Why Smart Small Business Tax Planning Advice Can Save You Thousands

Small business tax planning advice isn’t just about filing returns correctly – it’s about implementing strategic moves year-round that can slash your tax bill by thousands of dollars. The difference between reactive tax preparation and proactive tax planning often determines whether you keep more of your hard-earned profits or hand them over to the IRS.

Quick Answer: Top Small Business Tax Planning Strategies

- Choose the right business structure (LLC, S-Corp, or C-Corp based on income level)

- Maximize deductions – Section 179, bonus depreciation, home office, business meals

- Time income and expenses – defer revenue, accelerate deductible expenses

- Claim all available credits – Work Opportunity Tax Credit, R&D credits, energy credits

- Set up retirement plans – SEP-IRA, Solo 401(k) for immediate tax savings

- Keep detailed records – separate business accounts, digital receipt tracking

- Plan for tax law changes – TCJA provisions expire in 2025

According to recent data, small businesses face an average effective tax rate of 19.8%, but strategic planning can significantly reduce this burden. With bonus depreciation stepping down from 80% in 2023 to 60% in 2024, and the Section 179 deduction limit at $1,220,000 for 2024, timing your equipment purchases becomes crucial.

The key is shifting from a once-a-year mindset to year-round tax strategy. Your tax planning success depends on three core elements: entity optimization, deduction maximization, and strategic timing.

I’m David Fritch, and I’ve spent 40 years helping small business owners steer complex tax strategies through my CPA practice and law firm. My expertise in small business tax planning advice has helped countless entrepreneurs reduce their tax burden while staying fully compliant with IRS regulations.

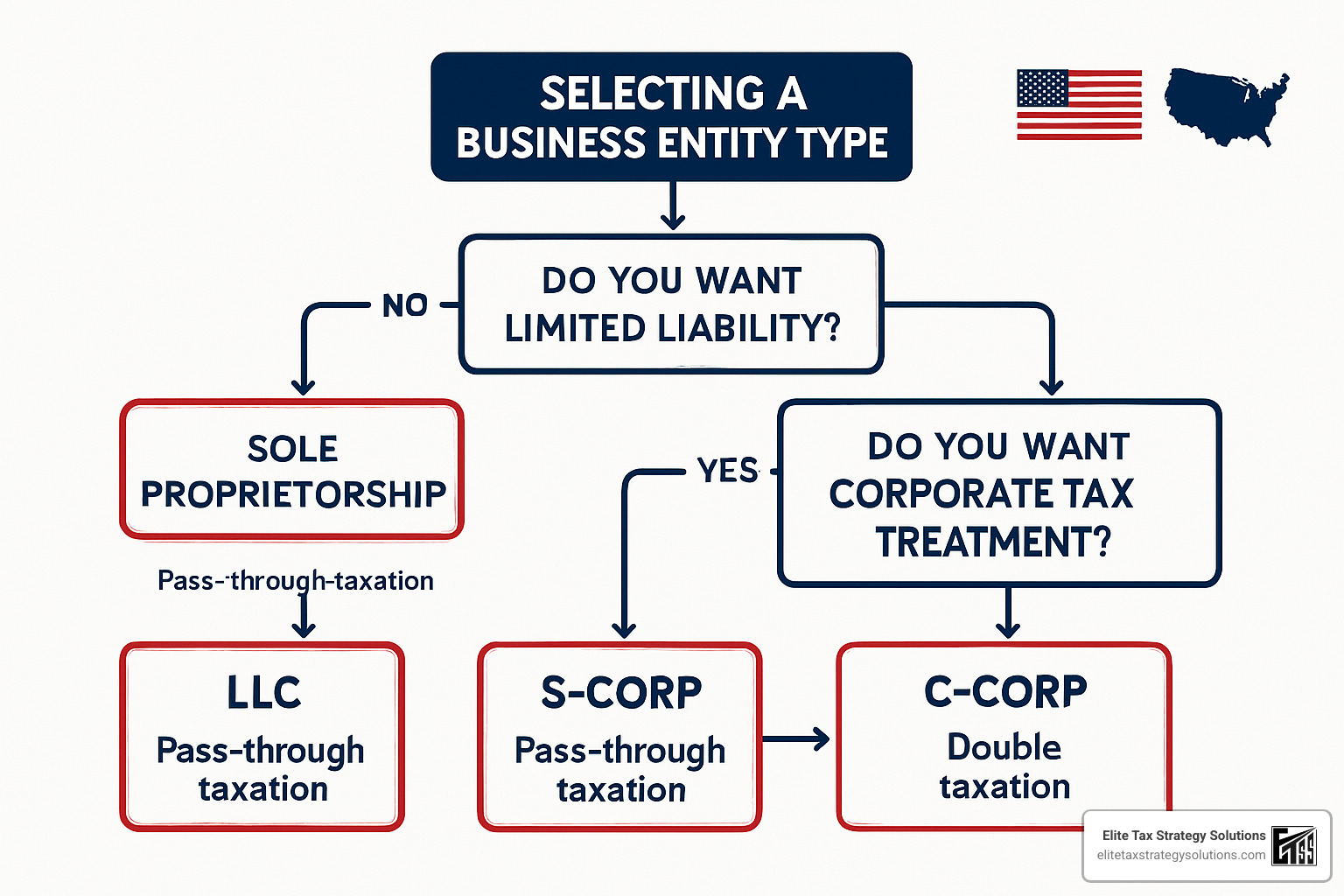

Pick the Right Business Structure First

Your business structure is the foundation of your tax strategy. Get it wrong, and everything else becomes more expensive and complicated. Small business tax planning advice starts with understanding how different structures handle taxes.

Sole proprietorships are simple but costly – every dollar of profit gets hit with 15.3% self-employment tax, and you have zero liability protection.

LLCs give you liability protection with simple pass-through taxation. Your business income flows through to your personal return, avoiding double taxation. You can elect S-Corp status later when it makes sense.

S-Corporations become the sweet spot once you’re consistently profitable. You pay yourself a reasonable salary (subject to payroll taxes), then take additional profits as distributions that avoid self-employment tax. On $100,000 in profit, this structure typically saves around $6,000 annually compared to sole proprietorship.

C-Corporations face double taxation – the company pays 21% corporate tax, then you pay personal taxes on distributions. Unless you’re planning rapid growth and reinvesting most profits, this structure usually costs more for small businesses.

With the Tax Cuts and Jobs Act provisions sunsetting in 2025, including the valuable 20% Qualified Business Income deduction, entity planning becomes even more critical.

Startup or Growing? Small Business Tax Planning Advice On Entity Choice

If you’re still filing Schedule C as a sole proprietor and making decent money, you’re probably leaving cash on the table. The Form 2553 election to become an S-Corporation typically makes sense once you’re consistently earning above $60,000 annually.

Here’s the math: Let’s say your business nets $80,000. As a sole proprietor, you’ll pay $12,240 in self-employment taxes. Elect S-Corp status, pay yourself a $50,000 reasonable salary, and take $30,000 as distributions. You’ll save about $4,590 in self-employment taxes annually.

Conversion timing matters tremendously. You must make the S-Corp election by March 15th of the tax year you want it effective, or within 75 days of forming your LLC.

For comprehensive guidance on optimizing your business structure and maximizing tax savings, explore our Business Tax Planning services.

Employees, Contractors, or Both?

The 1099 versus W-2 decision keeps me busy during audit season. The IRS loses payroll tax revenue when workers get misclassified, so they scrutinize these relationships carefully.

Worker classification comes down to control. Do you tell someone when to work, where to work, and exactly how to do the job? That sounds like an employee. Do they set their own hours, use their own tools, and work for multiple clients? That’s more like a contractor.

Getting worker classification wrong triggers audit triggers that can cost far more than the original payroll taxes. When in doubt, lean toward employee classification.

Essential Deductions & Credits Checklist

The difference between tax preparation and tax planning often comes down to knowing every deduction and credit available to your business. Here are the most impactful write-offs that small business owners frequently overlook.

High-Impact Business Deductions:

- Home Office Deduction – Use actual expenses or simplified method ($5 per square foot, up to 300 sq ft)

- Business Mileage – 67¢ per mile for 2024 (up from 65.5¢ in 2023)

- Section 179 Expensing – Up to $1,220,000 for 2024, phasing out at $3.05 million

- Bonus Depreciation – 60% for property placed in service in 2024

- Health Insurance Premiums – 100% deductible for self-employed individuals

- Business Meals – 50% deductible

- Professional Development – Training, conferences, certifications

- Marketing and Advertising – Including website development and social media promotion

Section 179 vs. Bonus Depreciation Comparison:

| Feature | Section 179 | Bonus Depreciation |

|---|---|---|

| 2024 Limit | $1,220,000 | 60% of cost |

| Phase-out | Begins at $3.05M purchases | No phase-out |

| Best for | Smaller purchases | Large equipment purchases |

The key insight: You can combine Section 179 and bonus depreciation on the same asset to maximize your deduction.

Claim What You Deserve: Small Business Tax Planning Advice for Big Write-Offs

The 20% Qualified Business Income (QBI) deduction represents one of the most significant tax benefits for pass-through entities.

QBI Deduction Thresholds for 2024:

– Single filers: $191,950

– Married filing jointly: $383,900

Below these thresholds, most businesses qualify for the full 20% deduction. Above these amounts, service businesses face restrictions.

Start-up Costs Strategy: New businesses can deduct up to $5,000 in start-up costs in their first year, with the remainder amortized over 15 years.

For comprehensive guidance on maximizing your business deductions, explore our Small Business Tax Planning Strategies resource.

Don’t Miss These Powerful Credits

Tax credits provide dollar-for-dollar reductions in your tax liability, making them more valuable than deductions.

Work Opportunity Tax Credit: Up to $9,600 per eligible employee from targeted groups including veterans, ex-felons, and SNAP recipients.

Small Business Health Care Tax Credit: Available to businesses with fewer than 25 full-time equivalent employees. The credit covers up to 50% of premiums paid for employee health insurance.

Research and Development Credit: Often overlooked by small businesses, this credit applies to expenses for developing new products, processes, or software.

Clean Energy Credits: The Inflation Reduction Act provides nearly $400 billion in clean energy incentives, including credits for electric vehicles and solar installations.

Timing Moves: Defer Income & Accelerate Expenses

Think of tax timing as your financial time machine. The right moves in December can save you thousands when April rolls around. This small business tax planning advice becomes even more valuable as tax laws shift and your business grows.

Most small businesses operate on cash basis accounting, which gives you incredible power over when income and expenses hit your tax return. For cash basis businesses, the game is simple: push income into next year and pull expenses into this year when you want to reduce current year taxes.

Equipment purchases deserve special attention with bonus depreciation stepping down each year. Place that new computer, machinery, or office furniture in service before December 31st to qualify for current year depreciation benefits. With bonus depreciation at 60% for 2024 versus 40% for 2025, timing matters more than ever.

Prepaid expenses work beautifully for cash basis businesses. Pay insurance premiums, rent, or subscription services in advance. The IRS generally allows you to deduct prepaid expenses immediately, as long as the benefit doesn’t extend beyond 12 months.

The safe harbor threshold for estimated payments protects you while implementing these strategies. Pay at least 90% of your current year tax liability or 100% of last year’s tax to prevent underpayment penalties.

Year-End Playbook

December becomes your tactical command center for tax planning. Every day counts, and some moves can only happen before that December 31st deadline.

Mail those checks for deductible business expenses before year-end. The IRS honors the postmark date, not when the recipient cashes the check.

Credit card charges count on the date you make the purchase, not when you pay the credit card bill. Charge business expenses in December even if you won’t pay the credit card company until January.

Equipment timing requires placing assets “in service” before December 31st. Simply purchasing equipment isn’t enough – you must install it and make it available for business use.

Looking Ahead to 2026 Rate Hikes

The tax landscape changes dramatically after 2025 when TCJA provisions expire. Smart business owners are already planning for this “tax cliff.”

Individual tax rates jump from the current top rate of 37% back to 39.6%. The QBI deduction disappears entirely, potentially increasing effective tax rates for pass-through businesses by 4-5 percentage points.

This creates a strategic reversal of typical year-end planning. Instead of deferring income and accelerating deductions, consider accelerating income into 2024-2025 when rates are lower and deferring deductions to 2026 and beyond when they’ll provide more value at higher tax rates.

The key insight: small business tax planning advice must evolve beyond traditional year-end tactics to address these coming changes. Start planning now for the post-2025 tax environment rather than scrambling after the changes take effect.

Recordkeeping, Retirement & Audit Defense: Small Business Tax Planning Advice You Can’t Ignore

Proper recordkeeping is your business’s insurance policy against tax troubles. It’s not just about staying compliant – it’s your strongest defense against IRS audits and the foundation for claiming every deduction you deserve.

Here’s the reality: the burden of proof sits squarely on your shoulders. During an audit, you must prove every single deduction you claimed. The good news is that digital recordkeeping has revolutionized how small businesses manage their financial lives. Cloud-based accounting software connects directly to your bank accounts, automatically importing and categorizing transactions.

Separate business and personal accounts – this single step eliminates 80% of recordkeeping headaches. When everything runs through dedicated business accounts, your bank statements become a clear audit trail.

The IRS requires you to keep general business records for three years from your filing date, but some situations demand longer retention. Employment tax records must be kept for four years, while asset records need to stay until three years after you dispose of the property.

Best-Practice Record Systems

Modern technology makes excellent recordkeeping almost effortless. Bank feeds automatically import your transactions into accounting software, while receipt apps let you snap photos and categorize expenses instantly. Cloud storage keeps everything secure and accessible from anywhere.

For detailed guidance on organizing your business expenses effectively, check out our comprehensive Business Expense Categories resource.

Max Out Retirement & Cut Taxes Simultaneously

Retirement contributions create an immediate win-win: you slash your current tax bill while building long-term wealth. The trick lies in choosing the right plan for your business structure and employee situation.

Solo 401(k) plans work beautifully for business owners without employees. You can contribute up to $69,000 for 2024 ($76,500 if you’re 50 or older) by combining employee deferrals of $23,000 with employer contributions of up to 25% of your compensation.

SEP-IRA plans offer simplicity and flexibility. You can contribute up to 25% of compensation with a maximum of $69,000 for 2024. The catch? If you have employees, you must contribute equally for everyone who’s eligible.

SIMPLE IRA plans work well for businesses with 2-100 employees. Employees can defer up to $16,000 for 2024 ($19,500 if they’re 50+), while employers provide matching or non-elective contributions.

Small employers with 100 or fewer employees can claim a tax credit equal to 50% of plan start-up costs, up to $5,000 annually for three years.

For comprehensive guidance on retirement plan rules and depreciation strategies, reference IRS Publication 946.

Reduce Audit Risk Before Filing

Small businesses actually face lower audit rates than individual taxpayers, but certain red flags can put you on the IRS radar. Unreported 1099 income tops the list because the IRS matches these forms automatically. Excessive home office deductions relative to your income raise eyebrows, especially if you can’t prove exclusive and regular business use.

Your defensive strategy starts with reconciling all 1099 forms with your records before filing. Document the business purpose for every entertainment expense, and maintain detailed logs showing exclusive business use of your home office space.

Small business tax planning advice extends far beyond just filing returns correctly. It’s about building systems that protect your business, maximize your deductions, and give you confidence that everything will stand up to scrutiny if questions arise.

Frequently Asked Questions About Small Business Tax Planning Advice

What are the most lucrative deductions for a home-based business?

Running a business from home opens up fantastic tax-saving opportunities, but you need to play by the IRS rules. Your home office must be used regularly and exclusively for business purposes.

The home office deduction gives you two paths. The simplified method lets you deduct $5 per square foot up to 300 square feet, capping your deduction at $1,500. The actual expense method requires more paperwork but often delivers bigger savings for larger home offices.

With the actual expense method: If your home office takes up 15% of your home’s square footage, you can deduct 15% of your mortgage interest, property taxes, utilities, insurance, repairs, and depreciation. For a $3,000 monthly mortgage and $500 in utilities, that 15% adds up to $6,300 annually.

Don’t overlook additional home-based deductions: dedicated business phone line, office supplies, business equipment, professional liability insurance, and training or conferences that improve your business skills.

When should I hire a fractional CFO or outside tax expert?

The moment you start asking this question, you’re probably ready for professional help. Revenue hitting $500,000 annually usually marks the tipping point where professional small business tax planning advice pays for itself.

Consider professional help when you’re contemplating entity structure changes. Converting from an LLC to S-Corp election or evaluating C-Corp status requires careful analysis. Getting this wrong costs far more than getting it right with expert guidance.

The cost-benefit analysis usually favors professional help once you’re established. A fractional CFO typically runs $3,000 to $10,000 monthly – a fraction of a full-time CFO’s $150,000+ salary.

Look for professionals who provide year-round guidance, not just annual tax preparation. The best advisors reach out proactively about law changes and offer strategic advice that aligns with your business goals.

How do state and local taxes fit into my overall plan?

State and local taxes add complexity but also create opportunities. Pass-through entity (PTE) tax elections represent one of the biggest recent opportunities. Many states now allow LLCs and S-Corporations to pay state income tax at the entity level, creating a federal deduction that sidesteps the $10,000 SALT deduction limitation.

Nexus rules determine where your business owes taxes. Physical presence creates nexus, but so can economic activity thresholds, employee locations, or storage facilities. Sales tax compliance has become increasingly complex since the Supreme Court’s Wayfair decision.

When planning business expansion, consider the total tax burden rather than just federal implications. Some states offer no corporate income tax but higher property taxes. Others provide generous credits for job creation or equipment purchases.

Conclusion & Next Steps

The journey through effective small business tax planning advice doesn’t end with filing your return – it’s just the beginning of a year-round strategy that can transform your business finances. The businesses that nurture their tax strategies throughout the year harvest the biggest savings come April.

You now have the roadmap to potentially save thousands in taxes annually. The difference between business owners who thrive and those who merely survive often comes down to how proactively they approach their tax strategy.

Start with your foundation – reviewing your business structure. If you’re still operating as a sole proprietorship and earning substantial profits, you’re likely leaving money on the table through unnecessary self-employment taxes.

Next, maximize your current opportunities. Section 179 deductions, bonus depreciation, and business expense optimization won’t wait for you. With bonus depreciation stepping down each year and TCJA provisions expiring after 2025, the window for certain strategies is narrowing.

Don’t forget the timing game. Strategic income deferral and expense acceleration can shift your tax burden to more favorable years. This becomes especially powerful as we approach the 2025 tax law changes.

The credits we’ve covered represent free money that too many businesses leave unclaimed. Establishing retirement plans not only secures your future but provides immediate tax relief while building long-term wealth.

At Elite Tax Strategy Solutions, we’ve built our practice around the belief that small business tax planning advice should be proactive, personalized, and profitable. Our comprehensive Business Tax Planning Strategies services focus on year-round optimization because we know that’s where the real savings happen.

The clock is always ticking on tax opportunities. While December 31st marks many deadlines, the most successful business owners start their next year’s planning the moment they file their current return. This continuous approach to tax strategy creates compounding benefits that grow more valuable each year.

Ready to stop leaving money on the table? Our team specializes in turning complex tax strategies into simple, actionable plans custom to your unique business situation. We’ll analyze your current structure, identify missed opportunities, and develop a roadmap for ongoing tax optimization.

The businesses that implement these strategies consistently see the biggest impact. Tax planning isn’t about one big win – it’s about making smart decisions throughout the year that add up to substantial savings. Start with one or two strategies that fit your situation, then build from there.

The best small business tax planning advice is simple: start now, stay consistent, and let your tax strategy work as hard as you do.