Why High-Income Earners Face Unique Retirement Tax Challenges

Earning a healthy six- or seven-figure income puts you in a great position to save—but it also makes you a magnet for higher taxes today and in retirement. Many professionals assume their tax bill will fall once the paycheques stop. In reality, Required Minimum Distributions (RMDs), Social Security taxation, and Medicare surcharges often keep high-earners in lofty brackets long after they clock out of the workforce.

Key retirement tax strategies for high-income earners:

- Maximise tax-advantaged accounts (401(k), IRA, HSA)

- Deploy advanced Roth tactics (Backdoor & Mega Backdoor Roth)

- Locate assets wisely (put tax-inefficient holdings in tax-deferred accounts)

- Plan ahead for RMDs beginning at age 73

- Manage income and deductions year-by-year

- Stay alert to law changes (TCJA sunset in 2026, shrinking estate exemption)

Without a proactive plan, a “tax time bomb” can explode once RMDs start. Combine forced withdrawals with lifestyle creep and potentially higher future tax rates, and you could pay more to Uncle Sam in retirement than you do today.

I’m David Fritch, CPA and attorney. For four decades I’ve helped clients earning $200,000–$2 million build tax-smart retirement roadmaps that can shave hundreds of thousands off their lifetime tax bill.

Helpful terms at a glance:

- financial planning for high income earners

- tax planning for high earners

- traditional ira for high income earners

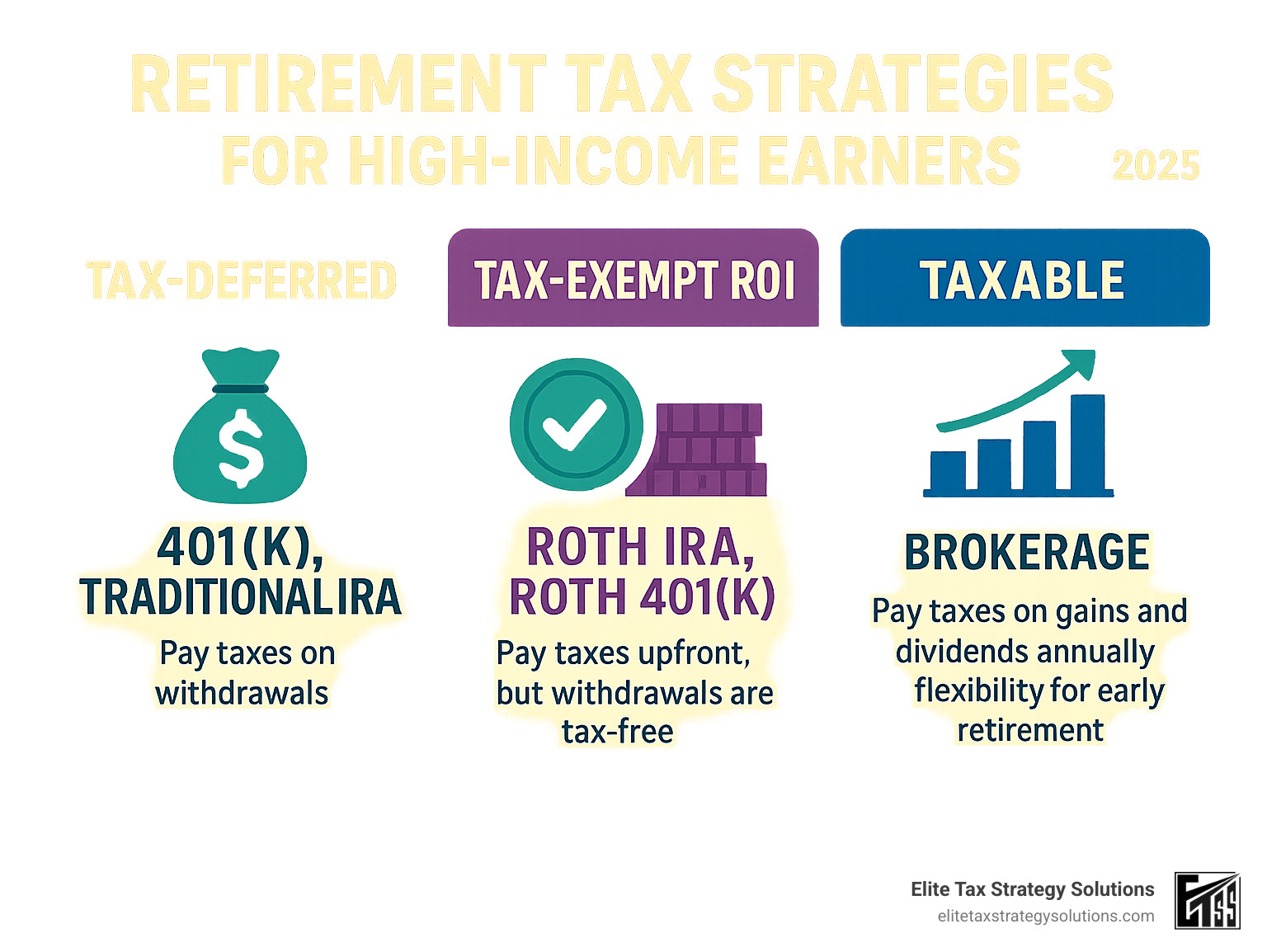

Foundational Tax-Advantaged Accounts to Maximize First

Here’s the truth about retirement tax strategies for high-income earners: you need to walk before you can run. While advanced strategies get all the attention, your foundation determines whether your retirement tax plan succeeds or fails.

Think of these three account types as the three legs of a sturdy stool. Your 401(k) or 403(b) gives you immediate tax relief and employer matching. Your IRA provides additional tax-advantaged space and flexibility. Your HSA offers the ultimate tax trifecta that no other account can match.

The magic happens when you use all three together. This creates what we call tax diversification – having money in pre-tax accounts, Roth accounts, and taxable accounts. In retirement, this gives you the flexibility to manage your tax brackets year by year, potentially saving tens of thousands in taxes.

Most high earners make the mistake of putting all their eggs in one basket – usually their 401(k). But what happens when tax rates go up? Or when Required Minimum Distributions force you into higher tax brackets? You’re stuck with whatever tax rates exist at that time.

Our Tax-Efficient Retirement Planning services help you build this foundation properly from the start.

Max Out Your Employer-Sponsored Plan (401(k), 403(b))

Your workplace retirement plan should be your first stop, especially if you’re a high earner. The contribution limits are substantial, and they just got better for people approaching retirement.

For 2025, you can contribute $23,500 to your 401(k) or 403(b). But here’s where it gets exciting – the catch-up contribution rules have been completely revamped to help high earners who hit their peak earning years later in life.

If you’re ages 50-59, you can add an extra $7,500 in catch-up contributions, bringing your total to $31,000. But if you’re ages 60-63, you get an even bigger boost – an additional $11,250 in catch-up contributions, for a total of $34,750.

This improved catch-up for ages 60-63 is a game-changer. It recognizes that many high earners don’t hit their stride until their late 50s and early 60s. Now you have extra time to make up for any earlier years when you couldn’t save as much.

Don’t overlook your employer match – it’s the closest thing to free money you’ll find. If your company matches 50% of your contributions up to 6% of your salary, that’s an immediate 50% return on your investment. No stock, bond, or real estate investment can guarantee those returns.

Many plans now offer a Roth 401(k) option, which can be particularly smart for high earners. You pay taxes now at known rates rather than gambling on what tax rates will be in 20 or 30 years. Given the federal debt and potential for higher future tax rates, this can be a wise hedge.

The 2025 contribution limits from the IRS provide all the official details if you want to dive deeper.

Fully Fund Your Individual Retirement Accounts (IRAs)

Even if you’re maxing out your 401(k), you should still fund an IRA. The 2025 contribution limit is $7,000, plus a $1,000 catch-up contribution if you’re 50 or older.

Here’s where things get tricky for high earners. The government doesn’t want to give unlimited tax breaks to people who earn substantial incomes, so they’ve created income limits for direct Roth IRA contributions.

For 2025, direct Roth IRA contributions phase out at relatively modest income levels. Single filers lose the ability to contribute directly between $150,000 and $165,000 of income. Married couples filing jointly face phase-outs between $236,000 and $246,000.

If you earn above these thresholds, you can’t contribute directly to a Roth IRA. But don’t worry – there’s a perfectly legal workaround called the Backdoor Roth IRA that we’ll cover in the next section.

You can always make non-deductible contributions to a Traditional IRA regardless of your income level. While you won’t get an immediate tax deduction, the money still grows tax-deferred, and it sets you up for the Backdoor Roth strategy.

Our guide on Traditional IRA for High-Income Earners walks through the specific strategies for navigating these income restrictions.

Leverage a Health Savings Account (HSA) as a Triple-Tax-Advantaged Tool

The HSA is hands-down the most tax-advantaged account in the entire tax code. It’s the only account that offers triple tax advantages: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

For 2024, you can contribute $4,150 for individual coverage or $8,300 for family coverage. If you’re 55 or older, you get an additional $1,000 catch-up contribution.

Here’s the secret that transforms your HSA from a medical account into a retirement powerhouse: after age 65, you can withdraw HSA funds for any purpose without penalty. You’ll pay ordinary income tax on non-medical withdrawals, but that’s the same as a Traditional IRA.

The difference? If you use HSA funds for medical expenses, the withdrawals remain completely tax-free even after age 65. Given that healthcare costs are one of the largest expenses in retirement, this becomes incredibly valuable.

Consider this: the average couple retiring today will need approximately $300,000 to cover healthcare costs in retirement. Having a dedicated account that grows tax-free and can be withdrawn tax-free for these expenses is like having a healthcare pension.

The strategy for high earners is to pay current medical expenses out of pocket and let your HSA grow untouched. Think of it as a stealth retirement account that happens to have amazing medical benefits.

For advanced strategies on maximizing your HSA in retirement, check out our guide on Extending Your Health Savings Account HSA Contributions Beyond Age 65.

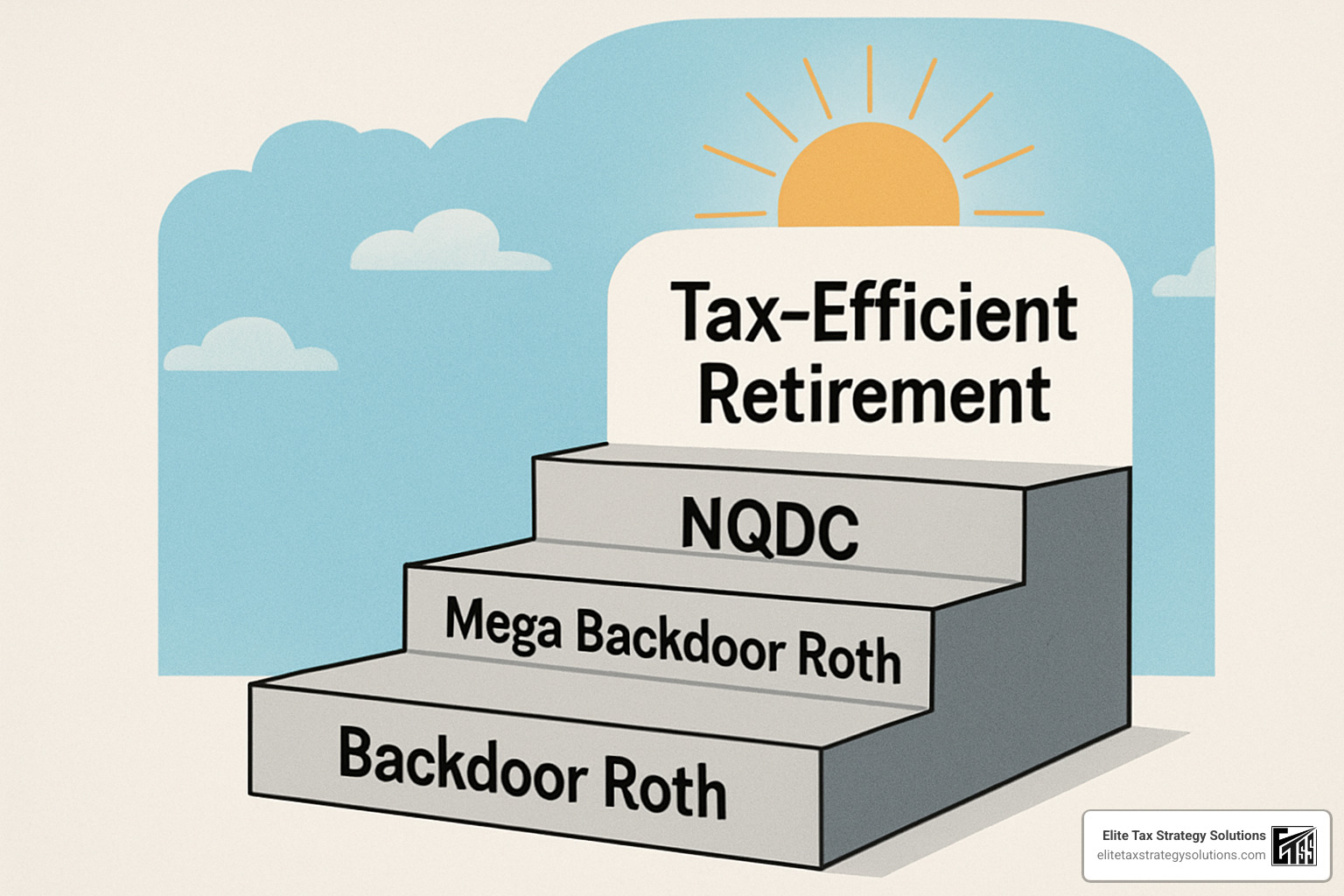

Advanced Retirement Tax Strategies for High-Income Earners

Once your 401(k), IRA and HSA are fully funded, it’s time to open up the “secret menu” designed for top earners. Used correctly, these tactics can funnel tens of thousands of after-tax dollars into accounts that will never be taxed again.

For personalised help, see our Retirement Tax Strategies for High-Income Earners services.

Backdoor Roth IRA: Sneak Past the Income Limits

- Contribute up to $7,000 (2025) to a non-deductible Traditional IRA.

- Convert the contribution to a Roth IRA right away.

- Avoid the pro-rata trap by rolling any existing pre-tax IRA money into your employer plan before converting.

Result: Unlimited income earners get decades of tax-free growth.

Mega Backdoor Roth: Super-Size Your Roth Savings

If your 401(k) allows after-tax contributions and in-service conversions, you can contribute up to the overall plan limit of $69,000 ($76,500 age 50+) in 2024. After filling the regular $23,500 employee slot and receiving any employer match, the rest can be pushed into after-tax and then swept into a Roth IRA or Roth 401(k). One move, potentially $30k–$50k per year in new Roth dollars.

Confirm your plan’s rules with HR before attempting this strategy.

Non-Qualified Deferred Compensation (NQDC): Time-Shift Your Pay

High-income employees can defer hefty bonuses or salary into a corporate NQDC plan, paying tax later—ideally in a lower bracket. Caution: plans are an unfunded promise of the employer, so evaluate company stability and distribution schedules before committing.

Asset Location: Put Each Investment in Its Ideal Home

- Tax-inefficient assets (bond funds, REITs) → 401(k)/IRA

- Tax-efficient assets (ETFs, broad index funds) → taxable brokerage

- Highest-growth assets → Roth accounts

Proper location can add 0.2%–0.5% to annual after-tax returns. Learn more in our Tax-Efficient Investments guide.

Key reference: IRS 401(k) contribution limits.

Leveraging Other Financial Tools for a Tax-Smart Retirement

Retirement tax planning doesn’t stop at qualified accounts. Here are three supplemental tactics that integrate easily with a high-income plan.

Harvest Tax Losses in Your Brokerage Account

Sell positions trading below cost to offset current capital gains, then reinvest in a similar (not “substantially identical”) holding to maintain market exposure. Up to $3,000 of net losses can offset ordinary income, and unused losses carry forward indefinitely. See the IRS capital-gains overview for details.

Give Your Kids a Head-Start With the New 529-to-Roth Rollover

SECURE 2.0 now lets unused 529 funds—up to $35,000 over a lifetime—roll into a beneficiary’s Roth IRA once the account is 15 years old. Annual rollovers are capped at the IRA contribution limit and the child must have earned income, but the rule converts leftover college savings into a tax-free retirement nest egg.

Make Charitable Gifts Work Harder

- Qualified Charitable Distributions (QCDs): Donate up to $100,000 per year directly from your IRA starting at age 70½ and reduce your taxable RMD dollar-for-dollar.

- Donate appreciated stock: Avoid capital-gains tax and receive a deduction for fair-market value.

- Donor-Advised Funds (DAFs): Bunch several years of contributions into one high-income year, then grant to charities over time.

For broader planning help, visit our Financial Planning for High-Income Earners page.

Proactive Planning for Law Changes and Wealth Transfer

Here’s something most high earners don’t realize: the tax laws you’re planning around today won’t be the same ones you’ll retire under. If you’re not preparing for these changes now, you could be in for some unpleasant surprises.

Think of it like this – you wouldn’t drive across the country without checking the weather forecast, right? The same principle applies to retirement tax strategies for high-income earners. You need to know what’s coming down the road.

The biggest mistake I see clients make is assuming current tax laws will stay the same. They won’t. Several major changes are already scheduled, and being proactive about them can save you hundreds of thousands of dollars.

For comprehensive guidance on staying ahead of these changes, explore our Proactive Tax Planning services.

Prepare for Upcoming Tax Law Changes

Let’s talk about the big changes that are already on the books. These aren’t maybes – they’re scheduled to happen unless Congress acts.

The Tax Cuts and Jobs Act (TCJA) expires in 2026, and when it does, tax rates will jump back up. The current 37% top rate will revert to 39.6%, and that’s just the beginning. The standard deduction will be cut roughly in half, which means many high earners will suddenly find themselves itemizing again.

Here’s what makes this particularly challenging: the state and local tax (SALT) deduction cap might be removed, but higher federal rates could offset any benefits. It’s like getting a discount at a store that just raised all its prices.

Required Minimum Distribution ages keep changing too. We went from 70½ to 72, then to 73 in 2023, and it’s scheduled to hit 75 in 2033. While this gives you more time for tax-deferred growth, it also compresses your withdrawal period once RMDs begin.

The estate tax exemption is perhaps the most dramatic change coming. Right now, you can pass $13.99 million per person to your heirs without federal estate tax. In 2026, that drops to approximately $7 million per person. For married couples, that’s potentially $14 million less they can transfer tax-free.

What does this mean for your planning? Consider Roth conversions before 2026 while rates are still lower. Accelerate estate planning strategies before exemptions drop. And most importantly, plan for potentially higher tax rates in retirement, not lower ones.

Our High Net Worth Tax Planning services can help you steer these complex changes.

Time Your Income and Deductions Strategically

Smart timing of income and deductions is like conducting an orchestra – everything needs to work together to create harmony. For high earners, this becomes even more important because you have more control over when you receive income and more opportunities to optimize.

Income timing is all about managing your tax brackets year by year. Maybe you can defer that bonus to next year if you expect to be in a lower bracket. Or perhaps you should accelerate income into this year if you think rates are going up. Stock option exercises can be spread over multiple years to avoid pushing yourself into higher brackets all at once.

NQDC plans are particularly powerful here because they let you defer large compensation amounts to years when you’ll be in lower tax brackets. It’s like having a time machine for your income.

On the deduction side, bunching charitable contributions into high-income years can be incredibly effective. Instead of giving $10,000 annually to charity, consider giving $50,000 every five years when your income spikes.

Roth conversions deserve special attention in your timing strategy. The best time to convert is when your income is unusually low – maybe you took a sabbatical, retired early, or had a down year in your business. Market downturns can also create excellent conversion opportunities because you’re converting shares at depressed values.

Don’t forget about the Net Investment Income Tax (NIIT) – that 3.8% surtax on investment income above $200,000 for singles or $250,000 for married couples. Strategic timing can help you manage this threshold too.

Integrate Estate and Wealth Transfer Planning

For high earners, estate planning isn’t just about avoiding taxes when you die – it’s about efficiently transferring wealth while you’re alive and minimizing the overall tax burden on your family.

The current lifetime gift and estate tax exemption of $13.99 million per person in 2025 is historically high, but it’s temporary. The annual gift tax exclusion of $19,000 per recipient gives you additional transfer opportunities each year.

Spousal Lifetime Access Trusts (SLATs) allow you to transfer assets out of your estate while maintaining some access through your spouse. Grantor Retained Annuity Trusts (GRATs) let you transfer appreciation to heirs while keeping an income stream. These strategies sound complex, but they’re incredibly powerful for the right situations.

Here’s the urgency: the current high exemption amounts are scheduled to be cut roughly in half in 2026. This creates a limited window to take advantage of these historically high exemptions.

Let me give you a real-world example. A married couple with a $20 million estate could transfer $14 million to their children in 2025 using their combined exemptions. If they wait until 2026, they might only be able to transfer $7 million without paying gift taxes. That’s a $7 million difference in tax-free transfers.

The generation-skipping transfer tax exemption is also $13.99 million per person, which means you can transfer significant wealth to grandchildren without triggering additional taxes.

For sophisticated wealth transfer strategies, explore our Wealth Management Tax Planning services.

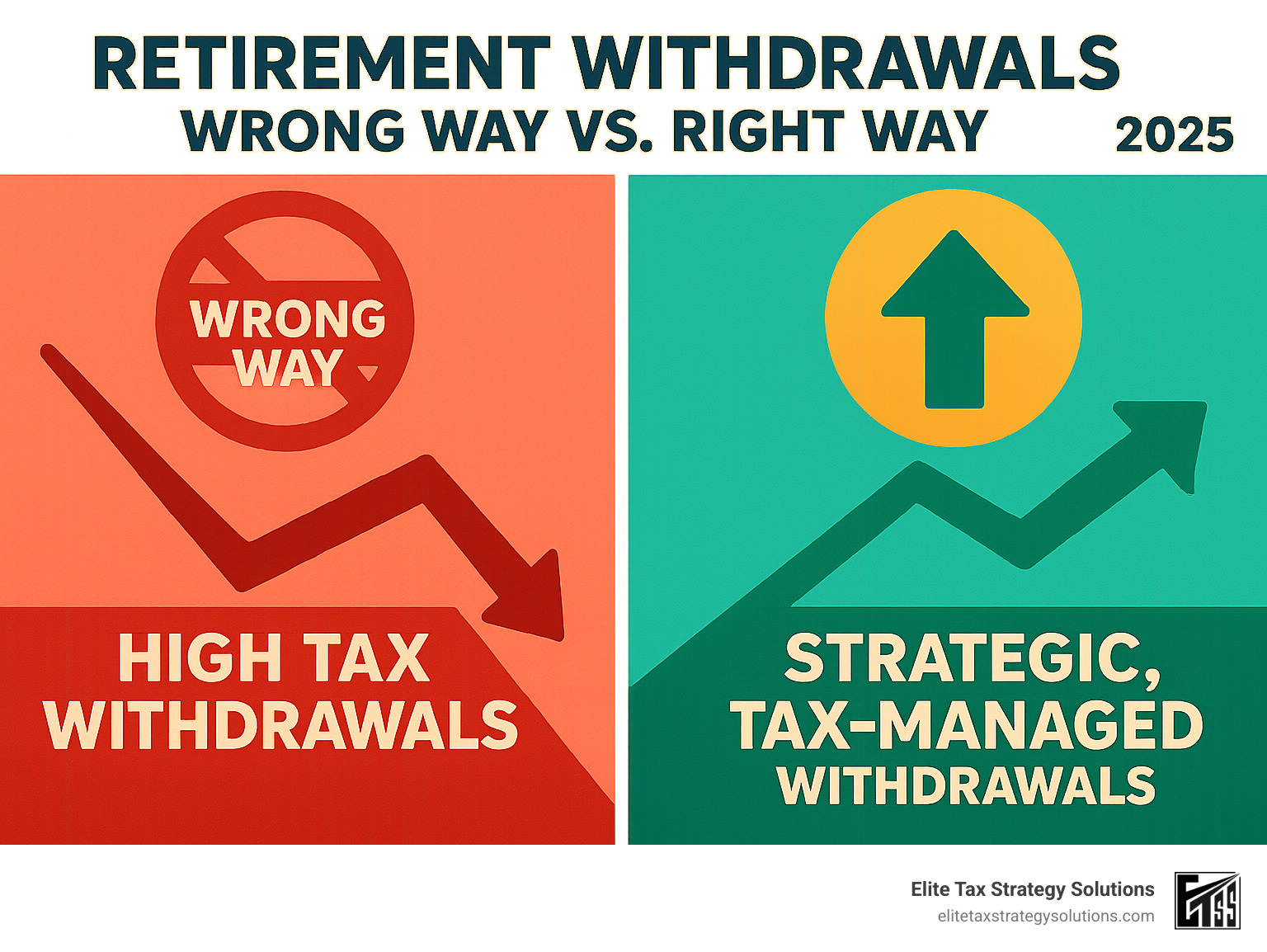

Avoiding Common Mistakes and Mastering Your Withdrawal Strategy

Five Costly Mistakes Wealthy Retirees Make

- Saving only in pre-tax accounts—leaves you hostage to future tax rates.

- Ignoring RMDs—forced withdrawals can catapult you into higher brackets.

- Assuming taxes will be lower later—often false for high-balance savers.

- Letting lifestyle creep crowd out saving—target 15-20% of gross income.

- Over-saving and under-living—balance tomorrow’s security with today’s joy.

A Simple Yet Powerful Withdrawal Order

- Taxable accounts first – harvest gains at favourable capital-gains rates.

- Tax-deferred (Traditional 401(k)/IRA) – manage withdrawals to “fill” but not overflow each bracket and control Medicare IRMAA.

- Roth last – no RMDs, so let tax-free growth compound as long as possible.

Early retiree? Consider a Roth conversion ladder: move a slice of Traditional IRA money to Roth each year in your 50s or early 60s, wait five years, then draw the converted principal without penalty.

Smart decumulation can save hundreds of thousands over a 30-year retirement. For customised guidance, explore our Tax Planning Strategies for High-Income Earners services.

Conclusion

Think of retirement tax strategies for high-income earners as building a custom roadmap for your financial future. You wouldn’t drive cross-country without a map, and you shouldn’t approach retirement without a comprehensive tax strategy that goes far beyond simply maxing out your 401(k).

The strategies we’ve explored together – from building that solid foundation with tax-advantaged accounts to implementing sophisticated techniques like Mega Backdoor Roth conversions and strategic withdrawal planning – aren’t just theoretical concepts. They’re proven methods that can save you hundreds of thousands of dollars in taxes over your lifetime.

The most important takeaway? High-income earners need to think holistically about their retirement planning. This means building a tax-diversified foundation by maximizing contributions to all available accounts, not just the obvious ones. It means implementing advanced strategies like Backdoor Roth IRAs and NQDC plans when your income allows it.

But it doesn’t stop there. You need to prepare for upcoming tax law changes – the TCJA sunset in 2026 and estate tax exemption reductions aren’t distant possibilities, they’re coming whether we’re ready or not. And perhaps most critically, you need to create a smart withdrawal strategy that manages your tax brackets throughout retirement and minimizes your lifetime tax burden.

The biggest mistake I see high earners make is avoiding common pitfalls like failing to plan for RMDs or putting all their eggs in the pre-tax savings basket. These seemingly small oversights can turn into massive tax headaches later.

Here’s the reality: for high-income earners, a personalized tax strategy isn’t a luxury – it’s absolutely essential. The tax code is incredibly complex and constantly evolving. The stakes are simply too high to leave your retirement security to chance or generic advice.

At Elite Tax Strategy Solutions, we’ve spent decades helping high-income earners and closely held businesses steer these exact challenges. Our proactive approach to tax optimization and compliance has helped clients save tens of thousands of dollars annually while building secure, tax-efficient retirement plans that actually work in the real world.

Whether you’re just hitting your stride in your career or you can see retirement on the horizon, the time to implement these strategies is right now. The power of compound growth and tax savings means that every year you delay could cost you thousands down the road.

The best retirement tax strategies for high-income earners are those that become part of your financial DNA – implemented consistently over time, adapted as your circumstances change, and fully integrated into your overall financial plan. Don’t wait until you’re already retired to start thinking about taxes. Start planning today for the retirement you’ve worked so hard to earn.

Ready to take control of your retirement tax strategy? Develop your innovative tax plan with us and find how our personalized approach can help you retire comfortably without handing Uncle Sam a fortune in the process.