Small business tax reduction strategies can be the key to achieving financial stability and promoting business growth. For business owners feeling overwhelmed by complex tax regulations and seeking ways to minimize their tax burden, understanding these strategies can provide significant relief.

Here’s a quick overview of effective small business tax reduction strategies:

-

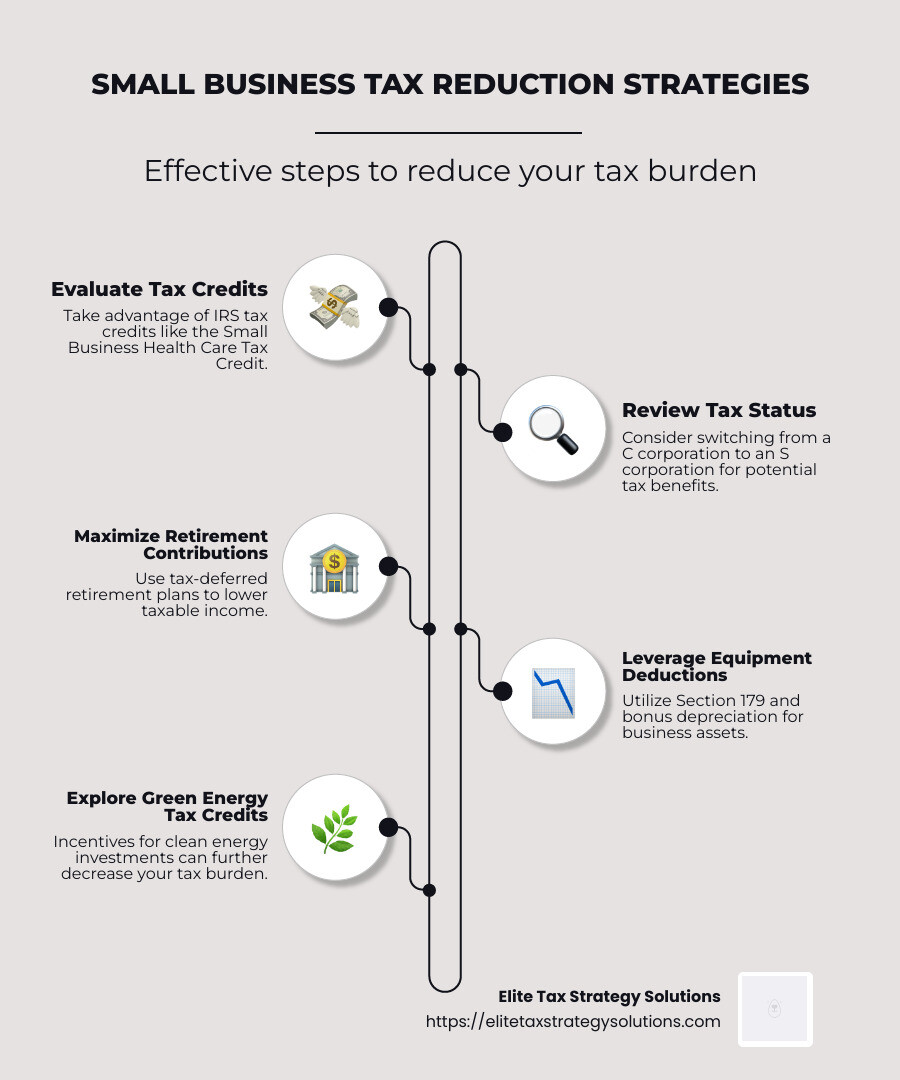

Evaluate Tax Credits: Take advantage of available IRS tax credits such as the Small Business Health Care Tax Credit or Work Opportunity Tax Credit.

-

Review Your Tax Status: Consider whether switching from a C corporation to an S corporation could reduce your liability.

-

Maximize Retirement Contributions: Use tax-deferred retirement plans to lower taxable income.

-

Leverage Equipment Deductions: Use Section 179 and bonus depreciation for business assets.

-

Employ Family Members: This can provide payroll tax savings and future retirement benefits for the children.

-

Explore Green Energy Tax Credits: Incentives for clean energy investments may further decrease your tax burden.

My name is David Fritch, and I bring over 40 years of experience in tax strategy and business management. With Elite Tax Strategy Solutions, I have focused on providing innovative approaches to reduce tax liabilities and support small businesses in achieving long-term financial stability through effective small business tax reduction strategies.

Handy small business tax reduction strategies terms:

– small business tax planning strategies

– tax strategies for small business owners

– tax liability reduction

Understanding Small Business Tax Reduction Strategies

Navigating taxes can feel like wading through a swamp of paperwork and regulations. However, small business tax reduction strategies can make a significant difference in your financial health. Let’s break down the essentials: tax deductions, tax credits, and reducing your adjusted gross income (AGI).

Tax Deductions

Tax deductions are like little gifts from the IRS. They reduce your taxable income, which means you pay less tax. Common deductions include business expenses such as rent, utilities, and office supplies. If you work from home, you might qualify for the home office deduction, which allows you to deduct a portion of your home expenses.

Keep an eye on depreciation, which allows you to spread the cost of property over several years. This is crucial for items like office furniture and computers. Using the Section 179 Deduction, you can deduct up to $1,250,000 of the cost of qualifying business equipment purchased or financed during the year. This is a great way to save on taxes if you’re investing in new tools or machinery.

Tax Credits

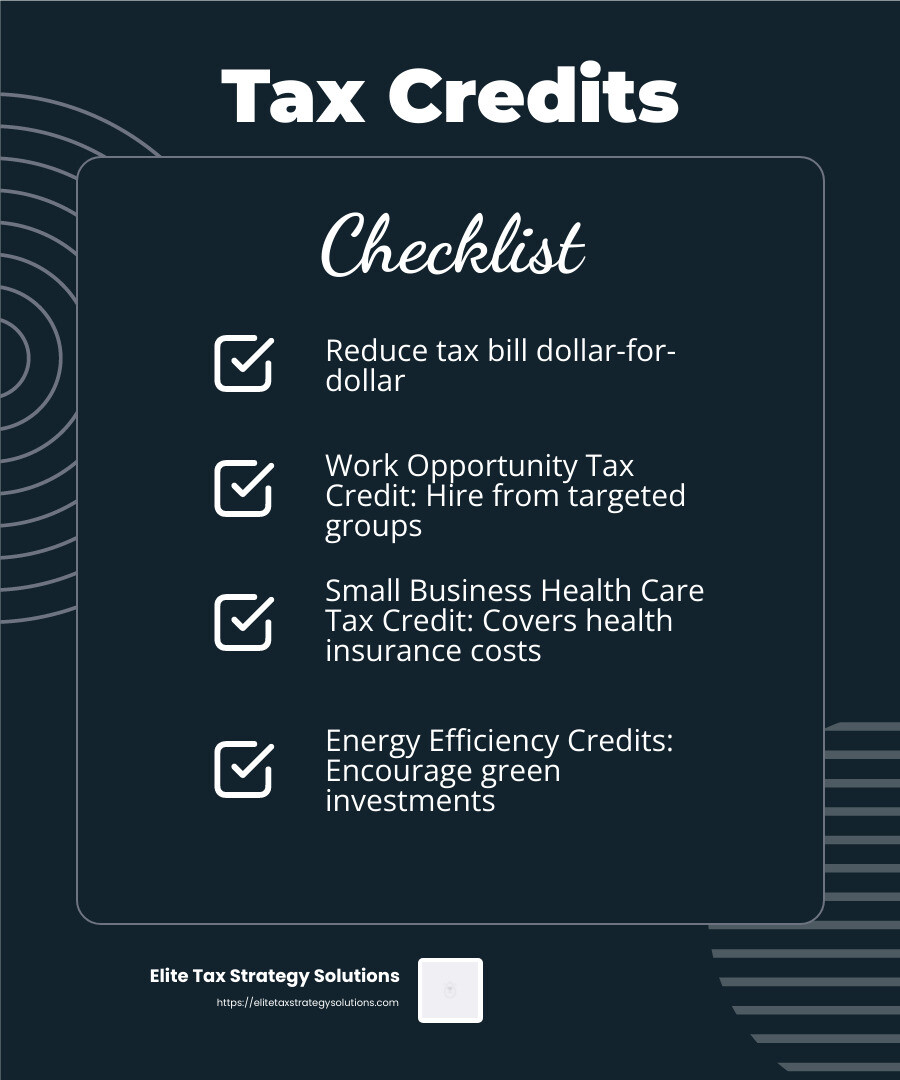

Unlike deductions, tax credits reduce your tax bill dollar-for-dollar. They’re powerful tools for tax reduction. The Work Opportunity Tax Credit, for instance, rewards businesses for hiring individuals from certain targeted groups, like veterans.

Another example is the Small Business Health Care Tax Credit, which helps cover employee health insurance costs. These credits can significantly lower what you owe, so it’s worth exploring which ones apply to your business.

Reducing Your Adjusted Gross Income (AGI)

Your AGI is a key number in the tax world. Many taxes and credits are based on it. Lowering your AGI can keep you from crossing into higher tax brackets or facing additional taxes like the Medicare surtax.

To reduce your AGI, consider contributing to tax-deferred retirement plans or health savings accounts. These contributions lower your taxable income and can provide long-term financial benefits.

Another strategy is to itemize deductions if they exceed the standard deduction. Keep track of these deductions throughout the year to avoid a last-minute scramble.

By understanding these small business tax reduction strategies, you can effectively manage your tax obligations and keep more of your hard-earned money. Next, we’ll dive into the top five strategies that can make an immediate impact on your business’s financial health.

Top 5 Small Business Tax Reduction Strategies

Employ Family Members

Hiring family members can be a smart move for small business owners. When you employ family members, you can legally shift some of your business income to them. This can reduce your overall taxable income, especially if your family members are in lower tax brackets.

For example, if your business is a sole proprietorship, hiring your children can save on payroll taxes. Children under 18 are not subject to FICA taxes, which include Social Security and Medicare. This means neither you nor your child has to pay these taxes, saving you money.

Maximize Retirement Contributions

Contributing to retirement plans is a powerful way to reduce your taxable income. Plans like the SIMPLE IRA, SEP IRA, and 401(k) offer tax-deferred growth. This means you can deduct contributions now and pay taxes on withdrawals during retirement.

Small business owners can also benefit from tax credits for setting up retirement plans. These credits can offset the costs of starting a plan, making it easier to save for the future while reducing your current tax bill.

Use Equipment Deductions

Investing in equipment? The Section 179 Deduction allows you to deduct the full cost of qualifying equipment in the year you purchase it. For 2025, you can deduct up to $1,250,000. This is a great way to lower your taxable income if you’re buying new machinery or tools.

If you exceed the Section 179 limit, consider bonus depreciation. In 2025, you can deduct 40% of the cost of eligible equipment. This phased-down rate still offers significant savings, especially if you’re planning large purchases.

Implement Accountable Plans

Accountable plans are a method for reimbursing employees for business expenses. By doing this, you can deduct these expenses from your business income, while your employees receive reimbursements tax-free. This includes costs like travel, vehicle use, and remote work expenses.

These plans not only provide tax savings but also keep your employees happy by covering their work-related costs. Just ensure the reimbursements are properly documented to meet IRS requirements.

Explore Green Energy Tax Credits

With the Inflation Reduction Act, there are new incentives for investing in clean energy. Businesses can receive tax credits for adopting green technologies, such as installing solar panels or purchasing electric vehicles. These credits can significantly reduce your tax liability.

Check for both federal and state incentives to maximize your savings. Going green not only helps the environment but also boosts your bottom line through tax savings.

By employing these strategies, you can effectively reduce your tax burden and reinvest those savings back into your business.

Advanced Tax Planning Techniques

When it comes to small business tax reduction strategies, advanced planning can make a big difference. Here are some techniques that savvy business owners use:

Defer Income

Deferring income is a strategy where you delay receiving income until the next tax year. This can be especially useful if you expect to be in a lower tax bracket next year. For example, if you operate on a cash basis, you might wait until January to send out invoices for December’s work. This pushes the income into the next year, potentially lowering your current year’s taxable income.

Carryover Deductions

Sometimes, your deductions exceed your income. Instead of losing these deductions, you can carry them over to future tax years. This is known as a carryover deduction. It allows you to offset future income, which can be particularly beneficial if you anticipate higher earnings in the coming years. For example, if you have a net operating loss, you can use it to reduce taxable income in future profitable years.

Business Structure Review

Your business structure can significantly impact your tax situation. For instance, as your business grows, you might benefit from changing your structure. If you’re a sole proprietor, consider forming an LLC or electing to be taxed as an S Corporation. These structures can offer tax advantages, such as reduced self-employment taxes and additional deductions.

Regularly reviewing your business structure ensures you’re taking advantage of the best tax benefits available. Consulting with a tax professional can provide insights into which structure aligns with your business goals and tax strategy.

By implementing these advanced techniques, small businesses can optimize their tax planning and potentially save a significant amount of money. It’s all about being proactive and making informed decisions that align with your financial goals.

Frequently Asked Questions about Small Business Tax Reduction Strategies

How can small businesses pay less taxes?

Small businesses can reduce their tax liabilities by leveraging various deductions and credits. Here are some effective strategies:

-

Health Insurance: If you’re self-employed, you can deduct the cost of your health insurance premiums. This includes medical, dental, and long-term care insurance for yourself, your spouse, and dependents.

-

Retirement Savings: Setting up a retirement plan like a Solo 401(k) or SEP IRA not only secures your future but also provides immediate tax benefits. Contributions to these plans are often tax-deductible, reducing your taxable income.

-

Employee Benefits: Offering benefits such as health insurance and retirement plans to employees can also lead to tax deductions. This not only helps reduce taxes but can improve employee satisfaction and retention.

What is the $5000 tax credit for small businesses?

The $5,000 tax credit is part of the economic relief measures designed to support small businesses. If you start a new retirement plan for your employees, you can deduct up to 50% of the start-up costs, capped at $5,000 per year for the first three years.

To qualify, your business must have fewer than 101 employees, and you should not have had a similar plan in place in the last three years. This credit is a great way to encourage business owners to offer retirement benefits, which can attract and retain talent.

How much should small business owners save for taxes?

Saving for taxes is crucial to avoid surprises. Here are some guidelines:

-

Income Tax: On average, small businesses face an effective tax rate of about 19.8%. However, this can vary based on your business structure and location. It’s wise to set aside a portion of your income throughout the year to cover these taxes.

-

Self-Employment Tax: If you’re self-employed, you must pay self-employment taxes, which cover Social Security and Medicare. This is approximately 15.3% of your net earnings.

-

Estimated Taxes: Small business owners often need to make quarterly estimated tax payments. This helps avoid penalties and a large tax bill at the end of the year. Using accounting software or consulting with a tax professional can help you calculate these payments accurately.

By understanding these elements and planning accordingly, small business owners can manage their tax liabilities effectively and ensure they are not caught off guard when tax season arrives.

Conclusion

Navigating the complex world of taxes can be overwhelming for small business owners, but it doesn’t have to be. At Elite Tax Strategy Solutions, we believe in the power of personalized tax planning to transform your financial landscape. Our proactive approach ensures that your tax strategy is not only compliant but optimized for maximum savings.

We specialize in crafting tax solutions custom to your unique business needs. Whether it’s leveraging deductions, maximizing credits, or exploring advanced strategies like income deferral and business structure review, our team is committed to helping you keep more of your hard-earned money.

Our experts stay updated on the latest tax laws, ensuring your strategy evolves with the changing landscape. This means you can focus on growing your business while we handle the intricacies of tax planning.

For small business owners, understanding and implementing effective tax reduction strategies is crucial. It’s not just about saving money; it’s about achieving financial stability and setting your business up for long-term success.

If you’re ready to take control of your taxes and explore how a proactive, personalized approach can benefit your business, contact us today. Let’s work together to build a tax strategy that aligns with your financial goals and helps your business thrive.