Tax compliance for companies is a critical aspect of business management, ensuring they adhere to laws and regulations while avoiding hefty penalties. Maintaining compliance involves understanding and following the constantly changing tax laws, preparing accurate returns, and making timely payments. This is essential to prevent legal repercussions and safeguard a company’s reputation. Compliance failures not only lead to financial penalties but also risk damaging a company’s standing with authorities and the public.

- Importance of Compliance: Protects against legal issues and penalties.

- Legal Consequences: Non-compliance can result in severe fines and possible litigation.

- Staying Informed: Regular updates on tax laws help avoid unexpected liabilities.

- Changing Regulations: Adapt quickly to new laws to ensure ongoing compliance.

As companies face these challenges, adopting proactive strategies for compliance becomes vital. My name is David Fritch, and I have over 40 years of experience in managing tax compliance for companies. I’ve worked with both large firms and small businesses, helping them steer tax laws effectively. My expertise in this field ensures businesses can focus on growth while staying compliant.

Tax compliance for companies word list:

– multi state sales tax compliance

– international tax compliance

– vat compliance services

Understanding Tax Compliance for Companies

Tax compliance is the practice of adhering to tax laws and regulations. For businesses, this means preparing accurate tax returns, paying taxes on time, and keeping up with ever-changing tax laws. It’s not just about avoiding penalties; it’s also about maintaining a good reputation and building trust with the IRS and other tax authorities.

What is Tax Compliance Work in Business?

In the business world, tax compliance work involves several key activities. A tax compliance representative plays a crucial role here. They ensure that companies meet all their tax obligations, help taxpayers understand their responsibilities, and work on collecting delinquent taxes if needed.

Think of tax compliance as a strategic asset. It’s not only about following rules but also about using compliance as a tool to improve financial planning and decision-making. By staying compliant, businesses can avoid legal troubles and focus on growth.

IRS compliance checks are another important aspect. These checks are reviews conducted to ensure that companies are following tax laws correctly. They’re less formal than audits but still require accurate reporting and record-keeping.

Types of Taxes Companies Must Pay

Businesses are subject to various types of taxes, each with its own set of rules:

-

Corporate Income Tax: This tax is levied on a company’s profits. It’s essential for businesses to understand their tax rate and take advantage of any deductions or credits to minimize their liability.

-

Employment Taxes: These include Social Security and Medicare taxes. Companies must withhold these taxes from employees’ wages and pay them to the government.

-

Sales Tax: Businesses collect this tax on goods and services sold and remit it to the government. The rate varies by jurisdiction, so it’s crucial to stay informed about local tax laws.

-

Property Tax: This tax is applied to real estate and personal property owned by the business. It can significantly impact operational costs, especially for companies with substantial property holdings.

-

Excise Tax: Levied on specific goods like alcohol or tobacco, this tax affects pricing and demand. Businesses involved in these industries need to account for excise taxes in their financial planning.

Understanding and managing these taxes is key to maintaining tax compliance for companies. By keeping accurate records and staying informed about tax laws, businesses can ensure they meet all their obligations and avoid costly penalties.

In the next section, we’ll explore how to establish a robust record-keeping system to support tax compliance efforts.

Establishing a Robust Record-Keeping System

Tools and Best Practices for Record-Keeping

Keeping accurate and organized records is essential for any business aiming to maintain tax compliance for companies. Good record-keeping ensures that you can report income and deductions correctly, which is crucial for preparing accurate tax returns.

Why is Record-Keeping Important?

Think of record-keeping as the backbone of your tax compliance strategy. Without proper records, it’s tough to prove your financial transactions, which can lead to errors in tax filings and potential penalties. Accurate records provide a clear picture of your business’s financial health and help you make informed decisions.

Accurate Transaction Records

Your records should include all transactions, such as income, expenses, and deductions. This means keeping track of invoices, receipts, bank statements, and any other documents that show your financial activities. These records are not just for tax purposes—they also help you monitor cash flow and manage budgets effectively.

Digital Tools and Accounting Software

Gone are the days of paper ledgers. Today, digital tools and accounting software make record-keeping easier and more efficient. Platforms like Invoicera offer features like automated invoicing and expense tracking, which can streamline your financial management. By using these tools, you can ensure that your records are not only accurate but also easily accessible.

Regular Audits

Conducting regular internal audits is a best practice that helps identify any discrepancies in your records. These audits allow you to catch and correct errors before they become larger issues. Regular reviews of your financial data ensure that everything is in order for when tax season rolls around.

Documentation Standards

Having clear documentation standards is crucial. This means establishing guidelines on how to store and organize records. Ensure that your team knows what to keep, where to store it, and how long to retain different types of documents. Consistent documentation practices help you stay organized and ready for any compliance checks or audits.

In summary, a robust record-keeping system is vital for maintaining tax compliance for companies. By leveraging digital tools, conducting regular audits, and adhering to solid documentation standards, businesses can confidently manage their tax obligations and focus on their growth.

Next, we’ll dive into the key tax compliance deadlines companies need to know to stay on top of their tax responsibilities.

Key Tax Compliance Deadlines for Companies

When Must Companies Provide Tax Documents?

Navigating tax compliance for companies involves keeping track of several critical deadlines throughout the year. Missing these can lead to penalties, so stay informed.

Annual Tax Return Deadlines

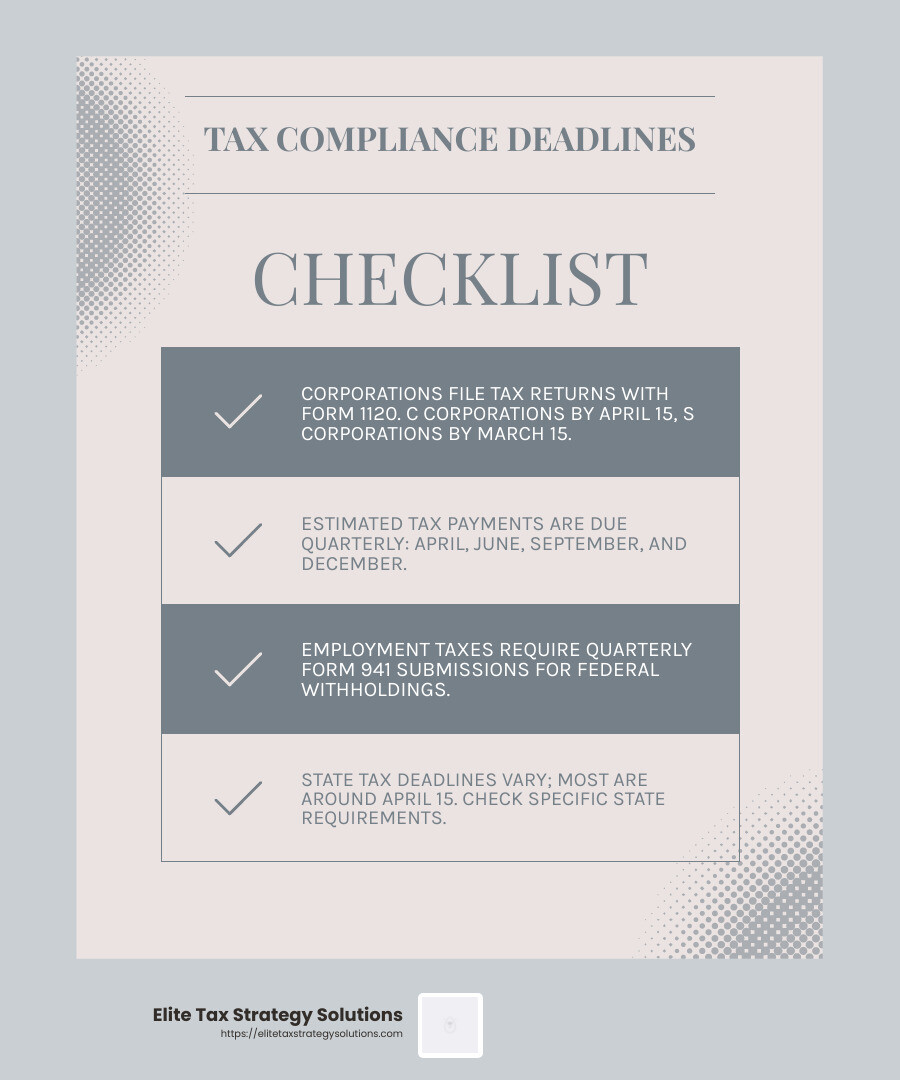

Corporations must file their annual tax returns using Form 1120. For C corporations, this is due by April 15, while S corporations have a deadline of March 15. Companies can request an automatic six-month extension by filing Form 7004. However, it’s crucial to remember that this extension only applies to the filing of the return, not the payment of any taxes owed.

Quarterly Estimated Tax Payments

Most companies must make estimated tax payments four times a year. For calendar-year corporations, these payments are due by the 15th day of April, June, September, and December. It’s important to accurately estimate your tax liability to avoid underpayment penalties.

Employment Tax Deadlines

Companies with employees must adhere to employment tax deadlines, which include withholding federal income, Social Security, and Medicare taxes. Employers must also file Form 941 quarterly to report these withholdings. Ensuring timely payments and filings helps avoid hefty fines and interest charges.

State-Specific Deadlines

Each state has its own tax deadlines, which can vary. Often, state tax returns are due around April 15, but it’s wise to check the specific requirements for each state where your business operates. Missing state deadlines can result in additional penalties and interest.

Forms W-2 and 1099 Series

Companies must provide employees with Form W-2, detailing their total compensation and taxes withheld, by January 31. Similarly, Forms 1099-MISC and 1099-NEC must be sent to independent contractors by the same date. These forms must also be filed with the IRS, typically by January 31, though electronic filings may have slightly extended deadlines.

Staying on top of these deadlines is a key part of maintaining tax compliance for companies. By leveraging digital tools and maintaining a robust record-keeping system, businesses can ensure they meet all their tax obligations on time.

Next, we’ll explore tax compliance strategies custom to different business structures, from sole proprietorships to corporations.

Tax Compliance Strategies for Different Business Structures

Starting and Closing a Business

Starting a Business: Choosing the Right Structure

When starting a business, selecting the appropriate structure is crucial for tax compliance. Each business structure—sole proprietorships, partnerships, LLCs, corporations, and S corporations—has unique tax implications.

-

Sole Proprietorships are the simplest form, where the owner reports business income on their personal tax return. However, they bear the burden of self-employment taxes.

-

Partnerships require filing an information return with the IRS but do not pay income tax themselves. Instead, profits and losses pass through to partners’ personal tax returns.

-

LLCs (Limited Liability Companies) offer flexibility. They can choose how they are taxed, either as a sole proprietorship, partnership, or corporation, depending on their preference.

-

Corporations pay corporate income taxes and must file Form 1120. They face double taxation unless they elect to be an S corporation.

-

S Corporations avoid double taxation by passing income directly to shareholders, who then report it on their personal tax returns. However, they must meet specific IRS requirements to qualify.

Selecting the right structure influences how taxes are calculated and paid. It’s a strategic decision that can impact your tax burden and compliance requirements.

Obtaining an EIN

Once your business structure is determined, obtaining an Employer Identification Number (EIN) is the next step. This unique number is essential for tax filings and is required for opening a business bank account, hiring employees, and applying for business licenses. You can apply for an EIN through the IRS website.

Closing a Business: Final Tax Returns and Reporting

Closing a business involves several tax-related steps. Final tax returns must be filed for the year the business ceases operations. This includes reporting income, expenses, and any capital gains or losses from the sale of business assets.

If the business owns property that is sold or disposed of, this must be reported on the tax return. Any income from these transactions is taxable and should be accurately documented.

Reporting Property Disposal

Disposing of business property requires careful reporting. The gain or loss from the sale or disposal of assets should be included in the final tax return. This ensures compliance and helps avoid future tax issues.

By understanding the tax obligations tied to both starting and closing a business, you can steer these transitions smoothly. The right strategies will ensure you remain compliant with IRS regulations and optimize your tax position.

Next, we’ll dig into how leveraging technology can improve tax compliance for companies.

Leveraging Technology for Tax Compliance

Next-Generation Tax Compliance Tools

As businesses evolve, so do their tax compliance needs. Digitalization has transformed how companies handle taxes, making the process more efficient and accurate. Here’s how technology is reshaping tax compliance:

Automated Tax Filing

Gone are the days of manually filling out forms. Automated tax filing tools streamline the process by collecting and submitting tax data electronically. This not only saves time but also reduces the risk of human error. Many companies are adopting these tools to ensure they meet all filing deadlines accurately.

Data Analytics for Insightful Decisions

Data analytics plays a crucial role in making informed tax decisions. By analyzing financial data, companies can identify trends, spot discrepancies, and optimize tax strategies. This proactive approach helps in minimizing tax liabilities and ensuring compliance.

Real-Time Issue Resolution

Technology enables real-time monitoring of tax processes. If an issue arises, it can be addressed immediately before it escalates. This capability is vital for maintaining compliance and avoiding penalties. Companies can use these tools to track their tax status and resolve any discrepancies quickly.

Emerging Indirect Tax Solutions

Indirect taxes, like sales tax, require precise handling. Emerging solutions are now available to manage these taxes efficiently. For example, some platforms offer real-time tax rate updates, ensuring that companies apply the correct rates in their transactions. This reduces the chance of errors and keeps businesses compliant with ever-changing regulations.

Generative AI for Tax Tasks

Generative AI is revolutionizing how companies approach tax compliance. It can handle complex tasks, answer tax-related questions, and generate reports that would typically require entry-level professionals. By taking over routine tasks, AI frees up tax professionals to focus on strategic planning and analysis.

With tax laws constantly changing, staying updated is crucial. Technology helps businesses monitor changes in tax regulations and adjust their compliance strategies accordingly. Tools that provide alerts and updates on new tax laws ensure that companies remain compliant and avoid penalties.

By leveraging these next-generation tools, companies can transform tax compliance from a daunting task into a streamlined process. This not only improves efficiency but also positions tax compliance as a strategic asset for the business.

In the next section, we’ll explore frequently asked questions about tax compliance for companies, providing clarity on common concerns and misconceptions.

Frequently Asked Questions about Tax Compliance for Companies

What is a Tax Compliance Check?

A tax compliance check is a non-examination review conducted by tax authorities to ensure that companies adhere to tax laws. Unlike audits, these checks are generally simpler and less intrusive. They serve as an accountability tool, helping businesses identify and correct potential issues before they escalate. By participating in these checks, companies can maintain a good standing with tax authorities and avoid costly penalties.

What is the Tax Policy for Businesses in the US?

In the United States, businesses are taxed on an annual basis. Companies can choose a tax year that aligns with their business cycle, which doesn’t necessarily have to be the calendar year. For new corporations, a short tax year can be used for their first tax period. This flexibility allows businesses to align their tax reporting with their operational schedules. However, companies must be mindful of the various deadlines and requirements associated with their chosen tax year to ensure compliance.

How Can Companies Ensure Ongoing Tax Compliance?

Keeping up with changing tax laws is crucial for ongoing compliance. Here are some strategies companies can adopt:

-

Stay Updated on Tax Laws: Regularly monitor changes in tax regulations. This can be done through newsletters, tax authority websites, or professional updates.

-

Regular Training: Conduct training sessions for employees involved in tax processes. This ensures that everyone is aware of the latest compliance requirements.

-

Consulting Tax Professionals: Engage with tax advisors or professionals who can provide expert guidance. They can help steer complex tax scenarios and offer custom advice to meet your business needs.

By implementing these strategies, companies can ensure they remain compliant with tax laws, avoid penalties, and maintain financial stability.

In the next section, we’ll dig deeper into tax compliance strategies for different business structures, helping you understand the unique considerations for each type.

Conclusion

In today’s rapidly changing regulatory environment, proactive tax compliance is not just a necessity—it’s a strategic advantage. Companies that prioritize their tax compliance efforts can avoid costly penalties, protect their reputations, and ensure long-term financial stability.

At Elite Tax Strategy Solutions, we understand the complexities of navigating the tax landscape. Our approach is thorough and proactive, focusing on personalized tax planning for high earners and closely held businesses. By tailoring our strategies to each client’s unique situation, we aim to maximize tax savings and improve financial efficiency.

Our comprehensive services not only help you meet your current tax obligations but also position you for future success. By staying ahead of regulatory changes and leveraging the latest technology, we ensure that your tax strategies are both compliant and optimized for growth.

Financial stability is more than just paying your taxes on time—it’s about making informed decisions that align with your business goals. Our team of experts is dedicated to helping you achieve this by providing ongoing support and guidance.

To learn more about how we can assist you with your tax compliance needs, visit our Tax Support and Compliance page. With Elite Tax Strategy Solutions by your side, you can confidently steer your business towards sustained growth and success.