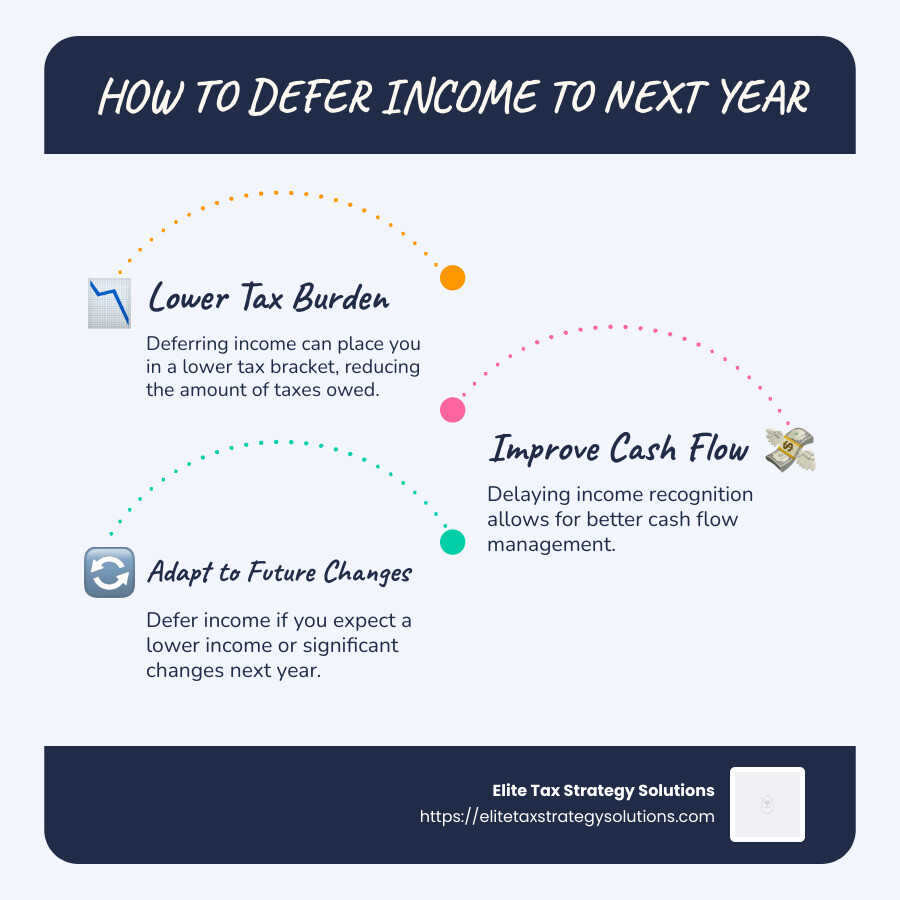

How to defer income to next year is a tactical approach to managing tax obligations for individuals and businesses, supporting healthier financial management. By strategically postponing income to the following year, you can:

- Lower your current tax burden: By deferring income, you might find yourself in a lower tax bracket for the current year, which can result in paying less tax.

- Improve cash flow: Delaying income recognition allows for better cash flow management, providing flexibility in financial planning.

- Take advantage of changing financial circumstances: If you expect a lower income or a significant change in your financial situation next year, deferring income can be a wise move.

Navigating through the complexities of tax planning is crucial for anyone looking to maintain and improve their financial health. As the fiscal year comes to a close, employing smart strategies to shift income into the next year can significantly impact your tax outcomes and overall financial strategy.

I’m David Fritch, and I’ve spent over 40 years helping high-income earners and small business owners optimize their financial strategies. With experience in both law and accounting, I specialize in innovative tax planning approaches, including how to defer income to next year, to improve your financial well-being.

Handy how to defer income to next year terms:

– how to defer taxes

– proactive tax strategies

– tax optimization strategies

Understanding Income Deferral

Understanding income deferral is key to effective tax planning. It involves managing your cash flow, reducing tax liability, and possibly moving into a lower tax bracket. Let’s break it down.

Cash Flow Management

Cash flow is all about the money moving in and out of your business or personal finances. A positive cash flow means you have more money coming in than going out. Managing this flow effectively can give you more control over your finances.

By deferring income to the next year, you can keep more cash on hand now. This helps you cover expenses or invest in opportunities without worrying about immediate tax payments.

Reducing Tax Liability

When you defer income, you might lower your tax liability for the current year. This means you pay less in taxes now, keeping more money in your pocket.

For example, if you’re close to the next higher tax bracket, deferring some income could keep you in the lower bracket, reducing your overall tax rate.

Lower Tax Bracket

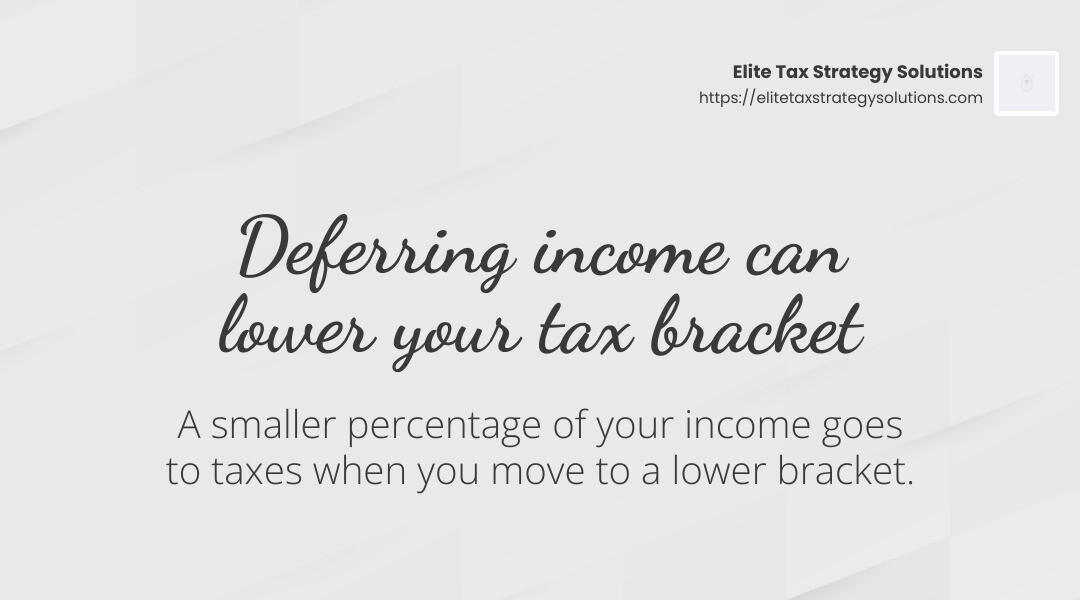

Deferring income can sometimes move you into a lower tax bracket. This is beneficial if you expect to have less income next year due to retirement, business changes, or other reasons.

Being in a lower bracket means a smaller percentage of your income goes to taxes. This strategy can be particularly useful if you’re planning for big life changes that will affect your income.

Understanding these concepts is essential for anyone looking to optimize their tax situation. As you plan for the end of the fiscal year, consider how income deferral might fit into your broader financial strategy.

How to Defer Income to Next Year

Deferring income to the next year can be a smart move for managing your taxes. Let’s explore some simple strategies to defer income to next year effectively.

Postpone Invoicing

If you’re a small business owner using cash-method accounting, you have the flexibility to defer income by postponing invoicing. Here’s how it works:

-

Delay Sending Invoices: If you delay sending invoices until late December, you may not receive payment until the new year. This means that income won’t show up on this year’s tax return.

-

Consider Customer Relationships: Always weigh the risk of delaying invoices. Ensure that postponing won’t affect your ability to collect payments. It’s crucial to maintain good relationships with your customers.

This strategy can be particularly useful if you expect to be in a lower tax bracket next year.

Delay Compensation

For employees, deferring salary or bonuses is another way to manage when income is taxed:

-

Negotiate with Your Employer: If possible, ask your employer to delay your year-end bonus or part of your salary until the next year. This is especially beneficial if you anticipate a lower tax rate next year.

-

Plan for Retirement: If you’re nearing retirement, delaying compensation can help you manage your income levels and tax brackets effectively.

This approach is more common in businesses where employees have flexibility in their compensation packages.

Installment Payments

If you’re selling property or a business, consider structuring the sale with installment payments:

-

Spread the Income: By receiving payments over several years, you spread out the income, potentially keeping you in a lower tax bracket each year.

-

Manage Capital Gains: This can also help manage capital gains taxes, allowing you to pay them gradually rather than in one large sum.

Installment payments offer a way to manage large income events that could otherwise push you into a higher tax bracket.

By using these strategies, you can effectively defer income, manage your cash flow, and potentially reduce your overall tax liability. It’s a step towards smarter financial planning and maximizing your resources.

Strategies for Deferring Income

Deferring income is a smart way to manage your taxes and keep more money in your pocket. Here are some effective strategies to help you defer income to next year.

Retirement Contributions

Contributing to retirement accounts like 401(k)s and IRAs is a classic way to defer income:

-

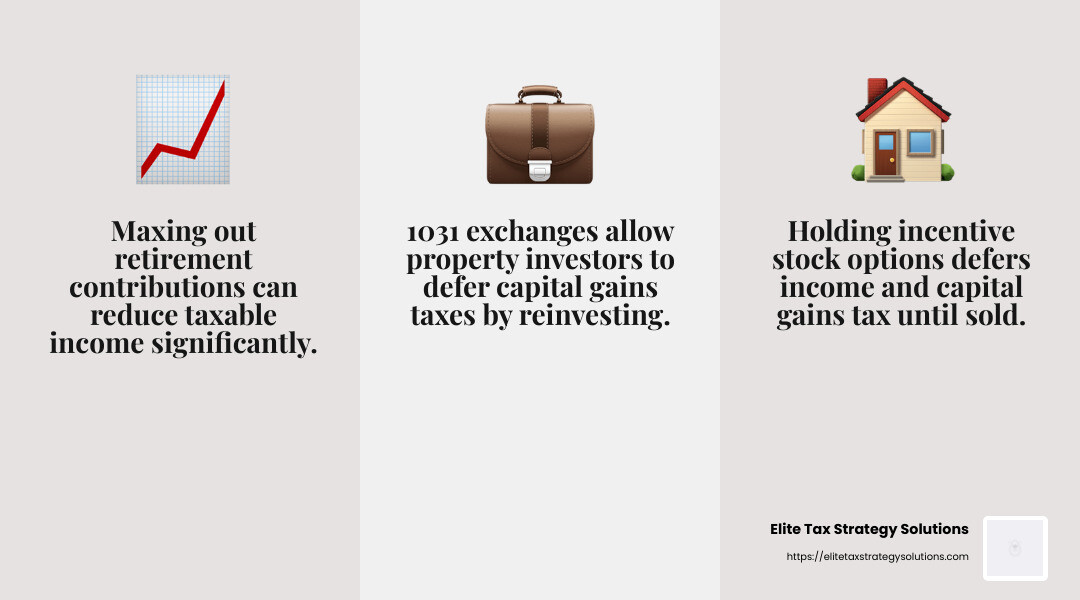

Increase Contributions: Max out your contributions to retirement accounts. This reduces your current taxable income since contributions are often made with pre-tax dollars.

-

Catch-Up Contributions: If you’re over 50, take advantage of catch-up contributions to defer even more income.

By increasing your retirement contributions, you not only save for the future but also lower your taxable income for the current year.

Incentive Stock Options

Stock options can be another tool for deferring income:

-

Hold Your Options: If your employer offers incentive stock options (ISOs), consider holding on to them. This defers income tax and capital gains tax until you sell the stock.

-

Plan the Timing: Carefully plan when to exercise and sell these options to manage your tax bracket effectively.

Incentive stock options can be a strategic way to manage both your income and your taxes if handled wisely.

Like-Kind Exchanges

Real estate investors can take advantage of like-kind exchanges to defer taxes:

-

Swap Properties: Under a 1031 exchange, you can defer capital gains taxes by reinvesting the proceeds from a sold property into a similar one.

-

Avoid Immediate Tax Liability: This strategy allows you to grow your real estate investments without the immediate tax burden.

Using like-kind exchanges can be a powerful way to build wealth through real estate while minimizing tax liabilities.

By employing these strategies, you can effectively defer income, manage your tax liability, and optimize your financial planning. This sets the stage for a more secure financial future.

Accelerating Deductions

Accelerating deductions is another smart way to manage your taxes. By moving certain expenses into the current year, you can reduce your taxable income. Let’s explore some key strategies: bunching deductions, prepaying expenses, and the 12-month rule.

Bunching Deductions

Bunching deductions means timing your expenses to maximize your tax benefits:

-

Group Expenses: If your itemized deductions are close to the standard deduction, try to group deductible expenses into one year. This way, you can itemize in one year and take the standard deduction the next.

-

Medical and Charitable Contributions: Consider scheduling medical procedures or making charitable donations in the same year to exceed the standard deduction threshold.

Bunching is a clever way to make the most of your deductions by concentrating them in a single year.

Prepaying Expenses

Prepaying expenses can also lower your taxable income for the current year:

-

Eligible Expenses: You can prepay certain expenses, like rent or insurance, if the benefit doesn’t extend beyond 12 months or the end of the next tax year.

-

Small Business Advantage: For small businesses, paying for supplies or services in advance can help reduce this year’s tax burden.

This strategy allows you to take advantage of deductions now, rather than waiting until the next year.

The 12-Month Rule

The 12-month rule is crucial for understanding when prepaid expenses are deductible:

-

Short-Term Benefits: If a prepaid expense provides benefits for 12 months or less, and doesn’t extend beyond the end of the next tax year, you can deduct it in the current year.

-

Cash Basis Taxpayers: This rule is particularly beneficial for cash basis taxpayers, as it allows for immediate deductions.

The 12-month rule helps ensure that your prepayments qualify for deductions, maximizing your tax savings.

By accelerating deductions through these methods, you can effectively manage your taxable income and potentially lower your tax bill. This approach complements income deferral strategies and helps optimize your financial planning.

Frequently Asked Questions about Deferring Income

Can you defer business income to the next year?

Yes, you can defer business income to the next year by employing a few strategic methods. If you’re a cash-basis taxpayer, you can delay sending invoices until the end of the year. By doing this, payments received in the following year won’t count as income for the current year, effectively pushing it forward. This is a common practice for small businesses looking to manage their cash flow and tax liability.

Another approach is to ask clients for installment payments on larger projects. This spreads the income over multiple years, reducing the immediate tax burden. However, always ensure that these strategies don’t disrupt your cash flow or client relationships.

Is deferring taxes always beneficial?

Deferring taxes isn’t always a one-size-fits-all solution. While it can lower your current year’s taxable income and possibly place you in a lower tax bracket, consider your future financial situation. If you expect to earn more next year or anticipate higher tax rates, deferring taxes might not be the best choice.

Additionally, the benefits of deferring taxes might be outweighed by potential risks, such as changes in tax laws or personal financial needs. It’s crucial to evaluate your unique situation and possibly consult with a tax professional to determine if deferring taxes aligns with your long-term financial goals.

How does deferring income affect tax brackets?

Deferring income can significantly impact your tax bracket. By pushing income to the next year, you might reduce your current year’s taxable income, potentially dropping you into a lower tax bracket. This can result in paying a lower percentage of taxes on your income.

For example, if you’re near the threshold of a higher tax bracket, deferring some income could save you a considerable amount in taxes. However, it’s important to plan carefully. If you defer too much income, you might end up in a higher bracket the following year, negating the benefits.

Consider your future income expectations and tax rate predictions when deciding how much income to defer. This strategic planning can help you optimize your tax situation over the long term.

Conclusion

Deferring income can be a powerful tool in your tax planning arsenal, but navigating the complexities requires more than just a basic understanding. That’s where we come in. At Elite Tax Strategy Solutions, we specialize in providing personalized tax planning services for high earners and closely held businesses.

Our proactive approach ensures that you not only maximize your tax savings but also align your financial strategies with your long-term goals. By working with seasoned tax professionals, you gain access to over 100 custom tax-saving strategies designed to improve your financial stability and optimize your tax position.

When it comes to deferring income, consulting with a tax professional can help you make informed decisions. Our team can guide you through the nuances of cash flow management, potential tax liabilities, and strategic planning to ensure you make the most of your income deferral opportunities.

Incorporating proactive tax planning into your financial strategy is not just about minimizing your current tax burden; it’s about setting the stage for future success. By understanding how to defer income to next year effectively, you can take control of your financial future and ensure you’re prepared for whatever comes next.

For more insights into innovative tax planning and to explore how we can assist you in achieving your financial aspirations, visit our Innovative Tax Planning page. Let’s work together to secure your financial future and optimize your tax strategy today.