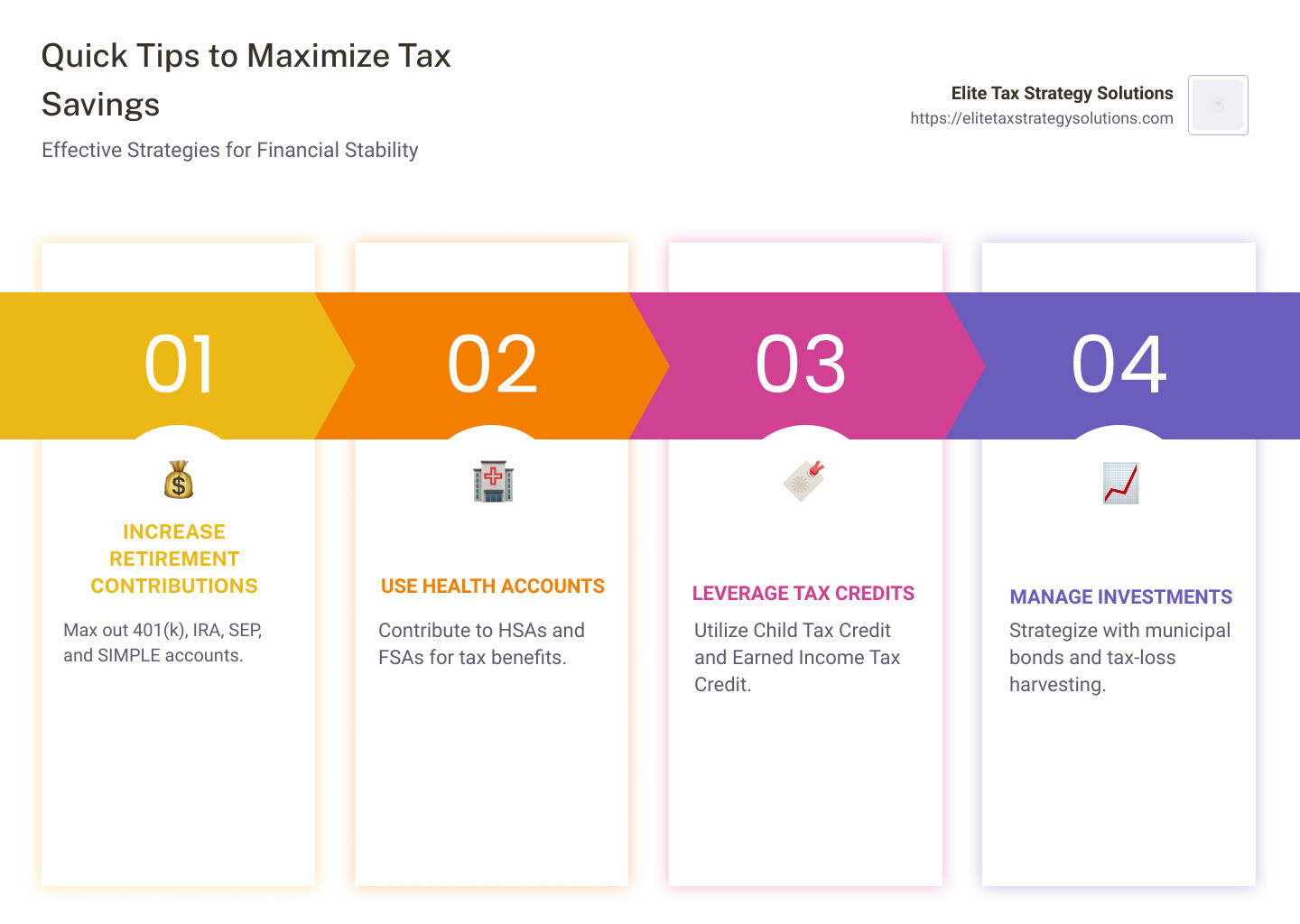

Maximize tax savings is a strategic approach to tax planning that can offer substantial financial stability and improved outcomes. By implementing proactive strategies, you can significantly reduce your tax liabilities and retain more of your hard-earned money. Here’s a quick overview of ways to maximize tax savings:

- Increase retirement contributions: Use 401(k), IRA, SEP, and SIMPLE accounts.

- Contribute to health savings accounts (HSA) or flexible spending accounts (FSA).

- Leverage available tax credits and deductions: Child Tax Credit, Earned Income Tax Credit, charitable donations.

- Manage investments and capital gains strategically: Use municipal bonds and tax-loss harvesting.

Tax planning is not a once-a-year task but a continuous effort to align your financial goals with your tax strategy. With frequent changes in tax laws, staying informed and adjusting strategies is vital for long-term financial success.

I’m David Fritch, your guide to steer the complexities of tax planning with 40 years of experience helping clients maximize tax savings. My expertise comes from running my CPA practice and working with high-earning individuals and small business owners to reduce stress and optimize financial outcomes.

Learn more about maximize tax savings:

– business tax reduction

– high-income tax planning

– tax planning for small businesses

Maximize Tax Savings with Retirement Contributions

Retirement contributions are a powerful tool to maximize tax savings while securing your future. Whether you’re an employee or self-employed, understanding how to leverage accounts like 401(k)s, IRAs, SEP, and SIMPLE IRAs can make a significant difference in your tax bill.

401(k) Plans

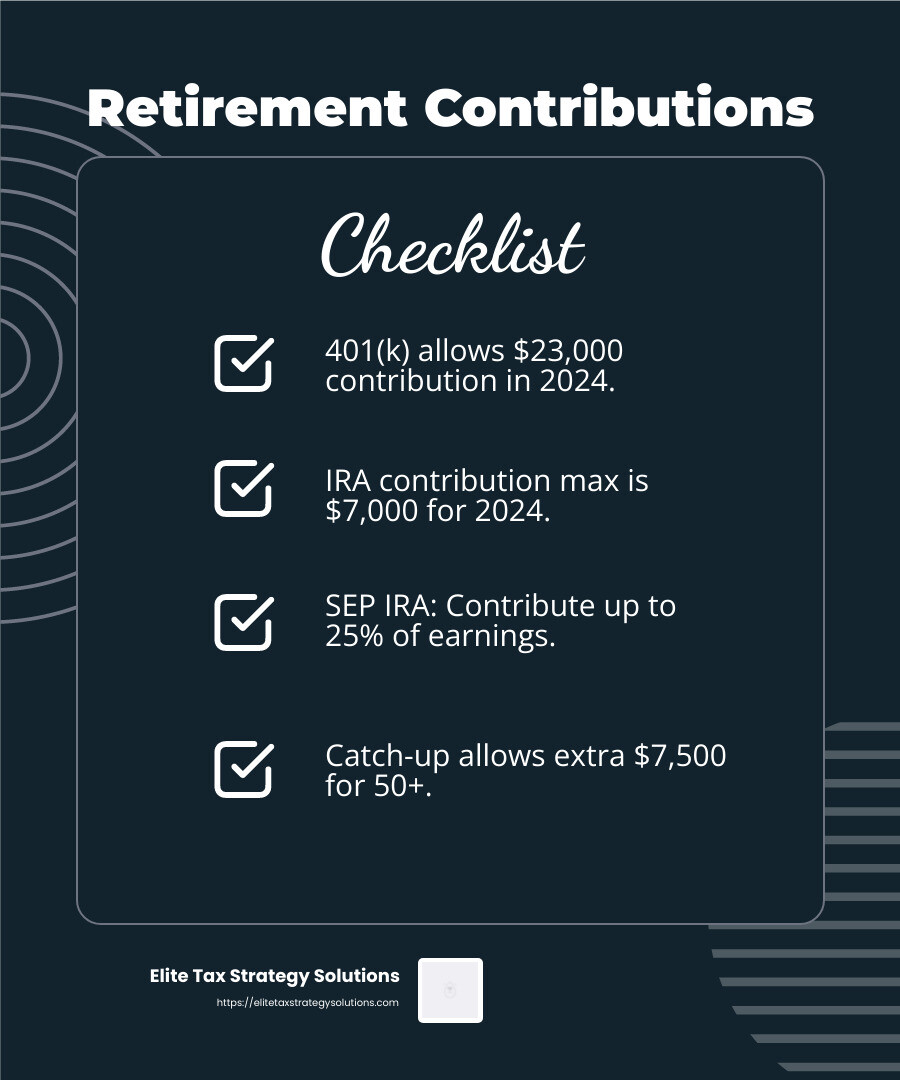

A 401(k) is a popular retirement savings plan offered by many employers. Contributions are made with pre-tax dollars, reducing your taxable income. For 2024, you can contribute up to $23,000, and if you’re 50 or older, you can add an extra $7,500 as a catch-up contribution. This means an employee earning $100,000 can reduce their taxable income to $77,000 by contributing the maximum amount.

Individual Retirement Accounts (IRAs)

IRAs offer another way to save for retirement with tax advantages. You can contribute up to $7,000 in 2024 to a traditional IRA, or $8,000 if you’re 50 or older. Contributions may be tax-deductible depending on your income and whether you or your spouse have a retirement plan at work. The IRS has specific rules about these deductions, so it’s crucial to check your eligibility.

SEP and SIMPLE IRAs

For the self-employed and small business owners, SEP and SIMPLE IRAs provide excellent opportunities to save for retirement while reducing taxable income.

-

SEP IRA: Allows contributions up to 25% of your net earnings, with a maximum limit of $66,000 in 2024. It’s flexible and easy to set up, making it ideal for self-employed individuals or small business owners.

-

SIMPLE IRA: Designed for small businesses, allowing employees to contribute up to $16,500 in 2024, with an additional $3,500 catch-up contribution for those 50 or older. Employers must either match employee contributions or contribute a fixed percentage.

Catch-Up Contributions

If you’re 50 or older, catch-up contributions allow you to contribute more to your retirement accounts, providing a significant tax break. This is especially beneficial if you started saving later in life or want to maximize your retirement savings as you near retirement age.

Remember: Contributing to these retirement accounts not only helps secure your future but also offers immediate tax benefits by lowering your taxable income. This dual advantage makes retirement contributions a cornerstone of any effective tax-saving strategy.

In the next section, we’ll explore how using health accounts like HSAs and FSAs can further improve your tax savings.

Use Health Accounts for Tax Benefits

When it comes to maximizing tax savings, health accounts like Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) offer excellent opportunities. These accounts not only help you manage healthcare expenses but also provide significant tax advantages.

Health Savings Accounts (HSAs)

An HSA is a powerful tool for those enrolled in a high-deductible health plan (HDHP). Contributions to an HSA are tax-deductible, and the funds grow tax-free. Plus, withdrawals for qualified medical expenses are also tax-free.

-

Contribution Limits: For 2024, you can contribute up to $4,150 for an individual or $8,300 for a family. If you’re 55 or older, you can make an additional catch-up contribution of $1,000.

-

Flexibility: Unlike FSAs, HSA funds roll over year to year, so you don’t have to worry about losing your savings if you don’t spend them within the year.

-

Tax Benefits: Contributions can be made up until the tax filing deadline, allowing you to reduce your taxable income for the previous year. For example, you can make your 2024 contributions by April 15, 2025.

Flexible Spending Accounts (FSAs)

FSAs are another option for managing healthcare costs with tax advantages. These accounts allow you to set aside pre-tax dollars to pay for eligible medical expenses.

-

Use-It-or-Lose-It: Generally, FSA funds must be used within the plan year. However, some employers offer a rollover option of up to $640 for 2024 or a grace period of 2½ months to spend the remaining balance.

-

Contribution Limits: The maximum contribution limit for FSAs is set by the IRS annually. Be sure to check with your employer for specific limits and rules.

-

Restrictions: You cannot contribute to both a general-purpose FSA and an HSA. However, a “limited purpose” FSA that covers only dental and vision expenses may be allowed alongside an HSA.

High-Deductible Health Plans (HDHPs)

To qualify for an HSA, you need to be enrolled in a high-deductible health plan. These plans typically have lower premiums but higher out-of-pocket costs, making an HSA a valuable complement to cover unexpected medical expenses.

By strategically using HSAs and FSAs, you can effectively manage your healthcare costs while maximizing tax savings. These accounts not only reduce your taxable income but also provide a smart way to save for future medical expenses.

In the next section, we’ll dive into leveraging tax credits and deductions to further improve your tax savings.

Leverage Tax Credits and Deductions

Tax credits and deductions are like the secret sauce for maximizing tax savings. They directly reduce the amount you owe, making them incredibly valuable. Let’s explore some key opportunities to save big on your taxes.

Child Tax Credit

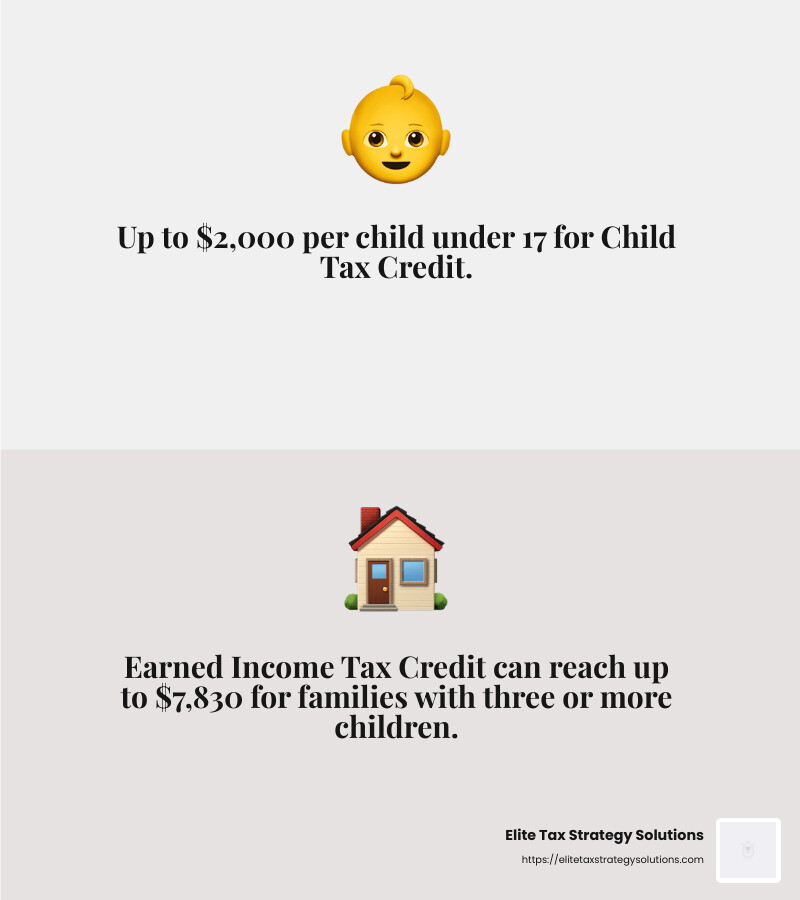

The Child Tax Credit is a significant relief for families. For 2024 and 2025, you can claim up to $2,000 per qualifying child under 17. If you meet the income requirements—under $200,000 for single filers or $400,000 for joint filers—you’ll get the full benefit. Even better, up to $1,700 of the credit is refundable, meaning it could result in a refund even if you owe no taxes.

Earned Income Tax Credit (EITC)

The EITC is a boon for low- to moderate-income workers. Depending on your income and number of children, you might qualify for a credit of up to $7,830 in 2024. The criteria can be complex, but the potential savings are worth it. For instance, a family with three or more children could see a significant boost in their refund.

Charitable Donations

Donating to charity doesn’t just feel good—it can also lower your tax bill. You can deduct donations of cash, goods, or even appreciated assets. For 2024, you might be able to deduct 20% to 60% of your adjusted gross income, depending on the type of donation. Remember to keep receipts and records, as these are essential for claiming deductions.

Pro Tip: Donating appreciated stocks or property can offer double benefits—you get a deduction for the full market value and avoid capital gains taxes.

Strategic Use of Deductions

When it comes to deductions, timing is everything. If you’re close to the threshold for itemizing, consider bunching deductions into one year to exceed the standard deduction. This could include charitable giving, medical expenses, or state taxes.

By leveraging these tax credits and deductions, you can significantly reduce your tax liability and potentially increase your refund. Next, we’ll explore strategic investment moves to further improve your tax savings.

Strategic Investment and Capital Gains Management

Investing wisely isn’t just about growing your wealth—it’s also about maximizing tax savings. Let’s dig into some smart strategies: municipal bonds, long-term capital gains, and tax-loss harvesting.

Municipal Bonds

Municipal bonds, or “munis,” are a great tool for tax-savvy investors. When you invest in these bonds, the interest income is generally exempt from federal taxes, and often state and local taxes if you live where the bond is issued. This makes them an attractive option, especially if you’re in a higher tax bracket.

Quick Fact: Municipal bonds have a lower default rate than corporate bonds. From 1970 to 2022, the default rate was just 0.08% for munis compared to 6.9% for global corporate issuers. This low risk, combined with tax-free interest, can improve your investment returns.

Long-Term Capital Gains

Holding onto investments for more than a year can lead to significant tax advantages. Long-term capital gains are taxed at lower rates than short-term gains, which are taxed as regular income. Depending on your income level, these rates can be as low as 0%, 15%, or 20%.

For example, if you’re a married couple filing jointly with taxable income up to $94,050 in 2024, you might pay no taxes on long-term capital gains. This makes it crucial to understand the timing of your asset sales.

Tax-Loss Harvesting

Even the best investors encounter losses, but these can be turned into a tax advantage through tax-loss harvesting. By selling securities at a loss, you can offset capital gains from other investments. If your losses exceed your gains, up to $3,000 can be deducted from your ordinary income each year, with any excess carried forward to future years.

Important Note: Be aware of the wash-sale rule. If you sell a security at a loss and buy a substantially identical one within 30 days, the loss may be disallowed for tax purposes.

By strategically managing your investments with these tools, you can effectively reduce your tax liability and keep more of your hard-earned money.

Up next, we’ll tackle some frequently asked questions about tax savings strategies.

Frequently Asked Questions about Tax Savings

How can I legally maximize my tax refund?

Maximizing your tax refund can feel like finding hidden treasure. Here are a few ways to do it:

Itemizing vs. Standard Deduction: Choosing between these two can make a big difference. If your deductible expenses exceed the standard deduction, itemizing could lead to a bigger refund. Consider expenses like medical costs, mortgage interest, and state taxes.

Charitable Donations: Giving to charity not only warms the heart but can also boost your refund. If you itemize, you can deduct cash donations up to 60% of your adjusted gross income (AGI). Donating appreciated assets like stocks can be especially beneficial, offering deductions up to 30% of your AGI without triggering capital gains tax.

How can I decrease my taxable income?

Reducing your taxable income is a smart way to keep more money in your pocket. Here’s how:

Retirement Accounts: Contributing to accounts like a 401(k), IRA, or even a SEP or SIMPLE IRA if you’re self-employed, can significantly lower your taxable income. These contributions are often tax-deferred, meaning you pay taxes on withdrawals in retirement when you might be in a lower tax bracket.

Tax Credits: Unlike deductions, which reduce taxable income, tax credits reduce the tax you owe. Popular credits include the Child Tax Credit and the Earned Income Tax Credit. Make sure you qualify and claim them to cut down your tax bill.

How to get a $10,000 tax refund?

Achieving a $10,000 refund might seem daunting, but it’s possible with careful planning:

Overpayment: One way to ensure a large refund is by overpaying your taxes throughout the year. This means adjusting your withholding so more tax is taken out of each paycheck. While this isn’t always the best financial strategy—since you’re essentially giving the government an interest-free loan—it can result in a hefty refund.

Tax Credits: Maximizing tax credits can also help reach that $10,000 mark. Combine credits like the Child Tax Credit with others you qualify for to boost your refund. Credits directly reduce the amount of tax you owe, so they pack a punch.

By understanding these strategies and applying them wisely, you can effectively manage your tax situation and potentially see a bigger refund. Up next, we’ll explore more advanced tax optimization techniques.

Conclusion

At Elite Tax Strategy Solutions, we believe that proactive tax optimization is the key to achieving financial stability and maximizing your tax savings. Our approach is not just about filing returns; it’s about creating a custom strategy that aligns with your financial goals.

We specialize in helping high earners and closely held businesses steer the complexities of tax laws. Our team of seasoned professionals offers over 100 custom tax-saving strategies designed to meet your unique needs. Whether it’s maximizing deductions, leveraging tax credits, or optimizing retirement contributions, we have the expertise to help you keep more of what you earn.

Staying informed and proactive is crucial, especially as tax laws change frequently. Our experts regularly update our strategies to ensure compliance and optimal savings. By integrating tax planning with your broader financial goals, we help you accelerate your progress toward financial success.

If you’re ready to take control of your taxes and improve your financial future, consider partnering with us for comprehensive tax planning. Our Comprehensive Financial Planning services are designed to maximize your tax savings and support your long-term financial stability.

Effective tax planning is not just about minimizing your current tax liabilities—it’s about making strategic decisions that will benefit you for years to come. Let us help you achieve your financial aspirations with confidence and clarity.