everything.

Installment sales allow you to spread gains over multiple tax years, potentially keeping you in lower tax brackets. For real estate investors, 1031 exchanges are like financial magic – they let you defer gains on investment properties by exchanging for like-kind property.

One of my favorite strategies for business owners is the Qualified Small Business Stock (QSBS) exclusion. Section 1202 allows up to 100% exclusion of capital gains on qualifying small business stock held for 5+ years. I’ve seen investors save hundreds of thousands in taxes through careful QSBS planning.

For those with significant capital gains, Qualified Opportunity Zones provide another avenue to defer and potentially reduce taxes by investing in designated development areas.

Harvesting Losses Year-Round

Tax-loss harvesting isn’t just a December activity. Smart investors make it a year-round practice.

Through strategic rebalancing, you can sell underperforming investments to offset gains elsewhere in your portfolio. Just be careful with the wash-sale rule – avoid repurchasing substantially identical securities within 30 days, or you’ll forfeit the tax benefit.

For sophisticated investors, direct indexing allows you to own individual securities rather than funds, creating more opportunities to harvest losses while maintaining your desired market exposure.

Here’s a pro tip I share with my clients: Prioritize harvesting short-term losses to offset short-term gains first, since these are taxed at higher ordinary income rates. Only then use remaining losses against long-term gains.

Boost Cash Flow with Retirement & Benefit Plans

The retirement plan landscape offers so much more than just basic 401(k)s for reducing your current tax burden.

Cash balance plans are particularly powerful for older business owners, allowing contributions exceeding $100,000 annually in many cases. I worked with an orthopedic surgeon who implemented a cash balance plan that enabled him to defer $250,000 annually, saving approximately $100,000 in current-year taxes while building a substantial retirement nest egg.

For self-employed individuals, SEP IRAs provide simplified but significant tax-advantaged retirement savings. And executives should explore Non-Qualified Deferred Compensation (NQDC) plans that allow income and tax deferral to future years when you might be in lower tax brackets.

Our approach to Proactive Tax Planning leverages these vehicles to not only reduce your current tax bill but build substantial tax-advantaged wealth for your future. As noted in Tax Planning for High Earners, these strategies can provide a substantial tax benefit when properly implemented.

Tools & Structures for Tax-Efficient Wealth Transfer

With the estate tax exemption scheduled to drop substantially in 2026, advanced tax planning for wealth transfer becomes increasingly important for many families. The current $13.61 million exemption will likely fall to around $7 million, putting many more families in range of potential estate taxes.

Trust Toolbox: ILITs, GRATs, SLATs & IDGTs

Think of trusts as specialized vehicles designed to transport your wealth to the next generation with minimal tax friction. Each type serves a unique purpose in your estate planning journey.

When clients visit us at Elite Tax Strategy Solutions, we often recommend Irrevocable Life Insurance Trusts (ILITs) as a starting point. These trusts work like a protective shield, keeping life insurance proceeds completely outside your taxable estate. This can be a game-changer for families concerned about estate liquidity.

Grantor Retained Annuity Trusts (GRATs) offer another powerful option. I recently worked with a business owner who transferred $5 million to a GRAT. Over the next decade, he’ll receive his principal back through annuity payments, while his children will inherit approximately $3 million in appreciation – all with minimal gift tax impact. The beauty is in the structure’s simplicity and effectiveness.

For married couples, Spousal Lifetime Access Trusts (SLATs) provide an neat balance of wealth transfer and access. You can move assets out of your estate while your spouse maintains indirect access to those funds if needed. This provides both tax efficiency and peace of mind.

Intentionally Defective Grantor Trusts (IDGTs) create a fascinating tax disconnect – the assets move outside your estate for estate tax purposes, but you remain responsible for the income taxes. This arrangement allows trust assets to grow essentially “tax-free” while further reducing your taxable estate as you pay those taxes.

Charitable Vehicles That Pay You Back—CRTs, CLATs & DAFs

Charitable planning doesn’t have to mean giving up financial security. In fact, the right structures can benefit both your favorite causes and your family’s financial wellbeing.

Charitable Remainder Trusts (CRUTs or CRATs) provide you income for life while generating an immediate partial tax deduction. The remaining assets go to your chosen charity when the trust ends. These work wonderfully for highly appreciated assets that would otherwise trigger significant capital gains taxes if sold.

Charitable Lead Annuity Trusts (CLATs) flip this arrangement – your chosen charity receives income for a set period, after which the remaining assets pass to your beneficiaries. This approach can provide substantial estate tax savings while supporting causes you care about.

For flexibility and simplicity, Donor-Advised Funds (DAFs) are hard to beat. You receive an immediate tax deduction when contributing, but can recommend grants to charities gradually over time. This strategy pairs beautifully with Tax-Efficient Investments to maximize both charitable impact and tax benefits.

For clients over 70½, Qualified Charitable Distributions (QCDs) allow direct transfers of up to $100,000 annually from IRAs to qualified charities without counting as taxable income. This strategy becomes particularly valuable when required minimum distributions would otherwise push you into higher tax brackets.

Life Insurance & Captive Insurance for Tax Leverage

Insurance strategies offer unique advantages in the advanced tax planning world that extend far beyond basic protection.

Permanent life insurance provides a powerful combination of tax-free death benefits and tax-deferred cash value growth. For larger policies, premium financing can leverage these benefits further – borrowing to pay premiums while the policy’s internal growth potentially outpaces the loan interest.

One of our more entrepreneurial clients, an online marketing professional, implemented a captive insurance strategy with impressive results. By forming his own insurance company to cover specific business risks, he gained meaningful tax deductions while creating a sophisticated risk management solution. This approach requires careful implementation but can provide substantial benefits for the right business owner.

Comparing Entity Structures for Business Owners

The structure of your business dramatically impacts your tax situation. Here in Jasper, Indiana, we help clients steer these choices based on their unique circumstances:

| Entity Type | Income Tax | Self-Employment Tax | Fringe Benefits | Section 199A | Best For |

|---|---|---|---|---|---|

| Sole Proprietor | Personal rates | All income | Limited | Yes, 20% QBI | Simplicity, startups |

| S Corporation | Personal rates | Reasonable salary only | Limited | Yes, 20% QBI | Service businesses, small-medium sized |

| LLC (default) | Personal rates | All income | Limited | Yes, 20% QBI | Flexibility, liability protection |

| C Corporation | 21% corporate + dividends | None | Extensive | No | Retained earnings, fringe benefits |

The S Corporation structure often provides the best balance for many of our clients. By paying yourself a reasonable salary and taking the rest as distributions, you can potentially save thousands in self-employment taxes annually while still qualifying for the 20% Qualified Business Income deduction.

For businesses planning to reinvest significant profits or provide extensive fringe benefits, the C Corporation’s 21% flat tax rate might be advantageous despite the potential for double taxation on dividends.

At Elite Tax Strategy Solutions, we believe that thoughtful wealth transfer planning is about more than just tax savings – it’s about creating a meaningful legacy while maintaining financial security for you and your loved ones. We’d be honored to help you craft a strategy custom to your unique situation.

Staying Proactive, Compliant & Tech-Savvy

Let’s face it – tax laws change constantly, and what worked last year might not be optimal today. That’s why advanced tax planning isn’t a “set it and forget it” activity but rather an ongoing process that requires regular attention.

When I work with clients at Elite Tax Strategy Solutions, I emphasize that staying ahead of tax changes is just as important as implementing the strategies themselves. This proactive approach helps prevent surprises and keeps your financial plan aligned with current laws.

Advanced Tax Planning Pitfalls to Avoid

Even the most sophisticated strategies can backfire if not implemented properly. I’ve seen well-intentioned clients fall into these common traps:

Listed transactions are tax strategies the IRS has specifically flagged as potentially abusive. These are guaranteed to trigger extra scrutiny, and the penalties can be severe. We carefully avoid these red-flagged approaches while still finding legitimate ways to minimize your tax burden.

Overvaluation issues often arise when transferring assets to family members or charities. I remember one client who nearly claimed a $250,000 deduction for artwork that was professionally appraised at just $75,000. That kind of discrepancy would have likely triggered an audit and potential penalties.

The step-transaction doctrine is another area where careful planning matters. The IRS may collapse what appear to be separate transactions into one if they seem pre-arranged. As I tell my clients, “It’s not just what you do, but how and when you do it that matters.”

Finally, every strategy must have economic substance beyond tax savings. The days of pure tax plays are long gone – there needs to be a legitimate business or investment purpose behind your actions.

Building Your Advisory Dream Team

No single professional has all the expertise needed for comprehensive advanced tax planning. The most successful clients build a collaborative team:

Your CPA handles tax projections and compliance, ensuring everything is reported correctly. At Elite Tax Strategy Solutions, we take pride in providing this foundation.

A good tax attorney becomes invaluable for complex structures and legal documentation. They ensure your strategies are properly implemented and documented.

A fiduciary financial advisor helps integrate tax strategies with your investment approach. The best investment returns in the world can be undermined by poor tax planning.

For families with significant wealth, an estate planning attorney creates the trusts and legal structures that protect your legacy, while a valuation professional provides defensible valuations for business interests and complex assets.

I personally work to coordinate with your existing advisors or can recommend qualified professionals to complete your team. This collaborative approach ensures all aspects of your financial life work in harmony.

How Technology Boosts Advanced Tax Planning

Remember when tax planning meant shuffling papers and manual calculations? Those days are thankfully behind us. Today’s technology makes advanced tax planning more powerful and accessible than ever.

AI-driven scenario modeling allows us to test dozens of tax strategies across multiple future years. This helps identify which approaches will likely deliver the greatest tax savings over time, not just for the current year.

Secure client portals have transformed how we collaborate. No more risky email attachments or lost documents – everything stays organized and protected in one secure location.

Real-time tax alerts keep us informed about changing laws and regulations. When Congress makes a change that affects your situation, we can quickly adapt your strategy rather than waiting until tax season.

Data analytics has become particularly powerful for identifying planning opportunities. By analyzing patterns in your financial data, we can spot trends and opportunities that might otherwise be missed.

At Elite Tax Strategy Solutions, we leverage these technological advantages while maintaining the personal touch that complex financial situations demand. Our Tax Optimization Strategies combine the best of human expertise with cutting-edge tools to deliver results that would have been impossible just a few years ago.

The most successful tax planning isn’t about aggressive schemes or questionable deductions – it’s about systematically applying legitimate strategies in a coordinated, documented way that stands up to scrutiny while minimizing your tax burden. With the right team, tools, and approach, you can steer even the most complex tax situations with confidence.

Frequently Asked Questions about Advanced Tax Planning

What is advanced tax planning, and when should I start?

Think of advanced tax planning as playing chess with your finances instead of checkers. It’s not just about filing taxes correctly—it’s about strategically positioning your financial pieces throughout the year to legally minimize what you owe.

Most people ask me when they should start this level of planning. My answer? If your household income has crossed the $200,000 threshold or your net worth is approaching $5 million, it’s time. At these levels, the potential tax savings typically more than cover the cost of sophisticated planning.

That said, the magic of compounding means starting earlier is always better. Strategies like Roth conversions or tax-efficient investment positioning can create dramatically different outcomes when given 10 or 20 years to work their magic. One client who started planning in her 40s instead of her 50s ended up with nearly twice the after-tax retirement assets.

Which strategies deliver the biggest bang for my tax buck?

This is like asking which exercise gives the best results—it depends entirely on your personal situation! However, I can tell you which strategies tend to move the needle most significantly for our clients:

Business owners typically see enormous benefits from proper S corporation structuring to minimize self-employment taxes—often saving $15,000+ annually with proper salary/distribution planning.

For high-income professionals and business owners, maximizing retirement contributions (especially through cash balance plans that allow $100,000+ annual contributions) frequently delivers six-figure tax benefits over time.

Timing Roth conversions during lower-income years or market downturns can transform decades of future growth into tax-free income. I’ve seen clients save hundreds of thousands in future taxes through well-executed conversion strategies.

Strategic charitable giving using appreciated assets rather than cash—especially through vehicles like Donor-Advised Funds or Charitable Remainder Trusts—often delivers double tax benefits while supporting causes you care about.

Family income shifting through properly structured family entities can spread income across multiple tax brackets, though this requires careful navigation of kiddie tax and other anti-abuse rules.

How do I choose the right advisor for advanced strategies?

Finding the right tax planning partner is crucial—and it’s not always the advisor with the fanciest office or biggest marketing budget. Look for someone who:

Has worked with clients in similar financial situations to yours. If you’re a real estate investor, you want someone who understands cost segregation and 1031 exchanges, not just general tax rules.

Demonstrates knowledge of multiple strategies rather than pushing a one-size-fits-all approach. Be wary of anyone selling a single “magic” tax solution.

Takes a year-round approach instead of just offering year-end tips. Real advanced tax planning happens in April through November, not just December.

Collaborates willingly with your other advisors. Tax strategies often intersect with legal, investment, and insurance considerations, requiring a team approach.

Explains complex concepts clearly without promising unrealistic results. If someone guarantees to eliminate your tax bill entirely, that’s a red flag!

At Elite Tax Strategy Solutions, we’ve built our practice around education-focused relationships. We believe informed clients make better decisions, and we’d rather you understand exactly why we’re recommending a strategy than simply trust us blindly.

The best tax planning isn’t about finding loopholes—it’s about aligning your financial decisions with tax-efficient strategies that support your broader life goals. When done right, advanced tax planning becomes an integral part of your wealth-building journey, not just a once-a-year headache.

Conclusion

Let’s be honest—advanced tax planning isn’t just for people with private jets and vacation homes in the Hamptons. It’s for anyone who works hard and wants to keep more of what they earn. The strategies we’ve explored throughout this guide can transform your financial future when implemented thoughtfully and consistently.

Here at Elite Tax Strategy Solutions, we see it happen every day. A business owner in Jasper finds they’ve been overpaying self-employment taxes for years. A physician realizes her retirement plan could be boostd with a cash balance plan. A real estate investor learns how to defer capital gains indefinitely through strategic 1031 exchanges.

These aren’t theoretical scenarios—they’re real stories from our clients who’ve finded the power of proactive planning.

The tax landscape is shifting beneath our feet. With major TCJA provisions set to expire in 2026, the window for implementing many of these strategies is narrowing. Tax rates for many are likely to increase, and estate tax exemptions will probably drop significantly. The time to act is now, not when these changes are already upon us.

It’s not your gross income that builds wealth—it’s what remains after taxes. With thoughtful planning, you can legally and ethically reduce your tax burden while building lasting financial security for yourself and future generations. Advanced tax planning isn’t about aggressive schemes or offshore accounts—it’s about understanding the tax code as it was designed and using it to your advantage.

I’ve spent four decades helping clients steer these waters, and I can tell you with certainty: the difference between reactive tax preparation and proactive planning is often hundreds of thousands of dollars over a lifetime.

Ready to stop overpaying and start building real wealth? Let’s talk. At Elite Tax Strategy Solutions, we specialize in creating personalized tax strategies that align with your broader financial goals and values. Our holistic approach integrates tax minimization with wealth building to create genuine financial freedom.

Your tax situation is unique. Your planning should be too.