Small business tax planning strategies are crucial for owners who want to thrive despite the complexities of modern tax regulations. At the heart of successful tax planning lies the ability to reduce tax liabilities, maximize deductions, and strategically plan for the future. Here are the essentials that small business owners should consider:

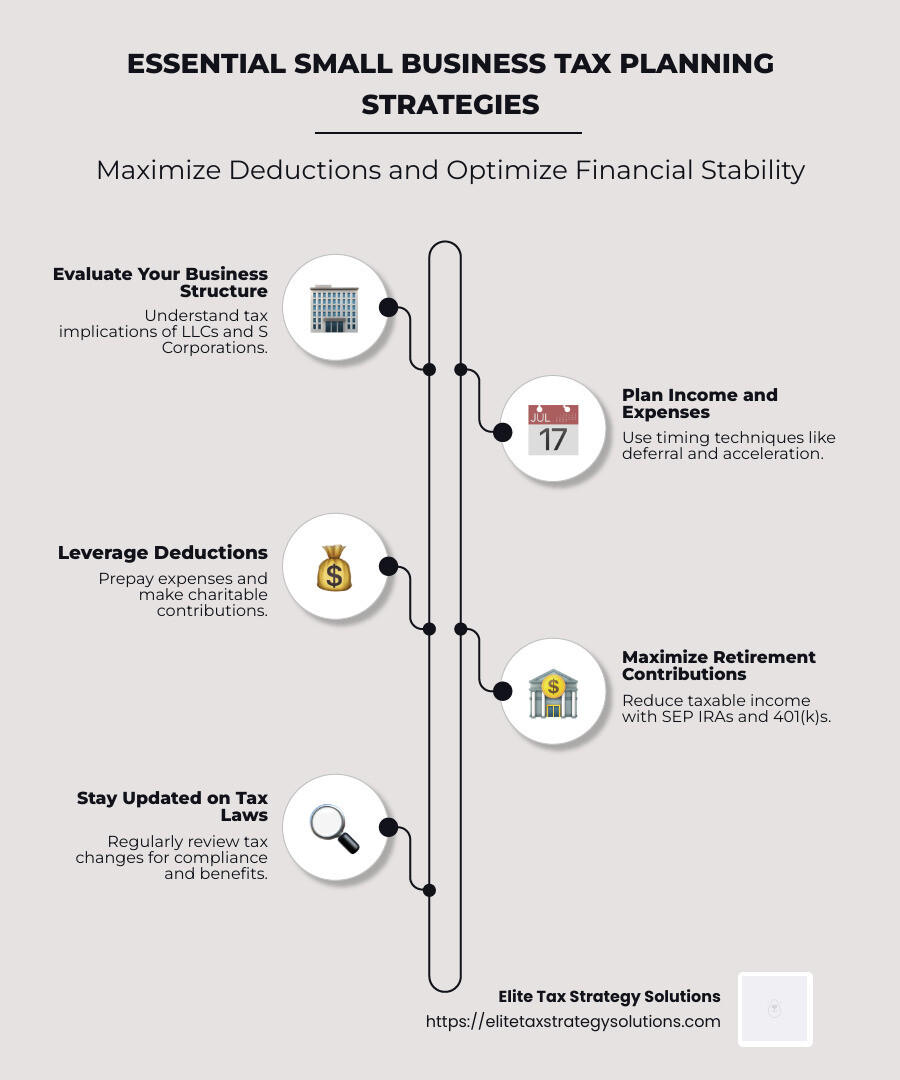

- Evaluate your business structure: Choosing the right structure like an LLC or S Corporation can have significant tax implications.

- Plan your income and expenses: Timing techniques such as income deferral or expense acceleration can optimize your tax burden.

- Leverage available deductions: Prepay certain expenses or make charitable contributions to maximize deductions.

- Maximize retirement contributions: Use plans like SEP IRAs and 401(k)s to reduce taxable income.

- Stay updated on tax laws: Regularly review changes to ensure compliance and opportunity for benefits.

In this guide, we will solve some of the best practices and insights on making smart tax choices, leading to lasting financial stability. By embracing these strategies, small business owners can confidently steer their financial journey through the intricate maze of tax obligations.

As someone who has over 40 years of experience in tax planning for small business owners, I, David Fritch, am dedicated to offering strategies that help high-income earners and entrepreneurs thrive. With expertise in small business tax planning strategies, I aim to make understanding and optimizing your tax position more accessible and achievable.

Relevant articles related to small business tax planning strategies:

– small business tax saving strategies

– business tax management

– business expense categories

Understanding the Basics of Small Business Tax Planning

Navigating the tax landscape as a small business owner can feel overwhelming. But understanding the basics of small business tax planning strategies can make a big difference in how much you owe Uncle Sam. Let’s break it down into three key areas: deductions, credits, and deferral.

Deductions

Think of deductions as your business’s best friend. They reduce your taxable income, which means you pay less in taxes. Common deductions include:

-

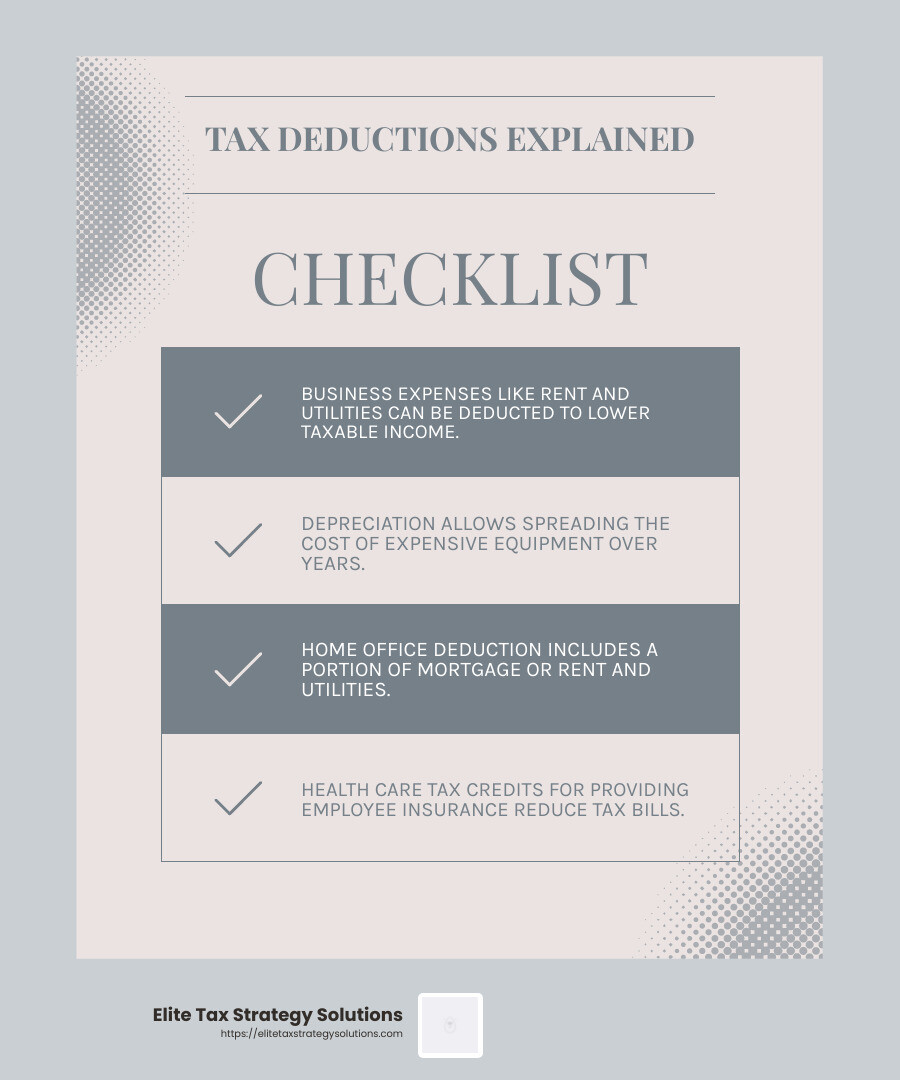

Business Expenses: These are the everyday costs of running your business, like rent, utilities, and office supplies. Deducting these can significantly lower your taxable income.

-

Depreciation: Instead of writing off the cost of expensive equipment all at once, you can spread it out over several years. This is particularly useful for high-cost items like machinery or computers.

-

Home Office Deduction: If you use part of your home exclusively for business, you can deduct a portion of your mortgage or rent, utilities, and even repairs.

Credits

Credits are like a golden ticket—they reduce your tax bill dollar-for-dollar. Here are some you might qualify for:

-

Small Business Health Care Tax Credit: If you provide health insurance to your employees, you might get a credit for part of the cost.

-

Work Opportunity Tax Credit: Hire someone from a targeted group, like a veteran, and you could earn a tax credit.

-

Disabled Access Credit: Make your business more accessible and earn up to $5,000 in credits.

Deferral

Deferring income or expenses can be a smart move. It’s like hitting the pause button on your tax bill:

-

Income Deferral: Delay sending invoices until the next tax year if you expect to be in a lower tax bracket.

-

Expense Acceleration: Pay for next year’s expenses now to take the deduction this year.

These basics form the foundation of effective tax planning. By understanding and utilizing deductions, credits, and deferral strategies, small business owners can steer the tax maze with confidence and keep more of their hard-earned money.

Next, we’ll dive into the top strategies for working closely with your CPA to ensure your business is on the right track.

Top 5 Small Business Tax Planning Strategies

Meet with Your CPA

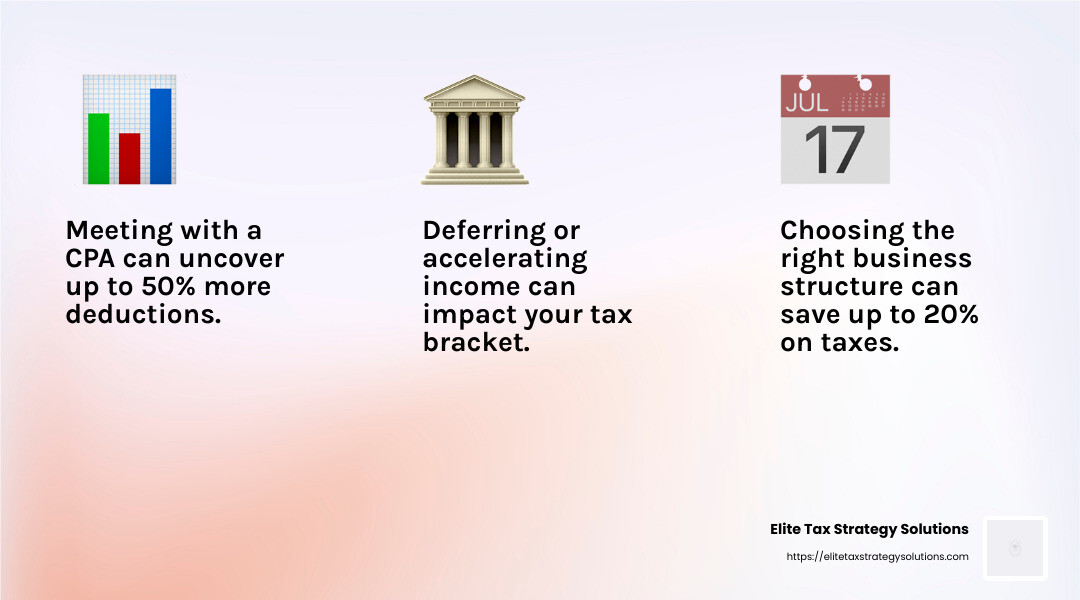

The first step in smart tax planning is to meet with your CPA or tax advisor. This isn’t just about crunching numbers—it’s about gaining insights into your business’s financial health. Your CPA can help you estimate your tax liability, suggest strategies to lower it, and make sure you’re taking advantage of every deduction and credit available.

Think of this meeting as a financial review that sets the stage for the rest of your tax planning. It’s like a roadmap to guide you through the complex tax landscape.

Evaluate Your Business Structure

Your business structure can significantly impact your taxes. Many small businesses start as sole proprietorships because it’s simple. But as your business grows, it might be time to consider other structures like an LLC or an S Corporation.

These structures not only offer liability protection but can also provide tax benefits. For instance, an S Corporation allows income to pass through to shareholders, potentially reducing your overall tax burden. Discuss these options with your CPA to determine the best fit for your business.

Consider Income Deferral or Acceleration

Timing is everything in tax planning. If your business operates on a cash basis, you can defer income by delaying invoices or accelerate income by billing clients sooner, depending on your financial situation.

For instance, if you expect to be in a higher tax bracket next year, it might make sense to accelerate income into this year. However, if you use accrual accounting, you must record income when it’s earned, not when it’s received.

Leverage Last-Minute Deductions

Before the year ends, look for ways to reduce your taxable income through deductions. Consider prepaying expenses like business insurance or rent to take the deduction this year.

Also, consider making charitable contributions. Not only do they benefit your community, but they also provide a tax deduction. Every deduction reduces your taxable income, helping you keep more money in your business.

Maximize Retirement Contributions

Retirement plans are not just for employees. As a business owner, contributing to a SEP IRA or a 401(k) can significantly reduce your taxable income. Plus, it helps you save for the future.

These contributions are tax-deductible, meaning they lower your taxable income. Setting up a retirement plan can also make your business more attractive to potential employees. Check with your tax advisor to see how much you can contribute and which plan is right for you.

By implementing these small business tax planning strategies, you can steer the tax maze with confidence and keep your business financially healthy. Up next, we’ll explore advanced strategies that can further optimize your tax situation.

Advanced Tax Strategies for Small Businesses

When it comes to small business tax planning strategies, thinking ahead can save you a bundle. Let’s dive into some advanced tactics that can make a big difference, especially if you’re looking to invest in equipment or go green.

Equipment Deductions

Buying new equipment? Great! You can take advantage of equipment deductions to reduce your tax bill. Under the current tax law, you can deduct up to $1,220,000 of the cost of qualifying equipment in the year you buy it. This is known as the Section 179 deduction. But remember, this deduction starts to phase out if you spend more than $3.05 million on equipment.

If you’ve already hit the Section 179 limit, don’t worry. You can still benefit from bonus depreciation, which allows you to deduct 60% of the cost of new equipment. This can be a smart move if you expect to be in a higher tax bracket in the coming years. So, if you’re on the fence about buying that new piece of machinery, it might be worth doing it now to maximize your deductions.

Green Energy Credits

Thinking about making your business more eco-friendly? The federal government offers green energy tax credits to encourage businesses to invest in clean energy. The Inflation Reduction Act, signed in 2022, provides nearly $400 billion for clean energy tax credits.

You can earn credits for activities like purchasing electric vehicles, installing solar panels, or other energy-efficient upgrades. These credits reduce your tax bill dollar-for-dollar, making them very valuable. Plus, some states offer additional incentives, so be sure to check with your tax advisor to see what’s available in your area.

These advanced tax strategies can significantly impact your bottom line, helping you save money while investing in your business’s future. By leveraging equipment deductions and green energy credits, you can optimize your tax position and support sustainable growth.

Frequently Asked Questions about Small Business Tax Planning Strategies

Navigating the tax maze can feel overwhelming, but understanding some key concepts can make it much easier. Let’s tackle some frequently asked questions to clarify essential small business tax planning strategies.

What are the 5 pillars of tax planning?

The five pillars of tax planning are all about smart strategies to manage your tax obligations:

-

Deducting: This involves identifying all possible deductions you can take. For small businesses, this might include office expenses, travel, and equipment. The goal is to lower your taxable income as much as possible.

-

Deferring: Sometimes, it’s beneficial to delay income or accelerate expenses to the next year. This can help manage your tax bracket and reduce your immediate tax burden.

-

Dividing: This strategy involves spreading income among family members or across different business entities to take advantage of lower tax rates.

-

Disguising: While it sounds sneaky, this is about legally structuring your income in a way that minimizes taxes. For instance, using a retirement account to shield income from immediate taxation.

-

Dodging: This isn’t about evasion but rather using tax credits to offset your tax liability. Credits are powerful because they reduce your tax bill dollar-for-dollar.

How can LLC owners avoid taxes?

LLC owners have unique opportunities to minimize taxes, primarily by utilizing the pass-through entity structure. This means the business income is reported on the owner’s personal tax return, avoiding the double taxation faced by C corporations.

Another strategic move is electing to be taxed as an S Corporation. By doing so, LLC owners can potentially save on self-employment taxes. In this setup, part of the income can be treated as a distribution, which isn’t subject to self-employment tax, unlike a salary.

What are the three basic strategies to use in planning for taxes?

When planning for taxes, focus on these three basic strategies:

-

Reduce Income: This doesn’t mean earning less but rather using deductions and retirement contributions to lower your taxable income.

-

Increase Deductions: Keep track of all business-related expenses. From office supplies to travel, every deduction helps reduce your taxable income.

-

Tax Credits: Take advantage of available tax credits, such as those for energy efficiency or hiring veterans. These credits directly reduce the amount of tax you owe, making them highly valuable.

Understanding these strategies can make a significant difference in your tax planning efforts. By applying these principles, you can steer the tax maze more effectively and keep more of your hard-earned money.

Conclusion

At Elite Tax Strategy Solutions, we understand that navigating the tax maze can be daunting for small business owners. That’s why our proactive approach to tax optimization is designed to simplify the process and maximize your savings.

Our team of seasoned professionals is dedicated to providing personalized tax planning services that align with your unique financial goals. We don’t just focus on compliance; we aim to improve your financial stability by uncovering opportunities for tax savings.

Whether it’s evaluating your business structure, leveraging last-minute deductions, or maximizing retirement contributions, our custom strategies are crafted to help you make informed decisions. By staying ahead of tax law changes and integrating tax planning with your broader financial strategy, we ensure that you are well-prepared to face any tax challenges.

Our commitment is to help you keep more of what you earn, so you can invest back into your business and secure a prosperous future. If you’re ready to take control of your taxes and optimize your financial situation, we invite you to learn more about our services.

Together, we can turn the complexities of tax planning into a roadmap for success.