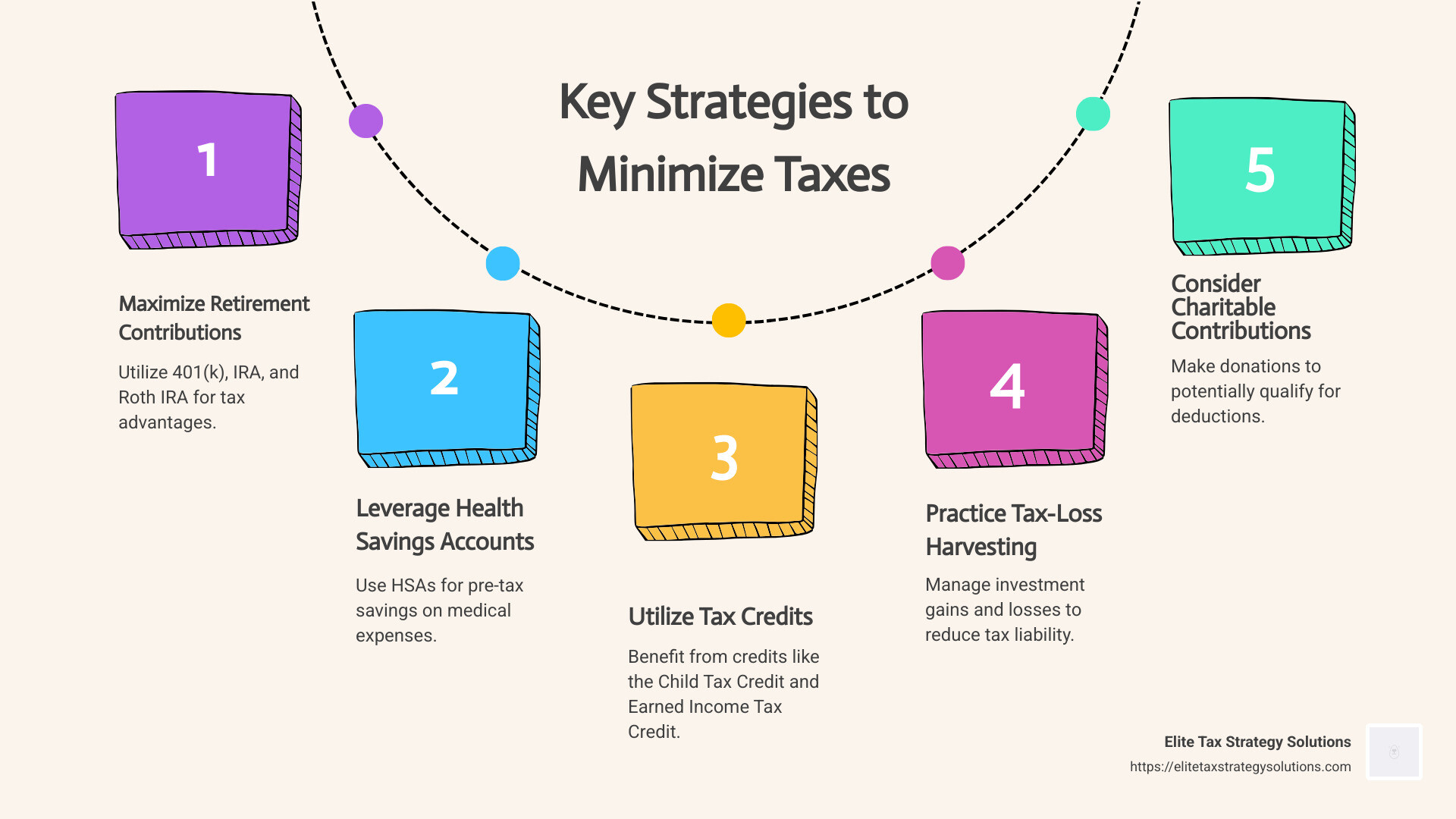

When it comes to how to minimize taxes, strategic tax planning throughout the year is key. Here are some foundational steps to consider immediately:

- Contribute to retirement accounts for possible deductions.

- Take advantage of tax credits like the Child Tax Credit.

- Use Health Savings Accounts (HSAs) if eligible.

- Explore tax-loss harvesting to manage investment gains and losses.

- Consider charitable contributions for potential deductions.

Smart, proactive tax planning is a crucial part of managing your financial health. Instead of waiting for tax season to roll around, actively managing your finances year-round can yield significant benefits in reducing tax liabilities and optimizing financial well-being.

As the founder of Elite Tax Strategy Solutions, I’m David Fritch. With four decades of experience in tax planning, I’ve helped countless individuals and businesses uncover opportunities within the tax code to achieve financial aspirations. Let’s explore how thoughtful tax strategies can lighten your tax load.

How to minimize taxes terms to know:

– proactive tax planning opportunities

– tax planning for high earners

– business tax savings strategies

How to Minimize Taxes

When it comes to minimizing your tax burden, understanding and utilizing tax credits, deductions, and retirement contributions are essential strategies.

Tax Credits

Tax credits are a powerful tool in reducing your tax bill because they offer a dollar-for-dollar reduction in the amount of tax you owe. Unlike deductions, which reduce your taxable income, credits directly decrease your tax liability. Some key tax credits to consider include:

-

Earned Income Tax Credit (EITC): Designed for low to moderate-income workers, this credit can significantly reduce the amount of tax owed.

-

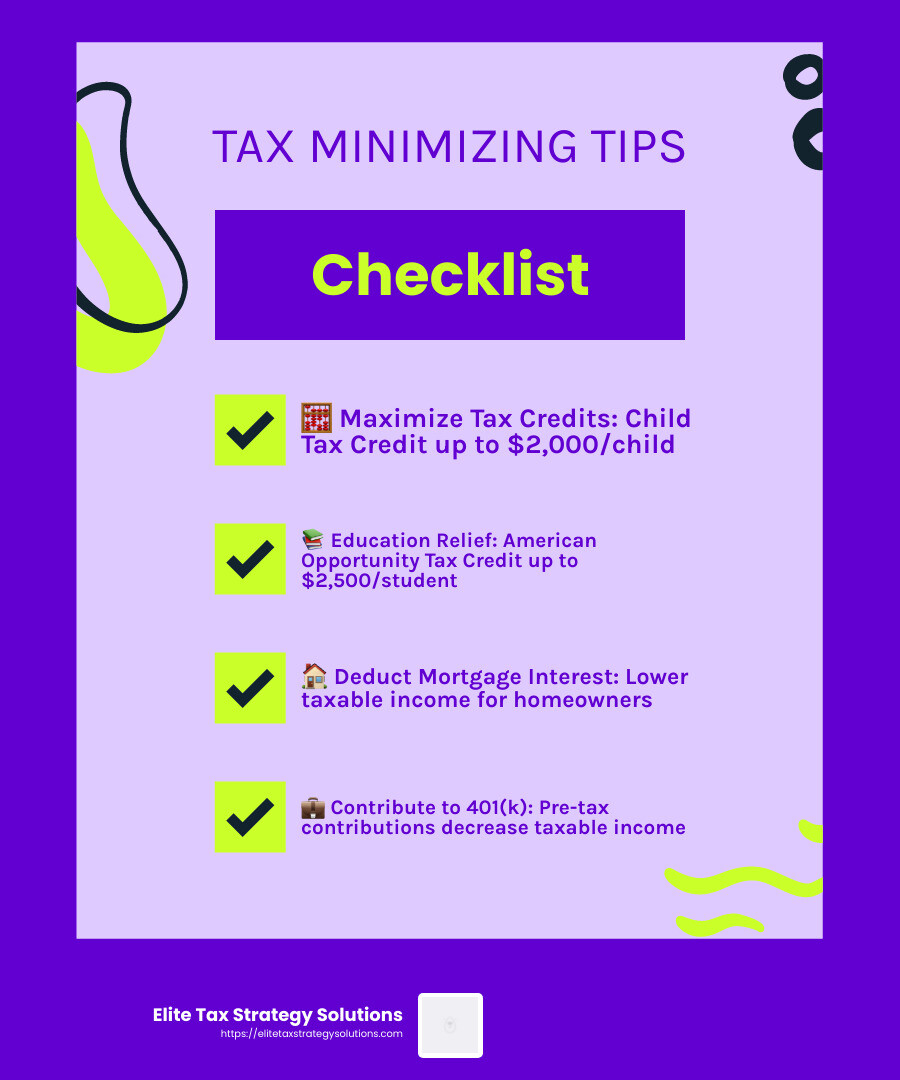

Child Tax Credit: Offers financial relief to families with children, potentially lowering your tax bill by up to $2,000 per child.

-

American Opportunity Tax Credit: Aimed at reducing the cost of higher education, this credit can provide up to $2,500 per eligible student.

Taking full advantage of these credits can make a substantial difference in your tax liability.

Deductions

Deductions are another way to lower your taxable income. Common deductions include:

-

Charitable Contributions: Donations to qualified organizations can be deducted, reducing your taxable income.

-

Medical Expenses: If your medical expenses exceed 7.5% of your adjusted gross income, you may be able to deduct the excess.

-

Mortgage Interest: Homeowners can deduct the interest paid on their mortgage, potentially lowering their taxable income significantly.

These deductions can help you pay less tax by decreasing the amount of income that is subject to taxation.

Retirement Contributions

Contributing to retirement accounts is a smart way to reduce taxable income while securing your financial future. Consider these options:

-

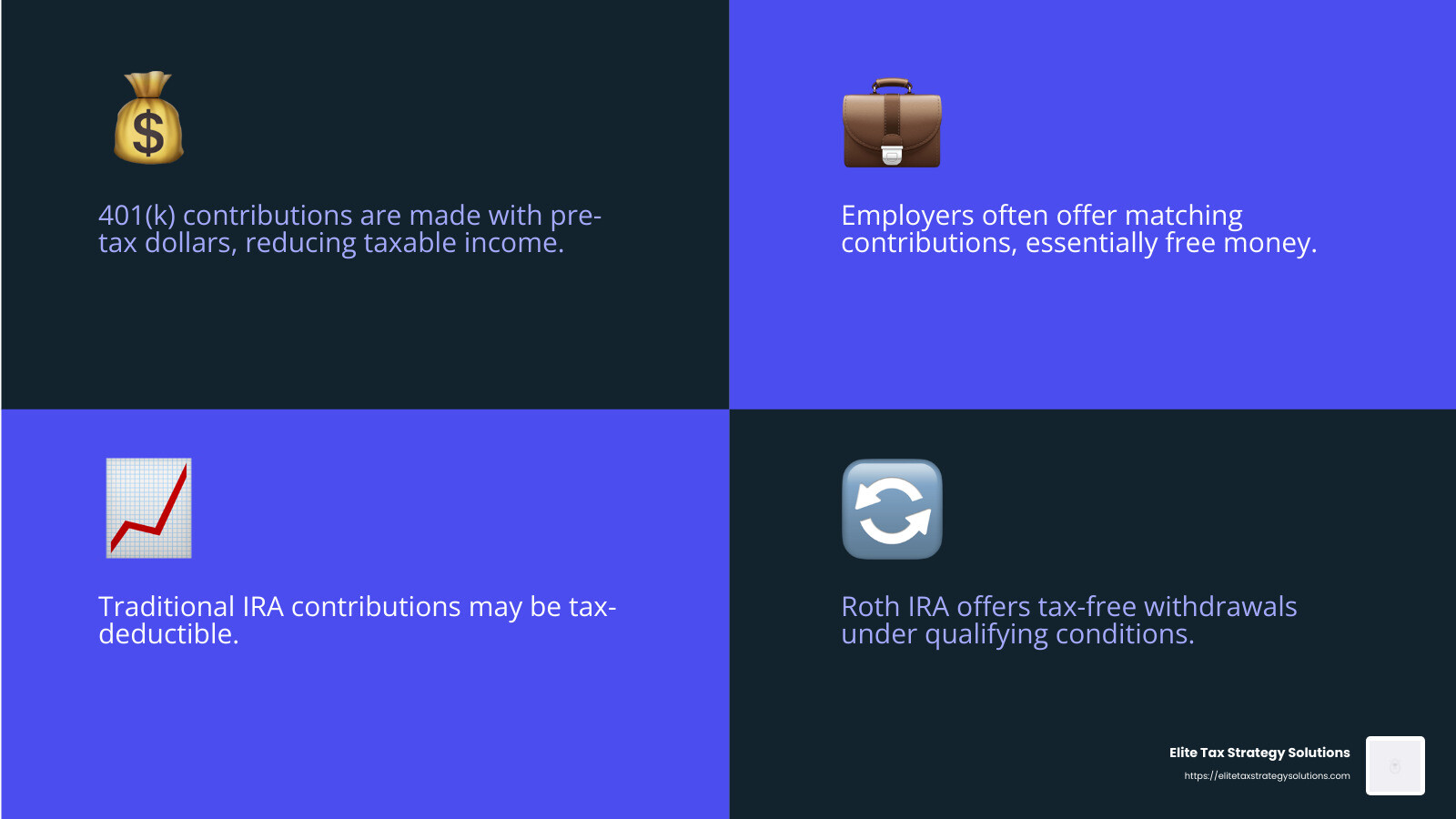

401(k): Contributions are made with pre-tax dollars, which lowers your taxable income. Many employers also offer matching contributions, further boosting your savings.

-

Traditional IRA: Like a 401(k), contributions may be tax-deductible, depending on your income and whether you have access to a retirement plan at work.

-

Roth IRA: While contributions are made with after-tax dollars, qualified withdrawals in retirement are tax-free, providing potential tax savings in the future.

Maximizing contributions to these accounts not only reduces your current tax burden but also helps build a nest egg for retirement.

By leveraging these strategies—tax credits, deductions, and retirement contributions—you can effectively minimize your taxes and improve your financial health. The key is to plan throughout the year and make informed decisions that align with your financial goals.

Maximize Retirement Contributions

When it comes to how to minimize taxes, maximizing your retirement contributions is a powerful strategy. Let’s explore the key retirement accounts you should consider: 401(k), IRA, and Roth IRA.

401(k)

A 401(k) is a retirement savings plan offered by many employers. Contributions are made with pre-tax dollars, which means the money goes into your account before taxes are taken out. This reduces your taxable income for the year, which can significantly lower your tax bill.

-

Contribution Limits: For 2025, you can contribute up to $23,500. If you’re 50 or older, you can make an additional catch-up contribution of $7,500, bringing the total to $31,000.

-

Employer Match: Many employers offer a matching contribution. It’s essentially free money, so make sure to contribute enough to get the full match.

Traditional IRA

A Traditional IRA is another tax-advantaged account that can help reduce your taxable income. Contributions may be tax-deductible, depending on your income and whether you have a retirement plan at work.

-

Contribution Limits: You can contribute up to $7,000 in 2025. If you’re 50 or older, you can add an extra $1,000 as a catch-up contribution.

-

Tax Benefits: The money grows tax-deferred, meaning you won’t pay taxes on it until you withdraw it in retirement. This can be beneficial if you expect to be in a lower tax bracket when you retire.

Roth IRA

Unlike the 401(k) and Traditional IRA, contributions to a Roth IRA are made with after-tax dollars. This means you don’t get a tax break upfront, but the benefits come later.

-

Tax-Free Withdrawals: Qualified withdrawals in retirement are tax-free, which can be a huge advantage if you expect to be in a higher tax bracket in the future.

-

Contribution Limits: The contribution limit for a Roth IRA in 2025 is also $7,000, with a $1,000 catch-up contribution for those 50 and older.

-

Conversion Opportunities: If you have a Traditional IRA or 401(k), consider converting to a Roth IRA during a year when your income is lower. This can be a smart move to minimize taxes over the long term.

By understanding and utilizing these retirement accounts, you can not only reduce your current tax burden but also set yourself up for a financially secure future. These accounts are key tools in the toolbox of anyone looking to minimize their taxes effectively.

Leverage Health Savings Accounts

When exploring how to minimize taxes, Health Savings Accounts (HSAs) are a fantastic tool. They offer triple tax benefits: contributions are pre-tax, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

What is an HSA?

An HSA is a special savings account for people with high-deductible health plans (HDHPs). It’s designed to help you save for medical expenses, but it also provides significant tax advantages.

-

Pre-Tax Contributions: Your contributions to an HSA are made with pre-tax dollars. This means the money is deducted from your paycheck before taxes, lowering your taxable income.

-

Contribution Limits: For 2024, individuals can contribute up to $4,150, and families can contribute up to $8,300. If you’re 55 or older, you can add an extra $1,000 as a catch-up contribution.

Tax Benefits of HSAs

-

Immediate Tax Savings: By contributing to an HSA, you reduce your taxable income for the year. This can lower your federal income tax and, in some cases, state income tax.

-

Tax-Free Growth: The money in your HSA grows tax-free. You can invest your HSA funds in stocks, bonds, or mutual funds, potentially increasing your savings significantly over time.

-

Tax-Free Withdrawals: When you use HSA funds for qualified medical expenses, the withdrawals are tax-free. This includes expenses like doctor’s visits, prescriptions, and even some over-the-counter medications.

How to Maximize Your HSA

-

Max Out Contributions: Aim to contribute the maximum allowed each year to take full advantage of the tax benefits.

-

Invest Wisely: If your HSA allows, consider investing the funds to grow your savings over time. This can be especially beneficial if you don’t need to use the money immediately for medical expenses.

-

Save Receipts: Keep records of your medical expenses. You can reimburse yourself from your HSA years later, allowing your money to grow tax-free in the meantime.

By leveraging an HSA, you not only save on taxes now but also build a financial cushion for future medical expenses. It’s a smart move for anyone with a high-deductible health plan looking to minimize their taxes effectively.

Use Tax Credits

Tax credits are a powerful way to reduce your tax bill because they offer a dollar-for-dollar reduction in the taxes you owe. Unlike deductions, which only reduce your taxable income, credits directly decrease the amount of tax you pay. Let’s explore three valuable tax credits: the Earned Income Tax Credit, Child Tax Credit, and American Opportunity Tax Credit.

Earned Income Tax Credit (EITC)

The EITC is designed to help low-to-moderate-income workers by reducing the amount of tax owed. It’s especially beneficial for families with children, but even those without children can qualify.

-

Eligibility: To qualify, you must have earned income from employment or self-employment. The amount of the credit depends on your income, filing status, and number of qualifying children.

-

Benefits: The EITC can significantly boost your refund or reduce your taxes owed, sometimes resulting in a refund even if no tax is owed.

-

Example: Suppose a single parent with two children earned $25,000 in a year. They might receive a credit of several thousand dollars, drastically lowering their tax bill.

Child Tax Credit

The Child Tax Credit provides financial relief to families with dependent children under the age of 17. This credit can be partially refundable, meaning it can increase your refund even if you don’t owe taxes.

-

Amount: For 2024, eligible families can receive up to $2,000 per qualifying child.

-

Phase-Out: The credit begins to phase out at higher income levels, so it’s important to check if your income qualifies.

-

Additional Benefits: If the credit exceeds your tax liability, you might qualify for the Additional Child Tax Credit, which can provide a refund.

American Opportunity Tax Credit (AOTC)

The AOTC is aimed at helping students and families pay for higher education expenses, like tuition and course materials, during the first four years of college.

-

Eligibility: Students must be enrolled at least half-time in a program leading to a degree or certificate. The credit is available for up to four years of post-secondary education.

-

Amount: The AOTC offers a maximum annual credit of $2,500 per eligible student. If the credit brings your tax liability to zero, 40% of the remaining amount (up to $1,000) can be refunded.

-

Example: A student paying $4,000 in tuition and fees could potentially receive a $2,500 credit, significantly offsetting education costs.

By understanding and utilizing these tax credits, you can effectively reduce your tax burden and keep more money in your pocket. Whether you’re a working individual, a parent, or a student, these credits offer valuable opportunities to minimize taxes and maximize financial benefits.

Optimize Investment Strategies

Investing wisely can be a game-changer when it comes to how to minimize taxes. By understanding and using strategies like municipal bonds, long-term capital gains, and tax-loss harvesting, you can keep more of your hard-earned money.

Municipal Bonds

Municipal bonds, or “munis,” are a great investment for those looking to reduce their tax burden. When you invest in these bonds, you’re essentially lending money to state or local governments. The best part? The interest income from most municipal bonds is tax-free at the federal level, and sometimes even at the state and local levels if you live where the bond is issued.

-

Why Invest? Besides the tax benefits, municipal bonds have lower default rates compared to corporate bonds. From 1970 to 2022, the default rate was just 0.08% for municipal bonds, while global corporate issuers had a 6.9% default rate.

-

Tax Equivalent Yield: If you’re in a high tax bracket, the tax-equivalent yield of municipal bonds can make them even more attractive.

Long-Term Capital Gains

Holding onto your investments for more than a year can pay off, thanks to the preferential tax rates on long-term capital gains. These rates are lower than ordinary income tax rates, making them a smart choice for tax-savvy investors.

-

Tax Rates: Depending on your income, long-term capital gains are taxed at 0%, 15%, or 20%. For instance, in 2024, married couples filing jointly with taxable income up to $94,050 fall into the 0% bracket.

-

Strategy: By planning your investments with these tax rates in mind, you can grow your wealth while keeping taxes low.

Tax-Loss Harvesting

Sometimes, investments don’t go as planned, but there’s a silver lining: tax-loss harvesting. This strategy lets you sell investments at a loss to offset taxes on capital gains from other investments.

-

How It Works: If your capital losses exceed your capital gains, you can deduct up to $3,000 from other income. Losses over this amount can be carried forward to future tax years.

-

Caution: Be mindful of the “wash sale” rule. If you buy back the same stock within 30 days, you can’t claim the loss for tax purposes.

By optimizing your investment strategies, you can effectively minimize taxes and boost your after-tax returns. Whether it’s through tax-free municipal bonds, favorable long-term capital gains rates, or strategic tax-loss harvesting, these approaches ensure that more of your money stays with you.

Charitable Contributions and Deductions

Giving to charity not only feels good, but it can also be a smart move for how to minimize taxes. Let’s explore how qualified charitable distributions and itemized deductions can benefit you.

Qualified Charitable Distributions (QCDs)

For those aged 70½ or older, Qualified Charitable Distributions (QCDs) offer a tax-savvy way to donate. You can transfer up to $100,000 directly from your IRA to a qualified charity. This amount counts toward your required minimum distribution (RMD) but isn’t included in your taxable income.

-

Why Choose QCDs? By lowering your taxable income, QCDs can help reduce your tax bill and potentially keep you in a lower tax bracket.

-

Example: Imagine you have a $10,000 RMD. By donating this amount through a QCD, you avoid paying taxes on it, saving you hundreds or even thousands of dollars.

Itemized Deductions

When it comes to tax deductions, you have two choices: take the standard deduction or itemize your deductions. Itemizing can be worthwhile if your deductible expenses exceed the standard deduction amount.

-

Charitable Contributions: Donations to qualified charities can be deducted if you itemize. For cash donations, you can deduct up to 60% of your adjusted gross income (AGI).

-

Proof Required: The IRS requires documentation for all charitable contributions. For donations over $250, a written acknowledgment from the charity is necessary.

-

Strategy: Consider “bunching” your donations. By making several years’ worth of donations in a single year, you might exceed the standard deduction and maximize your tax benefits.

A Real-Life Example

Let’s say you donate $5,000 each year to various charities. If your itemized deductions don’t exceed the standard deduction, you might not benefit from these donations. However, by bunching two years of donations into one, you could itemize in that year and potentially save on taxes.

By understanding and leveraging qualified charitable distributions and itemized deductions, you can make your charitable giving work harder for you at tax time. Whether you’re planning to donate cash, stocks, or use your IRA, these strategies can help you minimize your taxes while supporting causes you care about.

Frequently Asked Questions about Minimizing Taxes

How can I lower my taxable income?

Lowering your taxable income can be achieved through several strategies, and it starts with tax deductions and retirement accounts. Deductions reduce the amount of your income that is subject to tax. For example, contributing to a traditional IRA or a 401(k) plan can lower your taxable income because these contributions are made with pre-tax dollars.

Consider this: If you contribute $5,000 to your traditional IRA, your taxable income decreases by that amount, potentially saving you hundreds of dollars in taxes depending on your tax bracket.

How do tax credits work?

Tax credits are a powerful tool for reducing your tax bill because they offer a dollar-for-dollar reduction of your tax liability. Unlike deductions, which reduce your taxable income, credits directly reduce the amount of tax you owe. Some popular tax credits include the Earned Income Tax Credit, Child Tax Credit, and American Opportunity Tax Credit.

For instance, if you owe $3,000 in taxes and qualify for a $1,000 tax credit, your tax bill drops to $2,000. This is why tax credits can be more beneficial than deductions for minimizing your taxes.

What are the benefits of municipal bonds?

Investing in municipal bonds is another smart way to manage your taxes. The interest income from these bonds is typically tax-free at the federal level, and sometimes at the state and local levels if you reside in the issuing state. This makes them an attractive option for those in higher tax brackets.

Moreover, municipal bonds are known for their low default rates. According to a report, the default rate for municipal bonds was only 0.08% from 1970 to 2022, making them a safer investment compared to corporate bonds.

By leveraging these FAQs, you can gain a clearer understanding of how to minimize taxes effectively through strategic financial planning. Whether it’s through deductions, credits, or investments, each method offers unique benefits to help reduce your tax burden.

Conclusion

At Elite Tax Strategy Solutions, we understand that navigating the complexities of tax planning can be overwhelming. That’s why we offer personalized tax planning services custom to meet the unique needs of high earners and closely held businesses. Our proactive approach focuses on maximizing tax savings while ensuring financial stability.

Tax planning is not just about filing returns; it’s about strategically optimizing your financial situation. With over 100 custom tax-saving strategies, we help you uncover opportunities to minimize your tax liabilities and improve your financial well-being. Our expert team stays informed about the latest tax laws and regulations, ensuring that your tax plan is always up-to-date and aligned with your long-term financial goals.

Whether you are contributing to retirement accounts, leveraging health savings accounts, or investing in municipal bonds, our goal is to help you keep more of your hard-earned money. We believe that effective tax planning should be integrated into your overall financial strategy, accelerating your progress towards financial success.

If you’re ready to take control of your taxes and achieve financial stability, reach out to us today. With locations in Jasper, Indiana, and suburban areas near major cities, we’re here to provide the guidance and expertise you need.

Explore our Innovative Tax Planning services and find how we can help you optimize your tax position and work towards your financial aspirations.