High income self employed tax strategies are crucial for individuals who aim to maximize their deductions and maintain financial stability amid complex tax obligations. If you’re seeking swift insights, here are some quick strategies:

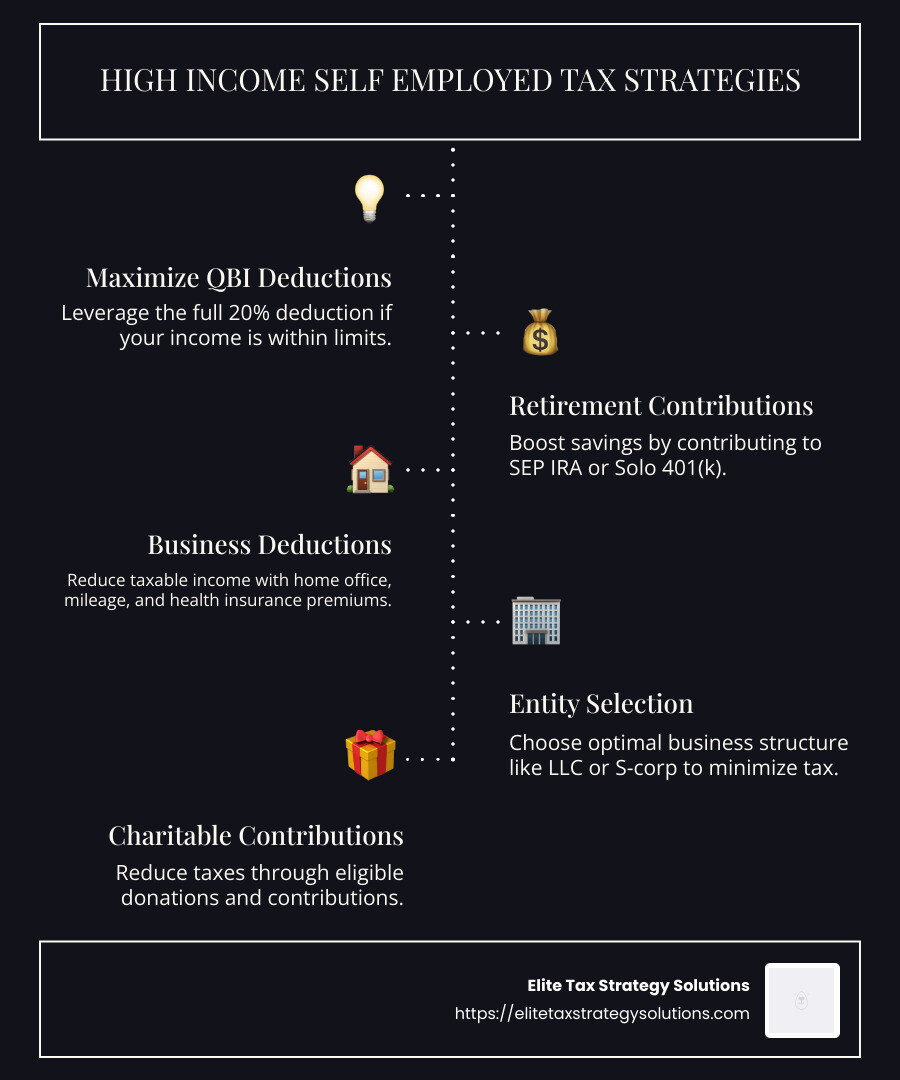

- Maximize Qualified Business Income (QBI) Deductions: Claim the full 20% deduction if your income is within the limits.

- Retirement Contributions: Boost tax savings by contributing to self-employed retirement plans like SEP IRA or Solo 401(k).

- Business Deductions: Leverage allowable business expenses like home office, mileage, and health insurance premiums to reduce taxable income.

- Entity Selection: Choose the optimal business structure (LLC, S-corp) to minimize tax liability.

For high-income earners transitioning to self-employment, understanding tax deductions and implications is key to maintaining financial stability.

My name is David Fritch, and with 40 years in tax strategy and small business management, I’ve dedicated my career to helping individuals steer the complexities of high income self employed tax strategies. My expertise is in uncovering tax savings opportunities to improve your financial well-being.

High income self employed tax strategies vocab to learn:

– tax planning for freelancers

– business tax planning strategies

– high income tax reduction strategies

Understanding Self-Employment Tax Obligations

Being self-employed means you’re in charge of your own taxes. Unlike regular employees, no one withholds taxes from your paycheck. This section will help you understand quarterly payments, Schedule C, Schedule SE, and estimated taxes.

Quarterly Payments

As a self-employed individual, you have to pay taxes four times a year. These are called quarterly payments. They cover your income tax and self-employment tax, which includes Social Security and Medicare taxes. If you don’t pay enough throughout the year, you might face penalties. The IRS sets the penalty rate at 8% as of 2024 for underpaid taxes.

To avoid penalties, use the IRS Form 1040-ES to calculate your estimated taxes. This form helps you figure out how much you owe each quarter. If your income changes, adjust your payments by re-calculating with the form. It’s better to slightly overestimate your taxes to avoid penalties.

Schedule C and Schedule SE

When you file your taxes, you’ll need to use Schedule C and Schedule SE.

-

Schedule C: This form reports your business income and expenses. It helps you figure out your net profit or loss. This net income is then added to your personal tax return.

-

Schedule SE: This form calculates your self-employment tax. It covers both the employee and employer portions of Social Security and Medicare taxes. The rate is 15.3% of your net earnings.

Keeping good records of your income and expenses is crucial. They help ensure you claim all possible deductions and accurately report your earnings.

Estimated Taxes

Estimated taxes are how you pay your taxes throughout the year. Since you’re self-employed, no employer withholds taxes for you. Use the IRS Form 1040-ES worksheet to figure out your estimated taxes.

Tip: Keep a running tally of your income and expenses. Regularly update your estimated payments to match your earnings. This helps avoid a big tax bill at the end of the year.

Understanding these tax obligations is essential for managing your finances and avoiding costly penalties. In the next section, we’ll dive into high income self employed tax strategies to help you save even more.

High Income Self Employed Tax Strategies

Being self-employed offers flexibility and the potential for high earnings, but it also comes with a hefty tax bill. Luckily, there are several strategies to help high-income self-employed individuals keep more of their hard-earned money. Let’s explore some key tactics, focusing on retirement contributions, health savings accounts, and business write-offs.

Retirement Contributions

Contributing to retirement accounts is a powerful way to reduce taxable income. For self-employed individuals, options like the SEP IRA and Solo 401(k) can be particularly beneficial.

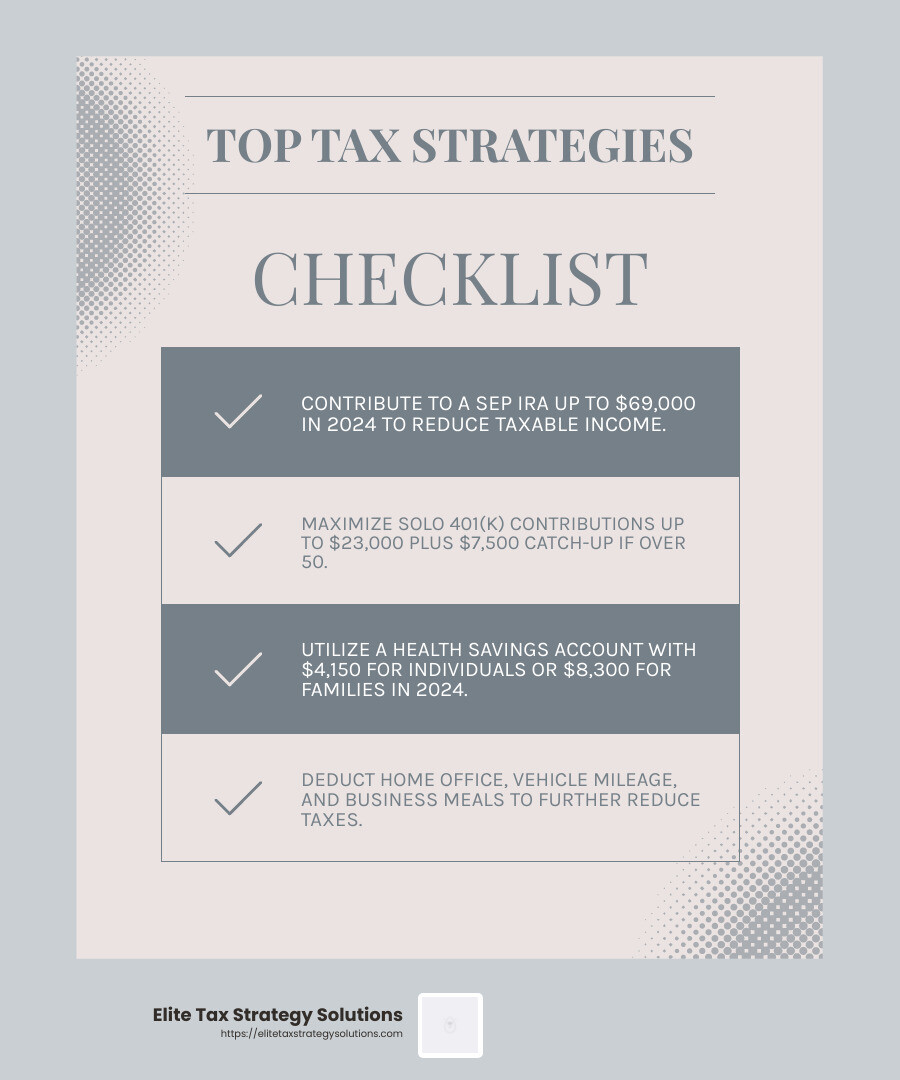

- SEP IRA: In 2024, you can contribute up to 25% of your net earnings or $69,000, whichever is less. This amount is increasing to $70,000 in 2025. Contributions are tax-deferred, meaning you don’t pay taxes until you withdraw the funds during retirement.

- Solo 401(k): This plan allows contributions as both an employer and an employee. In 2024, you can contribute up to $23,000, with an additional $7,500 catch-up contribution if you’re over 50. This can significantly lower your taxable income.

Health Savings Accounts (HSAs)

An HSA is another excellent tool for tax savings if you have a high-deductible health plan. Contributions are tax-deductible, and withdrawals for qualified medical expenses are tax-free.

- In 2024, you can contribute up to $4,150 for individual coverage or $8,300 for family coverage. These limits increase slightly in 2025. Contributions reduce your taxable income, and the funds grow tax-free, providing a triple tax advantage.

Business Write-Offs

Maximizing business deductions can greatly reduce your taxable income. Here are some key write-offs to consider:

- Home Office Deduction: If you use part of your home exclusively for business, you can deduct a portion of your mortgage, rent, utilities, and more.

- Vehicle Mileage: Keep track of every business mile driven. In 2024, the standard mileage rate is 58 cents per mile. Accurate records are crucial for maximizing this deduction.

- Business Meals: Generally, you can deduct 50% of meal expenses if the meal is business-related. Keep receipts and note the business purpose of each meal.

Implementing these high income self employed tax strategies can significantly lower your tax bill and boost your financial stability. Keep reading to learn how to maximize deductions for self-employed individuals.

Maximizing Deductions for Self-Employed Individuals

As a self-employed individual, maximizing deductions is key to reducing your tax bill. Here are some of the most effective deductions you can leverage:

Home Office Deduction

If you work from home, you might qualify for the home office deduction. This allows you to deduct a portion of your home expenses, like rent, utilities, and insurance, if you use part of your home exclusively for business.

- Eligibility: The space must be used regularly and exclusively for your business.

- Calculation: You can use the simplified option, which is $5 per square foot, up to 300 square feet, or calculate actual expenses.

Vehicle Mileage

Tracking your business mileage can lead to significant deductions. The IRS allows a standard mileage rate deduction, which is simpler than keeping track of actual expenses like gas and maintenance.

- Rate: In 2023, the standard mileage rate is 65.5 cents per mile.

- Record Keeping: Keep detailed records of each business trip, including the date, mileage, and purpose.

Health Insurance Premiums

Paying for your own health insurance? You can deduct the premiums for yourself, your spouse, and your dependents.

- Eligibility: You must not be eligible for a plan through an employer or a spouse’s employer.

- Coverage: This includes health, dental, and qualified long-term care insurance premiums.

Business Meals

Business meals can also be deductible, but there are rules to follow. Generally, you can deduct 50% of the cost of meals that are directly related to your business.

- Requirements: The meal must be ordinary and necessary, and not extravagant.

- Documentation: Keep receipts and record the business purpose and attendees.

Implementing these deductions can help you keep more of your earnings and invest back into your business. Next, we’ll explore how choosing the right business structure can further optimize your tax situation.

Choosing the Right Business Structure

Choosing the right business structure is crucial for high-income self-employed individuals. The structure you select impacts your taxes, liability, and even how you can grow your business. Let’s explore the most common options: sole proprietorship, LLC, S Corporation, and partnership.

Sole Proprietorship

A sole proprietorship is the simplest and most common structure for self-employed individuals. It’s easy to set up and doesn’t require formal registration. However, there’s a downside: no legal separation between you and your business.

- Taxes: Your business income is reported on your personal tax return using Schedule C.

- Liability: You are personally liable for all business debts and obligations.

While a sole proprietorship is easy to manage, the lack of liability protection can be risky, especially for high earners.

LLC (Limited Liability Company)

Forming a Limited Liability Company (LLC) provides a layer of protection by separating personal and business assets. This structure is favored for its flexibility and liability protection.

- Taxes: An LLC is typically taxed like a sole proprietorship for single-member LLCs, with income passing through to your personal tax return.

- Liability: Offers protection by keeping your personal assets separate from business liabilities.

An LLC is often a good fit for those looking to reduce personal risk while maintaining administrative simplicity.

S Corporation

An S Corporation (S Corp) is a bit more complex but offers potential tax advantages. It allows you to split income into salary and distributions, potentially reducing self-employment taxes.

- Taxes: Must file a separate business tax return. Shareholders report income on personal tax returns.

- Liability: Provides liability protection similar to an LLC.

S Corps require more rigorous bookkeeping and payroll processing, making them suitable for those prepared to handle increased administrative duties.

Partnership

If you’re going into business with others, a partnership might be the right choice. Partnerships allow multiple people to co-own a business and share profits and losses.

- Taxes: Partnerships file an informational return but do not pay income taxes. Instead, profits and losses pass through to partners’ personal tax returns.

- Liability: General partners are personally liable, but limited partnerships can offer some liability protection.

Partnerships offer flexibility in profit-sharing but require careful planning and agreements to ensure smooth operations.

Choosing the right business structure can have a significant impact on your tax situation and personal liability. It’s not just about today’s needs but also about future growth and changes. Next, we’ll explore the best retirement plans for self-employed high earners.

Top Retirement Plans for Self-Employed High Earners

When you’re self-employed and earning a high income, planning for retirement can be both a challenge and an opportunity. You have the freedom to choose from several retirement plans, each with its own benefits. Let’s explore SEP IRAs, Solo 401(k)s, SIMPLE IRAs, and defined benefit plans to help you find the best fit for your financial future.

SEP IRA

A Simplified Employee Pension (SEP) IRA is a popular choice for self-employed individuals due to its high contribution limits and straightforward setup.

- Contribution Limits: You can contribute up to 25% of your net earnings from self-employment, capped at $69,000 for 2024. This makes it ideal for high-income earners who want to maximize their retirement savings.

- Flexibility: Contributions are not mandatory every year, allowing for flexibility based on your financial situation.

- Tax Benefits: Contributions are tax-deductible, which can significantly reduce your taxable income.

SEP IRAs are especially beneficial for those who don’t have employees, as contributions for employees must be equal to the percentage contributed to your own account.

Solo 401(k)

The Solo 401(k), also known as a one-participant 401(k), is custom for self-employed individuals without employees, except perhaps a spouse.

- Contribution Limits: You can contribute as both an employer and an employee. This means you can defer up to $22,500 as an employee in 2024 (plus a $7,500 catch-up if you’re over 50) and add up to 25% of your net earnings as an employer, up to a total of $69,000.

- Loan Option: Unlike some other plans, a Solo 401(k) may allow you to borrow against your savings.

- Roth Option: Offers the ability to make Roth contributions, which means tax-free withdrawals in retirement.

This plan is perfect for those who want to maximize contributions and take advantage of both tax-deferred and Roth options.

SIMPLE IRA

A Savings Incentive Match Plan for Employees (SIMPLE) IRA is designed for small businesses and self-employed individuals, offering an easy way to save for retirement.

- Contribution Limits: You can contribute up to $16,000 in 2024, with a $3,500 catch-up contribution if you’re 50 or older.

- Employer Contributions: Employers must either match employee contributions up to 3% of their compensation or make a 2% nonelective contribution.

- Ease of Setup: SIMPLE IRAs are easy to establish and have lower administrative costs than some other plans.

SIMPLE IRAs are a good fit for those who want a straightforward plan with mandatory employer contributions.

Defined Benefit Plans

For those looking to save significantly more for retirement, a defined benefit plan might be the way to go. These plans promise a specific benefit at retirement, based on factors like salary and years of service.

- Contribution Limits: Contributions are based on the benefit you want to receive, which can be as high as $409,000 annually.

- Predictable Income: Offers a predictable retirement income, which can be appealing for those who want certainty.

- Tax Advantages: Contributions are tax-deductible, and the plan grows tax-deferred.

Defined benefit plans are ideal for high-income earners who want to defer a large portion of their income and can manage the complexity and cost of maintaining the plan.

Choosing the right retirement plan is crucial for optimizing your savings and minimizing taxes. Whether you prefer the flexibility of a SEP IRA or the high contribution limits of a defined benefit plan, there’s an option that fits your needs. Next, we’ll answer some frequently asked questions about high-income self-employed tax strategies.

Frequently Asked Questions about High Income Self Employed Tax Strategies

How can I avoid high self-employment tax?

If you’re self-employed, you’re likely aware of the hefty self-employment tax. But there are ways to ease this burden. One effective strategy is to increase your retirement contributions. For instance, contributing to a SEP IRA allows you to stash away up to 25% of your net earnings, reducing your taxable income and, consequently, your self-employment tax.

Another option is a Solo 401(k), where you can contribute both as an employer and employee. This setup provides significant tax-deferred savings potential, especially beneficial for high-income earners.

Additionally, consider leveraging a Health Savings Account (HSA), which offers triple tax benefits: contributions are tax-deductible, growth is tax-free, and withdrawals for medical expenses are also tax-free.

How to get the biggest tax refund when self-employed?

To maximize your tax refund, focus on maximizing write-offs. Keep meticulous records of all business expenses, including home office deductions, vehicle mileage, and business meals. These costs can add up significantly, lowering your taxable income.

You can also reduce business income through strategic purchases and expenses, like investing in new equipment or software before the tax year ends. This not only improves your business operations but also provides immediate tax benefits.

How can high-income earners reduce taxes?

High-income earners have several avenues to explore for reducing taxes. One powerful method is through charitable contributions. Donating appreciated assets not only supports your favorite causes but also provides a double tax benefit: you avoid capital gains tax and receive a deduction for the asset’s full market value.

Another strategy involves real estate losses. If you have investment properties, you can offset income with depreciation and other real estate-related expenses. This can create a tax advantage, especially if you’re actively involved in managing the properties.

By employing these strategies, you can effectively manage your tax obligations and keep more of your hard-earned money. Next, we’ll explore how choosing the right business structure can further optimize your tax situation.

Conclusion

Navigating taxes as a high-income self-employed individual can be challenging. But with the right tax planning strategies, you can significantly reduce your tax burden and improve your financial stability.

Engaging with skilled financial advisors is crucial. They can help you identify opportunities to maximize your deductions and use tax-saving tools like retirement accounts and health savings accounts. Tax planning is not just about compliance; it’s about proactively managing your financial future.

At Elite Tax Strategy Solutions, we specialize in personalized tax planning services for high earners and closely held businesses. Our expert team is dedicated to helping you optimize your tax situation and achieve long-term financial success. We take a thorough, proactive approach to ensure your tax strategy aligns with your financial goals.

Whether you’re looking to make the most of your retirement contributions, explore business write-offs, or choose the best business structure, we’re here to guide you every step of the way. With locations in Jasper, Indiana, and suburban areas near major cities, we’re accessible and ready to assist.

Don’t leave your tax savings to chance. Partner with us to develop a comprehensive tax strategy that keeps more of your hard-earned money in your pocket. Contact Elite Tax Strategy Solutions today to start planning for a brighter financial future.