The Strategic Approach to Tax Reduction

Minimize tax strategies for high income earners can save you thousands of dollars each year. As your income increases, so does your tax burden—but there are legal, effective ways to reduce what you owe to the IRS.

Here are the most effective strategies to minimize taxes for high-income individuals:

- Maximize retirement account contributions (401(k), IRA, HSA)

- Time your income and deductions strategically

- Use tax-loss harvesting to offset investment gains

- Invest in tax-advantaged vehicles like municipal bonds

- Make strategic charitable contributions

- Consider business ownership tax advantages

- Implement estate planning strategies

- Explore tax-friendly state residency options

The IRS defines high-income earners as those reporting $200,000 or more in total positive income, though in expensive markets this threshold may reach $400,000. Without proper planning, these earners can lose a significant portion of their income to taxes.

As the saying goes, “It’s not what you make but what you keep that counts.” This principle is especially true for high-income individuals facing tax bracket creep—where rising income pushes you into higher tax brackets, potentially increasing your effective tax rate.

I’m David Fritch, with over 40 years of experience helping high-income earners minimize tax strategies for high income through my work as both a CPA and attorney specializing in innovative tax planning solutions for individuals earning between $200,000 and $2,000,000 annually.

Simple guide to minimize tax strategies for high income terms:

– advanced tax planning strategies

– wealth management tax planning

– tax diversification strategy high income

1. Maximize Contributions to Retirement Accounts

Want to keep more of your hard-earned money? Retirement accounts are your best friends when it comes to minimize tax strategies for high income earners. These powerful tools not only secure your future but provide immediate tax relief today.

For 2024, contribution limits have increased across the board, giving you even more opportunity to shield income from the taxing hands of the IRS:

| Retirement Account | 2024 Contribution Limit | Catch-Up Contribution (Age 50+) | Total Possible Contribution (50+) |

|---|---|---|---|

| 401(k)/403(b) | $23,500 | $7,500 | $31,000 |

| Traditional/Roth IRA | $7,000 | $1,000 | $8,000 |

| SEP IRA | Up to $69,000 or 25% of compensation | N/A | Same |

| Solo 401(k) | Up to $66,000 | $7,500 | $73,500 |

At Elite Tax Strategy Solutions, we often remind our clients: “It’s not what you make but what you keep that counts.” By maximizing your retirement contributions, you’re essentially converting today’s taxable income into tomorrow’s tax-advantaged wealth.

Take Advantage of Employer-Sponsored Plans

Your workplace retirement plan might be the most convenient tax shelter available to you. When you contribute to a 401(k) or 403(b), you immediately reduce your taxable income by that same amount.

Let’s put some real numbers to this: If you’re earning $400,000 annually and contribute the maximum $23,500 to your 401(k), your taxable income drops to $376,500. In the 37% federal tax bracket, that’s an immediate tax savings of $8,695 this year alone!

Don’t overlook your employer match – it’s literally free money. If your company matches 5% of your $400,000 salary, that’s an additional $20,000 growing tax-deferred in your account. Missing out on this match is like declining a $20,000 bonus.

For those running their own businesses or working independently, options like SEP IRAs and Solo 401(k)s are even more generous, potentially allowing contributions up to $69,000 for 2024. These higher limits can dramatically reduce your taxable income while building substantial retirement savings.

Consider Backdoor Roth IRA Conversions

Making too much money to contribute to a Roth IRA? There’s a perfectly legal workaround. For 2024, direct Roth IRA contributions start phasing out at $161,000 for singles and $240,000 for married couples filing jointly.

The “backdoor Roth IRA” strategy neatly solves this problem:

- Make a contribution to a non-deductible traditional IRA (which has no income restrictions)

- Shortly afterward, convert those funds to a Roth IRA

- Pay taxes only on any earnings that accumulated between your contribution and conversion

If you’re fortunate enough to have a 401(k) plan that allows after-tax contributions, you might also qualify for the “mega backdoor Roth” strategy. This approach can potentially allow for significantly larger conversions – sometimes up to $40,000 or more annually.

“Using a Roth conversion can be beneficial, especially since Roth accounts do not require RMDs, offering long-term tax advantages,” notes tax expert Gio. This dual benefit of tax-free growth and flexibility in retirement makes Roth conversions particularly valuable for high-income professionals planning for the future.

The beauty of retirement accounts isn’t just in the immediate tax savings – it’s in the compounding growth that occurs free from annual taxation. For high-income earners facing substantial tax bills, maximizing these contributions should be the foundation of your tax minimization strategy.

2. Minimize Taxes with Health Savings Accounts (HSAs)

If you’re looking for a tax strategy that feels almost too good to be true, Health Savings Accounts (HSAs) might be your new best friend. These remarkable accounts offer what tax professionals lovingly call the “triple tax advantage” – a rare gem in the tax planning world that can significantly help minimize tax strategies for high income earners.

What makes HSAs so special? Unlike most tax-advantaged accounts that give you benefits either when you put money in OR when you take it out, HSAs reward you at every step of the journey:

First, every dollar you contribute reduces your taxable income. Then, your money grows completely tax-free inside the account. Finally – and this is the truly magical part – when you withdraw funds for qualified medical expenses, you pay absolutely zero taxes.

For 2025, you can contribute even more to your HSA than before:

– $4,300 for individual coverage (a $150 increase from 2024)

– $8,550 for family coverage (a $250 increase from 2024)

– An extra $1,000 catch-up contribution if you’re 55 or older

What many folks don’t realize about HSAs is that, unlike their cousin the Flexible Spending Account (FSA), your HSA money never expires. It rolls over year after year, patiently waiting for when you need it – whether that’s tomorrow or decades from now in retirement.

“HSAs are the most tax-advantaged account available in the tax code,” explains Sherman Standberry, CPA. “They’re the only account offering tax-free contributions, growth, and withdrawals when used correctly.”

Here’s where HSAs become truly powerful for high-income earners: instead of using your HSA funds for current medical expenses, consider paying those costs out-of-pocket while investing your HSA funds for long-term growth. Keep your medical receipts safely stored away, and years later – perhaps even in retirement – you can reimburse yourself tax-free for those expenses.

This approach essentially transforms your HSA into a stealth retirement account with better tax benefits than either traditional or Roth accounts. It’s especially valuable for high-income earners who may have limited access to other tax-advantaged accounts due to income restrictions.

To qualify for an HSA, you must be enrolled in a high-deductible health plan (HDHP). While these plans aren’t right for everyone, many high-income earners find the tax benefits of the HSA outweigh the potential downsides of a higher deductible, especially if you’re generally healthy and have adequate emergency savings.

At Elite Tax Strategy Solutions, we often recommend HSAs as a cornerstone of comprehensive tax planning for our high-income clients. The immediate tax deduction combined with tax-free growth makes HSAs one of the most powerful tools in your tax minimization toolkit.

3. Defer Income and Accelerate Deductions

Timing is everything—especially when it comes to your taxes. As a high-income earner, one of the most powerful yet underused ways to reduce your tax burden is strategically controlling when your income appears on your tax return and when you take your deductions.

Think of it as a financial dance: you want to push income into future years whenever possible, while pulling deductions into the current year when they’ll do the most good. This approach can significantly reduce your tax bill without changing your actual earnings or spending.

Strategies to Minimize Taxes Through Income Deferral

When you’re already in a high tax bracket, deferring income to future years can provide substantial savings. This strategy works especially well if you anticipate being in a lower tax bracket in the coming year—perhaps due to a planned sabbatical, reduced work schedule, or anticipated business expenses.

“Deferring part of your income can be a powerful strategy to minimize tax liability,” explains tax expert Gio. “If you’re normally in the 35% tax bracket but experience a year with lower self-employment income that drops you into the 32% bracket, you can strategically realize additional income to maximize the benefit of the lower rate.”

For W-2 employees, consider talking to your employer about delaying your year-end bonus until January. That $20,000 December bonus might feel nice in your bank account right away, but receiving it in January could save you thousands in taxes if it pushes you into a lower bracket for the current year.

Business owners have even more flexibility. You might hold off on sending December invoices until the last days of the month, ensuring payment arrives in January instead. Or if you’re planning major equipment purchases, timing them for December rather than January gives you the deduction a full year earlier.

For executives, non-qualified deferred compensation plans offer a formalized way to postpone receiving income until retirement years when your tax rate may be lower. Just be aware these plans come with specific rules and potential risks if your employer faces financial difficulties.

On the deduction side, the strategy flips—you want to accelerate deductions into the current tax year whenever possible:

Bunching charitable donations can be particularly effective. If you typically donate $15,000 annually to charity, consider doubling up with $30,000 this year and skipping next year. This approach helps you clear the standard deduction threshold and maximize the tax benefit of your generosity.

Prepaying deductible expenses that would normally hit in January can also help. Pay your January mortgage payment in December to claim the interest deduction this year. If you haven’t hit the $10,000 SALT (State and Local Tax) cap, consider paying property taxes early.

Medical expenses can be timed as well. If you’re planning elective procedures, clustering them in a single tax year might help you exceed the 7.5% AGI threshold needed for these deductions.

Let me share a real-world example: One of our clients, a consultant expecting to earn $750,000 last year, worked with us to defer a $100,000 project payment to January. This strategic timing kept her income below the highest tax bracket threshold. Meanwhile, she made a $50,000 charitable contribution in December rather than waiting until the following year, effectively “bunching” deductions when they provided maximum benefit.

The key to successful income and deduction timing is careful planning. At Elite Tax Strategy Solutions, we help our clients forecast their income and deductions throughout the year, identifying opportunities to minimize tax strategies for high income earners through strategic timing. This approach requires looking at your tax situation holistically—not just at year-end when options become limited.

The goal isn’t to avoid paying taxes entirely, but rather to pay them at the most advantageous time. With thoughtful planning, you can significantly reduce your overall tax burden while maintaining complete compliance with tax laws.

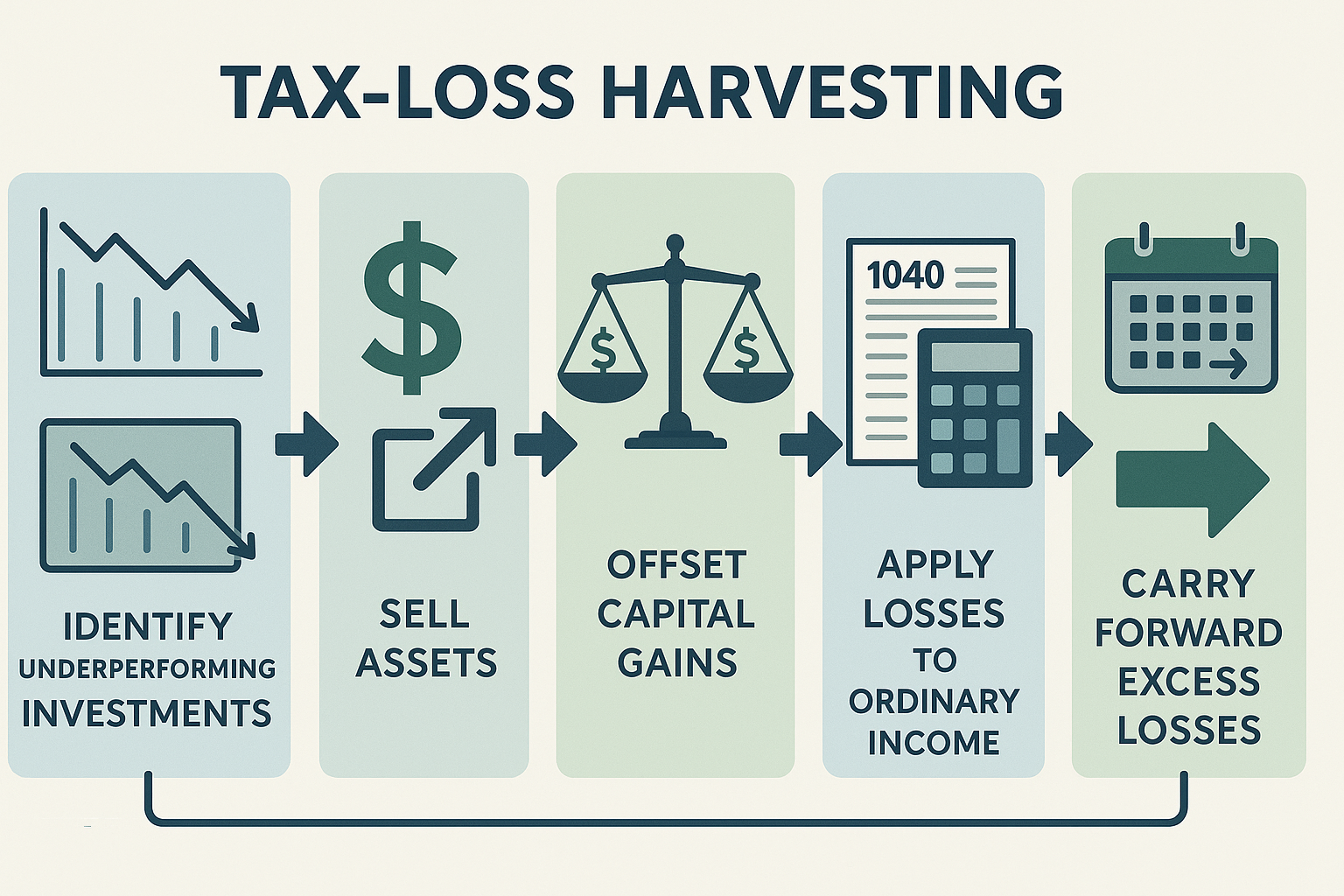

4. Leverage Tax-Loss Harvesting

Let’s talk about one of my favorite tax strategies that often flies under the radar: tax-loss harvesting. This powerful technique can help minimize tax strategies for high income earners by turning market downturns into tax advantages.

Tax-loss harvesting is like finding silver linings in investment clouds. When investments lose value (and let’s face it, even the best portfolios have some underperformers), you can sell those investments to capture the loss on paper. The IRS allows you to deduct up to $3,000 in losses against your ordinary income after offsetting any capital gains. Even better, any losses beyond that $3,000 limit roll forward to future tax years.

Here’s what makes tax-loss harvesting so valuable: those realized losses first offset your capital gains dollar-for-dollar. This is especially powerful when you can use losses to offset short-term gains (those held less than a year), which are taxed at your higher ordinary income rates.

Think of it this way: you’re essentially getting a discount on your taxes courtesy of your underperforming investments. It’s like telling the IRS, “I’ve already paid my dues through investment losses, so I’d like a break on my taxes, please.”

The beauty of this strategy is that you don’t have to abandon your investment strategy. After selling an investment at a loss, you can immediately reinvest the proceeds in a similar (but not identical) investment to maintain your market position. This keeps your money working for you while still capturing the tax benefit.

Just be careful about the wash-sale rule – the IRS’s way of saying “nice try, but no.” If you purchase a “substantially identical” security within 30 days before or after selling at a loss, the IRS will disallow the loss for tax purposes. This is where having a knowledgeable advisor can really help steer the nuances.

“One of the most common tax planning mistakes I see is neglecting tax-loss harvesting opportunities,” notes financial advisor Sherman Standberry. “Even in bull markets, there are usually some underperforming assets in a diversified portfolio.”

Let me share a real-world example: Imagine you’ve sold some tech stocks for an $80,000 long-term capital gain. Looking through your portfolio, you notice you have several investments with unrealized losses totaling $80,000. By selling those underperforming investments, you completely eliminate your tax bill on those capital gains – potentially saving $12,000 to $16,000 in taxes (assuming the 15-20% long-term capital gains rate).

For high-income earners facing the additional 3.8% Net Investment Income Tax (which kicks in at $200,000 for singles and $250,000 for married couples filing jointly), tax-loss harvesting becomes even more valuable. Every dollar of investment gains you can offset means savings on both capital gains taxes and this additional tax.

The best part? You don’t have to wait until year-end to harvest losses. At Elite Tax Strategy Solutions, we recommend monitoring your portfolio throughout the year for tax-loss harvesting opportunities, especially during market downturns when they can be most abundant.

5. Invest in Municipal Bonds

Looking for a tax-smart investment that high-income earners often overlook? Municipal bonds might be your answer. These “munis” are debt securities issued by state and local governments to fund everything from schools to highways, and they come with a tax advantage that makes financial advisors smile.

Here’s the beautiful part: interest income from municipal bonds is generally exempt from federal income tax. And it gets better – if you purchase bonds issued by your state of residence, that interest may also dodge state and local taxes, creating what we like to call a “triple tax-free” investment. Pretty sweet, right?

Let’s put this in perspective. If you’re in the 37% federal tax bracket, a municipal bond with a seemingly modest 4% yield actually provides a taxable-equivalent yield of about 6.35%. This means you’d need to find a taxable investment yielding 6.35% just to match what your muni bond is delivering after taxes.

Municipal bonds shine brightest for:

– Those of you in the highest tax brackets (hello, 37% club members!)

– Residents of high-tax states like California, New York, or New Jersey

– Investors trying to sidestep that pesky 3.8% Net Investment Income Tax

– Anyone looking to trim their taxable income without sacrificing returns

“Municipal bonds offer one of the few remaining truly tax-free investment options,” explains Sherman Standberry, CPA. “For high-income earners, the tax savings can significantly improve overall returns compared to taxable alternatives.”

You might notice that municipal bonds typically offer lower pre-tax yields than corporate bonds. Don’t let that fool you – their after-tax advantage often makes them the smarter choice for those looking to minimize tax strategies for high income. They also generally carry lower default risk than corporate bonds with similar ratings, helping you sleep better at night.

Want to dip your toe in without diving all the way? Consider municipal bond funds or ETFs. These provide instant diversification across many issuers and maturities, reducing your risk while still maintaining those wonderful tax advantages. It’s like getting the best of both worlds – tax efficiency with reduced single-issuer risk.

The formula insiders use for calculating the real value of these investments is simple:

Tax-Equivalent Yield = Municipal Bond Yield ÷ (1 - Your Marginal Tax Rate)

At Elite Tax Strategy Solutions, we’ve seen clients dramatically reduce their tax burden by strategically incorporating municipal bonds into their investment mix. It’s not flashy or exciting, but sometimes the best tax strategies are the quiet ones that steadily build wealth while keeping the IRS at arm’s length.

6. Optimize Charitable Contributions

Charitable giving isn’t just good for the soul—it can be remarkably good for your tax situation too. When done strategically, philanthropy becomes a powerful tool to minimize tax strategies for high income earners while supporting causes that matter to you.

The IRS is quite generous when it comes to charitable deductions, allowing charitable cash contributions of up to 60% of your adjusted gross income. If you’re donating non-cash assets, that limit is 30% of your AGI. Don’t worry if you’re feeling extra generous one year—any excess contributions can be carried forward for up to five years.

How High-Income Earners Can Minimize Taxes with Charitable Contributions

One of my favorite strategies for clients is setting up a Donor-Advised Fund (DAF). Think of it as your personal charitable savings account. You can make a substantial contribution in a high-income year, claim the full tax deduction immediately, and then take your time distributing those funds to charities over several years.

This “bunching” approach works wonders, especially when you’re trying to overcome the standard deduction threshold. For instance, if you typically donate $15,000 annually, you might instead contribute $45,000 to a DAF this year. You’ll get the larger itemized deduction now while supporting your favorite charities consistently over the next three years.

Did you know that donating appreciated securities instead of cash creates a remarkable double tax benefit? When you donate stocks or funds you’ve held for more than a year, you completely avoid paying capital gains tax on the appreciation, plus you get to deduct the full fair market value of the securities.

“When you donate appreciated stock that you’ve held for more than a year, you get to deduct the full value of the stock and you avoid paying capital gains taxes on the appreciation,” explains tax expert Sherman Standberry. “It’s one of the most tax-efficient ways to give.”

For those over 70½, Qualified Charitable Distributions (QCDs) offer another fantastic opportunity. You can direct up to $108,000 per year directly from your IRA to qualified charities. These distributions satisfy your Required Minimum Distribution (RMD) requirements but—here’s the beautiful part—they’re not included in your taxable income. It’s a win-win that reduces your tax burden while supporting causes you care about.

If you’re looking for more sophisticated options, consider a Charitable Remainder Trust (CRT). These specialized trusts provide income to you or your beneficiaries for a specified period, with the remainder eventually going to charity. They offer several advantages: an immediate partial tax deduction, avoidance of capital gains tax on appreciated assets, an income stream for you or your loved ones, and ultimately, a meaningful charitable impact.

Let me share a real-world example to bring this to life: One of our clients, a physician earning $800,000 annually, had $200,000 in appreciated stock with a cost basis of just $50,000. By donating the stock directly to charity instead of selling it and donating cash, she avoided $30,000 in capital gains tax (20% on the $150,000 gain), received a $200,000 charitable deduction, and provided her chosen charity with the full $200,000 value.

The best charitable strategies align your financial goals with your values. At Elite Tax Strategy Solutions, we find that helping clients support causes they care about while optimizing their tax situation creates a deeply satisfying planning experience—good for the world and good for your bottom line.

7. Use Estate Planning Strategies

Estate planning isn’t just a concern for the ultra-wealthy—it’s a powerful tool that high-income earners can use today to reduce their current tax burden while preserving more wealth for future generations. Think of it as planting financial trees whose shade you—and your loved ones—will enjoy for years to come.

In 2024, the annual gift tax exclusion has increased, giving you even more flexibility. The annual gift tax exclusion amount for 2024 to individuals is $18,000, up from $17,000 last year. For married couples, this means you can give $36,000 per recipient annually without triggering any gift tax consequences.

The lifetime gift and estate tax exemption has also grown to an impressive $13.61 million per individual (or $27.22 million for married couples) in 2024. But here’s the catch—this generous exemption is scheduled to be significantly reduced in 2026 when provisions of the Tax Cuts and Jobs Act expire. This makes strategic gifting in the next couple of years particularly valuable.

“The coming reduction in lifetime exemption amounts makes this a critical time for high-income earners to review their estate plans,” notes our senior tax strategist. “Many of our clients are accelerating their gifting strategies while the exemptions remain historically high.”

When it comes to minimize tax strategies for high income earners, several estate planning approaches stand out for their current tax benefits:

Annual gifting programs allow you to systematically transfer wealth to family members using the annual exclusion, reducing your taxable estate over time while helping loved ones. Grantor Retained Annuity Trusts (GRATs) let you transfer appreciation on assets to beneficiaries with minimal gift tax impact—particularly effective for rapidly appreciating assets or business interests.

For those with substantial life insurance, Irrevocable Life Insurance Trusts (ILITs) remove those proceeds from your taxable estate while still providing for your beneficiaries. And Family Limited Partnerships offer a way to transfer business interests while maintaining control and potentially applying valuation discounts that can significantly reduce gift and estate taxes.

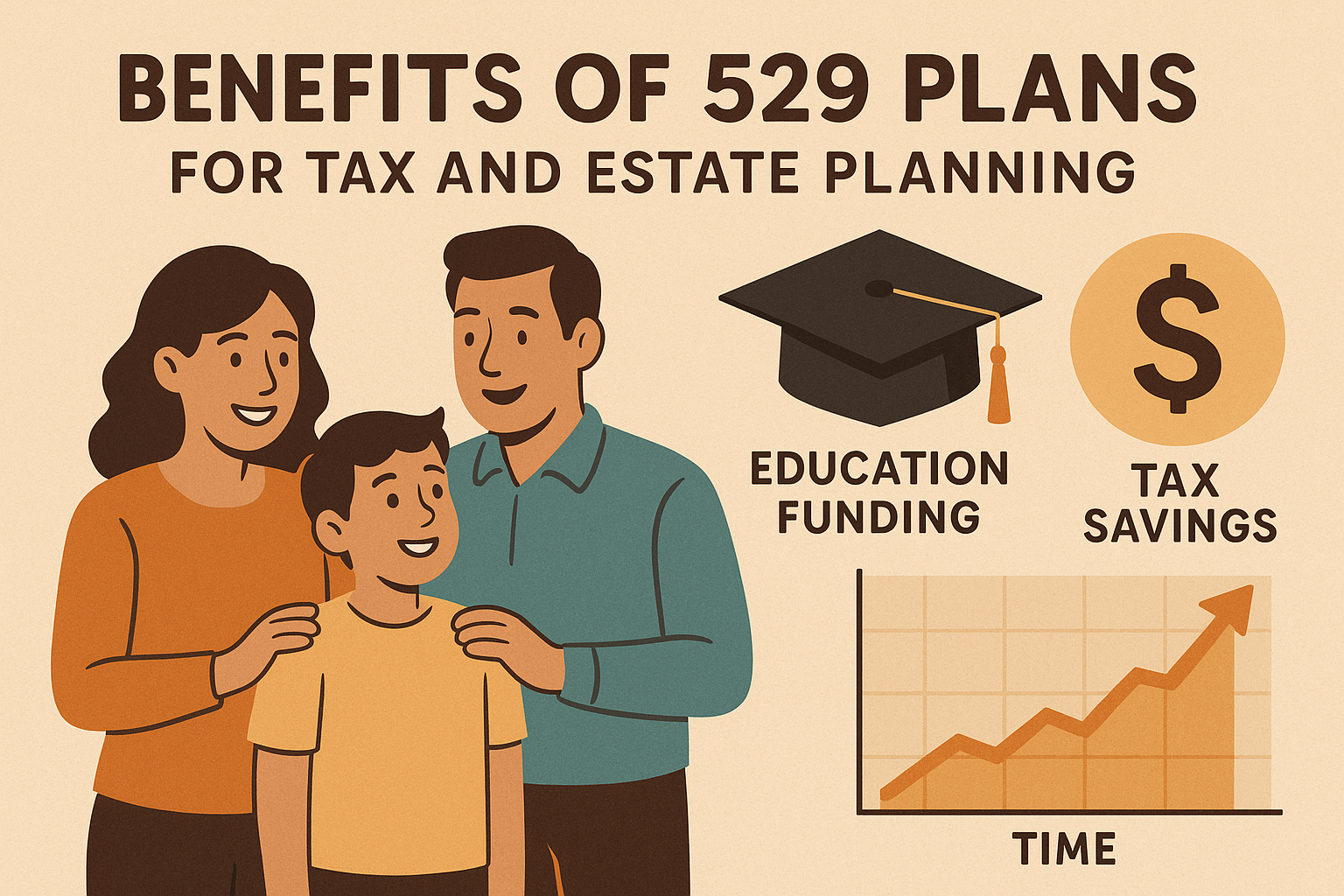

Leverage 529 Plans for Tax-Efficient Gifting

529 college savings plans deserve special attention in your estate planning toolkit. These versatile vehicles offer unique benefits that make them favorites among our high-income clients:

First, depending on your state, contributions may qualify for immediate state income tax deductions—a rare instance of getting both current tax benefits and future estate tax advantages. Second, all earnings grow completely tax-free when used for qualified education expenses. And perhaps most powerfully, 529 plans offer a “superfunding” provision that allows you to frontload five years of annual exclusion gifts in a single year.

With this frontloading strategy, an individual could contribute up to $90,000 per beneficiary in 2024 ($180,000 for married couples) without triggering gift tax, provided no additional gifts are made to that beneficiary for the next four years. This allows for significant wealth transfer and immediate tax-advantaged growth.

“529 plans serve dual purposes—funding education expenses while simultaneously reducing your taxable estate,” explains Sherman Standberry, CPA. “For grandparents especially, this can be an effective way to help future generations while managing potential estate tax exposure.”

Recent legislation has made 529 plans even more flexible. Now, up to $35,000 (lifetime limit) of unused 529 funds can be rolled over to a Roth IRA for the beneficiary, providing additional options if education needs change or if your grandchild receives scholarships.

At Elite Tax Strategy Solutions, we find that integrating estate planning with your current tax strategy creates a more comprehensive approach to wealth preservation. The strategies that reduce your estate tax exposure often provide immediate income tax benefits as well—truly a case where thoughtful planning delivers benefits both now and later.

8. Engage in Business Ownership or Side Ventures

There’s a saying in tax planning circles that the tax code is written for business owners, not employees. And there’s a lot of truth to that! Starting your own business—whether full-time or as a side venture—opens up a world of tax-saving possibilities that can dramatically help minimize tax strategies for high income earners.

As a W-2 employee, you’re essentially paying taxes on your gross income with very limited deductions available. But business owners? They get to deduct “ordinary and necessary” business expenses before calculating their taxable income, thanks to Section 162 of the Internal Revenue Code.

“Did you know that as a W-2 employee, you pay the highest taxes?” notes tax expert Sherman Standberry. “Businesses are taxed on net income after expenses, while employees are taxed on gross income with limited deductions.”

The home office deduction alone can be substantial if you use part of your home regularly and exclusively for business. Imagine writing off a portion of your mortgage interest, property taxes, utilities, internet, and even depreciation—all perfectly legal with proper documentation.

Business travel becomes partially deductible, as do business meals (50% in most cases). That conference in San Diego during February? If it’s legitimately for your business, the airfare, hotel, and half your meals could become tax deductions.

For professionals with specialized expertise, side businesses make perfect sense. A marketing executive might start a consulting practice. An attorney might teach continuing education courses or write legal guides. A doctor might develop a medical app or offer telemedicine services. Each of these creates a legitimate business structure for deducting related expenses.

Vehicle expenses offer another significant opportunity. You can either deduct actual expenses (gas, insurance, maintenance, depreciation) for the business portion of your driving or take the standard mileage rate (67 cents per mile for 2024). For someone driving 10,000 business miles annually, that’s a $6,700 deduction!

The structure of your business matters tremendously for tax planning:

Sole proprietorships offer simplicity but no liability protection. They’re reported on Schedule C of your personal return, and all profits are subject to self-employment tax.

LLCs provide liability protection with flexible tax treatment. They can be taxed as sole proprietorships, partnerships, S corporations, or even C corporations depending on your elections.

S corporations can help reduce self-employment taxes through a strategy of paying yourself a reasonable salary plus distributions. The salary is subject to payroll taxes, but the distributions aren’t—potentially saving thousands in self-employment taxes.

C corporations saw their tax rates reduced to a flat 21% under the Tax Cuts and Jobs Act, making them worth considering for very high-income individuals in certain situations.

One of the most powerful tax benefits for business owners came with the Tax Cuts and Jobs Act: the Qualified Business Income (QBI) deduction under Section 199A. This allows eligible pass-through business owners to deduct up to 20% of their qualified business income—a substantial tax break that can significantly reduce your effective tax rate.

The key to making these strategies work is legitimacy. Your business must have a genuine profit motive and appropriate documentation. The IRS looks closely at businesses that consistently show losses, particularly if they offset substantial income from other sources.

At Elite Tax Strategy Solutions, we help clients identify legitimate business opportunities that align with their expertise and interests. We then design optimal business structures and accounting systems to maximize allowable deductions while ensuring full compliance with tax regulations. The savings can be substantial—often tens of thousands of dollars annually for high-income professionals.

9. Relocate to a Tax-Friendly State

Where you live can have a dramatic impact on your tax bill—especially if you’re a high earner. When I work with clients looking to minimize tax strategies for high income, state residency often presents one of the biggest opportunities for savings.

Think about it: while federal tax rates are the same nationwide, state income taxes can vary from 0% to over 13% in California. For someone earning $500,000 annually, that difference could mean paying $65,000 more in taxes just because of your zip code!

Nine states currently don’t tax earned income at all:

– Alaska

– Florida

– Nevada

– New Hampshire (only taxes interest and dividend income)

– South Dakota

– Tennessee

– Texas

– Washington

– Wyoming

Many of my clients ask, “Can I just say I live in Florida and keep my home in New York?” Unfortunately, it’s not that simple. Tax residency requires legitimate life changes, not just paperwork.

“How do you leave a high tax state for a lower or no tax state?” asks tax expert Gio. “It’s important to officially change domicile by updating addresses, voter registrations, and memberships while avoiding frequent returns to the previous high-tax state.”

When planning a residency change, you need to understand two critical concepts:

First, your domicile is your permanent legal home—the place you intend to return to after any absences. This is more about your intention and mindset than just physical presence.

Second, statutory residency is typically based on physical presence—usually 183+ days spent in a state during the tax year. Many high-tax states use both concepts to determine who owes them taxes.

If you’re serious about changing your tax residency, be prepared to take comprehensive action. Buy or lease a home in your new state. Get that state’s driver’s license. Register your vehicles there. Update your voter registration, bank accounts, and mailing addresses. Establish relationships with local professionals like doctors and attorneys. And most importantly, actually spend most of your time in your new home state.

Keep detailed records of your whereabouts—credit card statements, travel receipts, and even cell phone location data can all help document your presence. High-tax states like New York and California are notorious for aggressively auditing residency changes, especially for high-income taxpayers who suddenly “move” to Florida or Nevada.

Don’t forget to file a final part-year resident tax return in your former state. This officially signals your departure from their tax system.

At Elite Tax Strategy Solutions, we’ve guided many clients through successful state residency changes. We help them steer the complexities while minimizing audit risk. For business owners, we also consider state business tax implications, which can vary dramatically between locations.

Even if relocation isn’t practical for you right now, understanding how your current state taxes different types of income can still inform smarter investment and retirement planning decisions. For instance, some states don’t tax retirement income or Social Security benefits, which might affect when and how you take distributions.

Changing your residency is a significant life decision that goes beyond just tax considerations. Family connections, career opportunities, climate preferences, and lifestyle factors should all weigh into your choice. But for those with flexibility, the tax savings from a strategic move can be substantial enough to fund a very comfortable retirement.

10. Shift Investment Income Timing and Character

Did you know that not all investment income is taxed the same way? For high-income earners, understanding the difference between various types of investment income can lead to thousands in tax savings each year. It’s not just about what investments you choose, but when and how you receive income from them.

Long-term capital gains—those from assets you’ve held for more than a year—enjoy significantly lower tax rates than short-term gains:

- 0% for incomes up to $47,025 (single) or $94,050 (married filing jointly)

- 15% for incomes up to $518,900 (single) or $583,750 (married filing jointly)

- 20% for incomes above these thresholds

Compare that to short-term gains, which get taxed as ordinary income at rates up to 37% for top earners. That’s nearly double! This difference creates a powerful incentive to be patient with your investments whenever possible.

Minimize Tax Strategies for High Income Through Investment Income Planning

Holding investments longer isn’t the only strategy available. Think of your investment income like clay that can be molded into different shapes—each with different tax consequences.

Timing your capital gains can make a substantial difference. If you’re considering selling appreciated assets, look at your overall income picture for the year. Will you be in a lower tax bracket than usual? That might be the perfect time to realize some gains. For instance, if you’re between jobs or taking a sabbatical, you might temporarily drop from the 20% capital gains bracket to the 15% bracket.

Installment sales offer another powerful option for larger assets. Rather than taking a lump sum payment and a big tax hit in one year, you can spread the gain—and the tax liability—across multiple tax years. This approach can keep more of your income in lower tax brackets each year.

“Changing the character of your income can significantly minimize your tax burden,” explains Sherman Standberry, CPA. “Converting ordinary income into long-term capital gains or qualified dividends can reduce your tax rate by nearly half in some cases.”

Qualified dividend investing deserves special attention in your portfolio strategy. These dividends receive the same preferential tax treatment as long-term capital gains. By focusing on companies with strong dividend histories that meet the IRS “qualified” criteria, you’re essentially converting what would otherwise be ordinary income into lower-taxed investment income.

The placement of different investments across your accounts matters too. Consider holding your tax-inefficient investments (like high-yield bonds that generate ordinary income) in tax-advantaged accounts like IRAs or 401(k)s. Meanwhile, keep investments that generate qualified dividends or long-term capital gains in your taxable accounts to take advantage of their already favorable tax treatment.

For business owners, investment income strategies take on additional dimensions. You might benefit from converting salary income to qualified business income (eligible for the Section 199A deduction) or S corporation distributions (not subject to self-employment tax).

Don’t forget about the 3.8% Net Investment Income Tax (NIIT) that applies to investment income when your modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly). Strategies that reduce your MAGI might help you avoid this additional tax entirely.

At Elite Tax Strategy Solutions, we look at both pre-tax returns and after-tax results when developing investment strategies for our clients. We understand that minimize tax strategies for high income earners requires seeing the complete picture—where investment planning and tax planning work together like two hands washing each other.

It’s not just what your investments earn that matters—it’s what you get to keep after taxes. With thoughtful planning around the timing and character of your investment income, you can significantly reduce your tax burden while building wealth for the future.

Frequently Asked Questions about Minimizing Tax Strategies for High-Income Earners

What are the most effective tax strategies for high-income earners?

When clients first come to my office, they often ask about the most powerful ways to reduce their tax burden. After decades of experience, I’ve found that the most effective minimize tax strategies for high income earners combine several approaches custom to your specific situation.

Maximizing retirement contributions is usually the first place we start. By fully funding your 401(k), IRA, and other retirement vehicles, you’re essentially giving yourself an immediate tax discount while building wealth for the future. This strategy works for nearly everyone, regardless of your profession or income source.

Strategic income timing can be a game-changer, especially if your income fluctuates year to year. I recently worked with a surgeon who delayed receiving a $75,000 end-of-year bonus until January, keeping her in a lower tax bracket for the current year. This simple timing adjustment saved her over $8,000 in taxes.

Tax-loss harvesting is something many high-income clients overlook, but it’s like finding money hiding in plain sight within your investment portfolio. Even in strong markets, there are usually some underperforming investments that can be strategically sold to offset gains elsewhere.

Charitable giving strategies not only help causes you care about but can significantly reduce your tax burden when structured properly. I’ve seen clients transform their giving approach from simple cash donations to sophisticated strategies involving appreciated securities and donor-advised funds, often doubling the tax benefit of their generosity.

Business ownership structures offer perhaps the most flexible and powerful tax planning opportunities. The tax code provides numerous advantages to business owners that simply aren’t available to W-2 employees.

The most effective approach usually combines multiple strategies customized to your unique financial picture, income sources, and long-term goals.

How can high-income earners minimize taxes through charitable contributions?

Charitable giving is one of the most fulfilling ways to minimize tax strategies for high income earners because it allows you to support causes you care about while also reducing your tax burden. The key is moving beyond simple checkbook philanthropy to more strategic approaches.

Donating appreciated securities rather than cash is my first recommendation for most clients. I remember working with a technology executive who had planned to donate $50,000 cash to her alma mater. Instead, we identified long-held company stock that had appreciated significantly. By donating the stock directly, she avoided paying capital gains tax on the appreciation while still receiving the full fair market value tax deduction. The university received the same value, but she saved an additional $12,000 in taxes compared to selling the stock and donating cash.

Establishing a Donor-Advised Fund (DAF) works beautifully for clients who want to “bunch” their charitable giving. One family I work with typically donates about $20,000 annually to various charities. By contributing $60,000 to a DAF in a single year, they claimed the larger itemized deduction immediately while maintaining their regular giving schedule over the next three years. This strategy became even more valuable after the Tax Cuts and Jobs Act increased the standard deduction.

For clients aged 70½ or older, Qualified Charitable Distributions (QCDs) offer a unique advantage. These allow you to direct up to $108,000 annually from your IRA directly to qualified charities. The distribution satisfies your Required Minimum Distribution requirements without increasing your taxable income. I’ve seen this strategy save clients thousands in taxes while supporting their favorite causes.

Charitable Remainder Trusts can be particularly valuable for clients with highly appreciated assets who also want to create an income stream. These split-interest trusts provide income to you or your beneficiaries for a specified period, with the remainder going to your chosen charity. The immediate partial tax deduction combined with potential capital gains tax avoidance makes this a powerful planning tool for the right situation.

Each of these strategies has specific requirements and limitations, which is why working with a knowledgeable advisor makes all the difference in maximizing both your charitable impact and tax benefits.

What is tax-loss harvesting and how can it benefit high-income individuals?

Tax-loss harvesting is like finding hidden tax deductions within your investment portfolio, and it’s one of my favorite minimize tax strategies for high income clients. The concept is straightforward, but the execution requires attention to detail and careful timing.

In simple terms, tax-loss harvesting means strategically selling investments that have declined in value to realize losses that can offset capital gains and reduce your taxable income. For my high-income clients, this strategy is particularly valuable because they face the highest capital gains tax rates – 20% plus potentially the 3.8% Net Investment Income Tax.

I recently worked with a physician who had realized significant gains from selling a rental property. By reviewing her investment portfolio, we identified several underperforming stock positions that had declined in value. Selling these positions generated losses that offset a substantial portion of her real estate gain, saving her nearly $40,000 in capital gains taxes.

What many people don’t realize is that after offsetting capital gains, up to $3,000 of net capital losses can be used to reduce ordinary income each year. For someone in the 37% federal tax bracket, that’s worth over $1,100 in tax savings annually. Any unused losses can be carried forward indefinitely, creating what I call a tax-loss “bank” for future years.

The beauty of tax-loss harvesting is that it doesn’t have to change your overall investment strategy. By immediately reinvesting the proceeds in similar (but not “substantially identical”) securities, you can maintain your investment allocation while capturing the tax benefits. For example, selling an S&P 500 index fund at a loss and purchasing a total market index fund would likely preserve your investment exposure while locking in the tax loss.

One important caveat to watch for is the wash-sale rule, which disallows losses if you purchase substantially identical securities within 30 days before or after the sale. This is where having professional guidance can help ensure you don’t inadvertently trigger this rule.

At Elite Tax Strategy Solutions, we help clients implement systematic tax-loss harvesting throughout the year, not just during the December rush when everyone else is thinking about taxes. This proactive approach often identifies more opportunities and avoids the market impact of year-end selling pressure.

While tax considerations are important, they should never completely drive your investment decisions. The goal is to optimize after-tax returns while maintaining an appropriate investment strategy for your long-term financial goals.

Conclusion

Navigating the complex world of taxes as a high earner doesn’t have to be overwhelming. With thoughtful planning and the right strategies to minimize tax strategies for high income, you can keep more of your hard-earned money working for you and your family’s future.

Think of tax planning as a year-round conversation rather than a dreaded April deadline. The most successful approach combines multiple strategies custom to your unique financial situation. This isn’t about finding shortcuts—it’s about making the tax code work for you the way it was designed to.

When my clients implement comprehensive tax planning, they typically focus on several key areas. First, they maximize every available tax-advantaged account, from 401(k)s to HSAs, essentially giving themselves an immediate return on investment through tax savings. They’re also thoughtful about when they recognize income and take deductions, sometimes shifting just a few weeks (from December to January, for instance) can make a substantial difference.

Smart investment management plays a crucial role too. I’ve seen clients save thousands through strategic tax-loss harvesting or by incorporating municipal bonds into their portfolios. For those charitably inclined, structured giving not only supports causes they care about but can significantly reduce their tax burden.

Business ownership, when appropriate, opens additional planning opportunities that simply aren’t available to W-2 employees. And for those thinking long-term, estate and gift planning strategies can protect wealth for future generations while potentially reducing current tax liability.

“Reducing your taxes as a high-income earner is critical to build lasting wealth,” notes Sherman Standberry, CPA. I couldn’t agree more—the difference between reactive tax preparation and proactive tax planning often amounts to tens or even hundreds of thousands of dollars over time.

Tax laws are constantly evolving. The potential reduction of the lifetime gift and estate tax exemption in 2026, for example, makes planning in these areas particularly important in the coming years. What works brilliantly today might need adjustment tomorrow.

At Elite Tax Strategy Solutions, we specialize in developing personalized, comprehensive tax strategies for high-income individuals. We don’t view tax planning in isolation—instead, we integrate it with your overall financial goals, ensuring that every tax decision aligns with your broader wealth objectives.

The most important step is simply to begin. Start the conversation early—well before year-end—to maximize your opportunities. Remember: It’s not what you make, but what you keep that truly counts.

To learn more about how we can help you implement these strategies and others custom to your specific situation, visit our More info about Innovative Tax Planning page or contact us for a personalized consultation. We’re here to help you steer the complexities of the tax code with confidence and clarity.