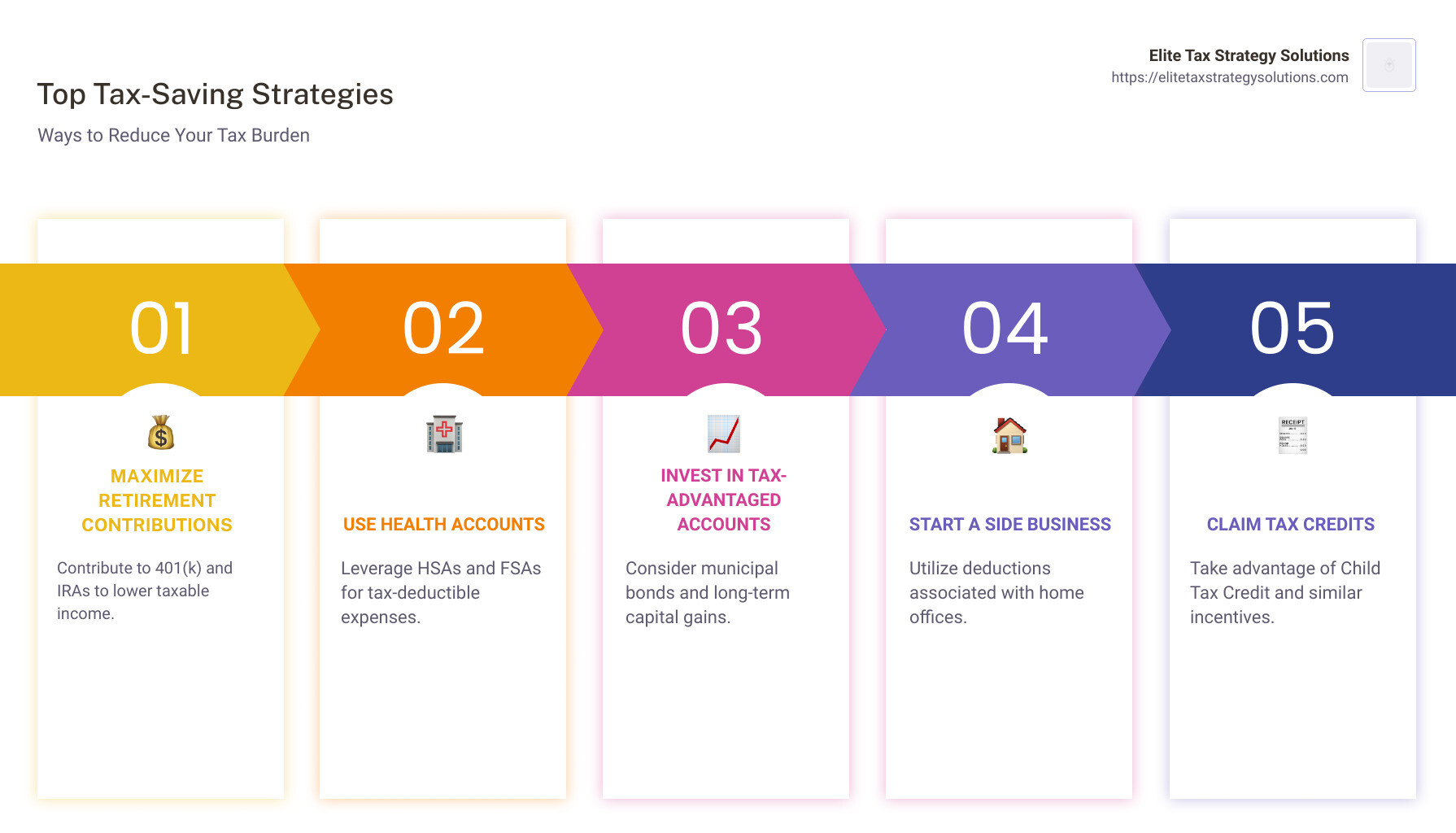

How can I save money on taxes? This is a question many high-income earners and small business owners face as they seek a pathway to financial stability. Here are some quick strategies that might help:

- Maximize contributions to retirement accounts like 401(k)s and IRAs.

- Use health savings accounts (HSAs) for tax deductions.

- Invest in tax-advantaged accounts such as municipal bonds.

- Consider starting a side business for potential deductions.

- Ensure you claim all eligible tax credits, like the Child Tax Credit.

In today’s complex tax landscape, effective tax planning isn’t just about filing your returns once a year. It’s a proactive approach to reduce tax liabilities and align with your financial goals. Tax planning offers a significant opportunity to improve your financial well-being by minimizing taxes and maximizing savings.

My name is David Fritch, and with over 40 years of experience in tax planning, I understand that the question of “how can I save money on taxes” is crucial for achieving financial stability. Through my work with Elite Tax Strategy Solutions, I’ve guided many individuals and businesses in reducing their tax burdens while reaching their long-term financial objectives.

Simple guide to how can i save money on taxes:

– Business tax management

– Comprehensive tax planning

– Tax risk management

Maximize Retirement Contributions

One of the most effective ways to save money on taxes is by maximizing your contributions to retirement accounts like 401(k)s and IRAs. These accounts are not just for saving for the future—they’re also powerful tools for reducing your taxable income today.

401(k) Plans

When you contribute to a 401(k) plan, you’re using pre-tax dollars. This means the money goes into your retirement account before taxes are taken out, reducing your taxable income. For example, if you earn $50,000 a year and contribute $5,000 to your 401(k), you’ll only pay taxes on $45,000.

In 2024, you can contribute up to $23,000 to your 401(k) if you’re under 50. If you’re 50 or older, you can make an additional catch-up contribution of $7,500. This is a great opportunity to boost your retirement savings while enjoying significant tax benefits.

Individual Retirement Accounts (IRAs)

IRAs are another fantastic way to lower your taxable income. You can contribute up to $7,000 annually to a traditional IRA if you’re under 50, and $8,000 if you’re 50 or older. The contributions you make to a traditional IRA may be tax-deductible, depending on your income level and whether you or your spouse are covered by a retirement plan at work.

Catch-up contributions are especially beneficial for those who are getting closer to retirement age. They allow you to contribute more than the standard limit, giving you a chance to make up for lost time and increase your retirement savings.

By maximizing your retirement contributions, you not only secure a more comfortable future but also answer the pressing question of how can I save money on taxes right now. As part of a proactive tax strategy, these contributions can significantly reduce your taxable income and help you achieve financial stability.

Next, we’ll explore how utilizing health accounts can provide additional tax advantages.

Use Health Accounts

Health accounts like Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) are excellent tools for reducing your taxable income. They not only help you cover medical expenses but also offer significant tax benefits.

Health Savings Accounts (HSAs)

An HSA is a tax-exempt account you can use to pay for qualified medical expenses. To contribute to an HSA, you must have a high-deductible health plan. The contributions you make are tax-deductible, and the withdrawals are tax-free when used for eligible medical expenses.

In 2024, you can contribute up to $4,150 if you have self-only coverage or $8,300 for family coverage. If you’re 55 or older, you can make an additional catch-up contribution of $1,000.

One of the best things about an HSA is that the funds roll over year after year. You don’t have to spend all the money in your account each year, allowing you to save for future medical expenses.

Flexible Spending Accounts (FSAs)

FSAs allow you to set aside pre-tax dollars for out-of-pocket medical expenses. The contributions lower your taxable income, which can lead to tax savings. However, unlike HSAs, FSAs usually have a “use it or lose it” policy. You need to spend the funds within the plan year, though some employers allow a small amount to carry over or a grace period to use the remaining balance.

For 2024, you can carry over up to $640 of unused FSA funds to the next year, or use them during a grace period of up to 2½ months after the plan year ends.

Tax Benefits of Health Accounts

Both HSAs and FSAs offer tax advantages by allowing you to use pre-tax dollars for medical expenses. This can significantly reduce your taxable income and answer the question of how can I save money on taxes.

By utilizing these health accounts, you not only manage healthcare costs efficiently but also enjoy substantial tax savings. Next, we’ll dive into how investing in tax-advantaged accounts can further optimize your tax strategy.

Invest in Tax-Advantaged Accounts

Investing in tax-advantaged accounts is a smart way to grow your wealth while minimizing your tax burden. Let’s explore two powerful options: municipal bonds and long-term capital gains.

Municipal Bonds

Municipal bonds, or “munis,” are issued by local governments to fund public projects like schools and roads. The big draw? Interest income from these bonds is generally exempt from federal taxes. If you live in the state where the bond is issued, you might also skip state and local taxes on that income.

This makes them a great choice for those in higher tax brackets. A 2023 report highlighted that municipal bonds have a default rate of just 0.08%, compared to 6.9% for global corporate bonds. This low risk adds to their appeal.

However, be cautious. If you buy a muni at a discount of less than 0.25%, you might face the “de minimis” tax, where the discounted amount is taxed as regular income.

Long-Term Capital Gains

Holding onto investments like stocks, bonds, or real estate for more than a year can lead to significant tax savings. Long-term capital gains are taxed at lower rates than short-term gains, which are taxed as ordinary income. Depending on your income, the tax rate for long-term capital gains could be 0%, 15%, or 20%.

For instance, in 2024, married couples filing jointly pay no tax on long-term capital gains if their taxable income is up to $94,050. This threshold rises slightly in 2025. Single filers have a limit of $47,025 in 2024.

Using long-term investments strategically can answer the question of how can I save money on taxes. You can also practice tax-loss harvesting, where you sell investments at a loss to offset gains, further reducing your tax liability.

By investing in municipal bonds and focusing on long-term capital gains, you can optimize your tax strategy and keep more of your hard-earned money. Next, we’ll explore how starting a side business can offer additional tax advantages.

Start a Side Business

Starting a side business can be a fantastic way to save money on taxes while pursuing your passions. By running a business, you can take advantage of various tax deductions that aren’t available to employees. Let’s break down the key benefits.

Deductions

When you operate a side business, many of your expenses can be deducted from your income. This includes costs like office supplies, travel expenses, and even a portion of your phone and internet bills if they’re used for business purposes. These deductions help lower your taxable income, meaning you pay less in taxes.

One of the notable deductions is for health insurance premiums. If you’re self-employed and meet certain requirements, you might be able to deduct your health insurance costs for yourself and your family.

Home Office

If you work from home, you might qualify for the home office deduction. This allows you to deduct a portion of your rent or mortgage, utilities, and other home-related expenses. However, the space must be used exclusively for business.

The IRS has specific guidelines, so it’s important to keep detailed records and ensure your home office meets the criteria. This can significantly lower your tax bill if done correctly.

Profit Intention

To claim these deductions, your business must be operated with the intention of making a profit. The IRS generally presumes you’re in business to make a profit if you earn a profit in three out of five consecutive years. This means you need to treat your side business as a real business: keep good records, separate personal and business finances, and market your services or products.

By starting a side business and carefully managing your expenses, you can take advantage of these tax benefits while pursuing something you enjoy. Next, we’ll dive into how claiming tax credits can further reduce your tax liability.

Claim Tax Credits

Tax credits are a powerful tool for saving money on taxes. Unlike deductions, which reduce your taxable income, credits directly reduce the amount of tax you owe. Let’s explore two valuable credits: the Child Tax Credit and the Earned Income Tax Credit.

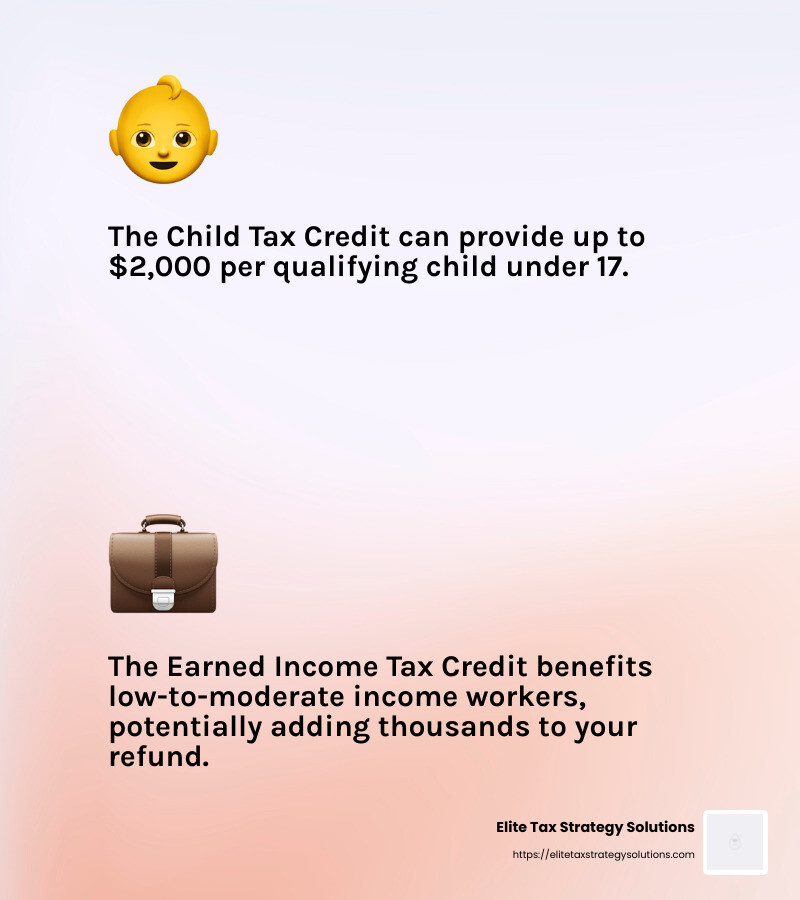

Child Tax Credit

The Child Tax Credit (CTC) can significantly reduce your tax bill if you have children. For each qualifying child under the age of 17, you can claim a credit of up to $2,000. This credit is partially refundable, meaning even if you don’t owe any taxes, you might still receive a refund.

To qualify, your child must have a valid Social Security number, live with you for more than half the year, and be claimed as a dependent on your tax return. The credit amount begins to phase out at higher income levels, so check the current thresholds.

Earned Income Tax Credit

The Earned Income Tax Credit (EITC) is designed to benefit low-to-moderate-income working individuals and families. Depending on your income and family size, the EITC can add up to several thousand dollars to your refund.

To qualify, you must have earned income from employment or self-employment, meet certain income limits, and not have investment income exceeding a specific amount. The EITC is fully refundable, which means if the credit is more than what you owe in taxes, you’ll receive the difference as a refund.

Maximizing Tax Savings

By understanding and utilizing these credits, you can significantly lower your tax liability. It’s crucial to keep detailed records and ensure you meet all eligibility requirements. If you’re unsure about qualifying, consulting a tax professional can be a wise move.

Next, we’ll tackle some frequently asked questions about tax savings to further improve your understanding of how to keep more of your hard-earned money.

Frequently Asked Questions about Tax Savings

How can I reduce my taxes on my income?

One of the most effective ways to reduce your taxable income is through retirement accounts. By contributing to accounts like a 401(k) or a traditional IRA, you can lower your taxable income since these contributions are often made with pre-tax dollars. This means you pay less in taxes now and save for your future at the same time.

Tax credits are another excellent method. Unlike deductions, which only reduce your taxable income, credits directly reduce the amount of tax you owe. For instance, the Child Tax Credit and the Earned Income Tax Credit can significantly cut down your tax bill.

What reduces the amount of tax due?

Tax credits and deductions are key players in reducing the amount of tax you owe. Credits like the Child Tax Credit directly reduce your tax bill, while deductions lower your taxable income. Common deductions include those for mortgage interest, student loan interest, and charitable donations.

Your filing status also impacts the amount of tax due. Whether you’re single, married, or head of household can change your tax bracket and affect the deductions and credits available to you.

How can I get more money off my taxes?

Getting more money off your taxes often involves strategic use of deductions and credits.

-

Filing Status: Choosing the correct filing status can maximize deductions and lower your tax rate. For example, the head of household status often offers more benefits than filing as single.

-

Tax Deductions: Itemizing deductions can sometimes lead to more savings than taking the standard deduction. This includes deductions for medical expenses, state and local taxes, and mortgage interest.

-

Tax Credits: Make sure you’re taking advantage of all the tax credits you’re eligible for. Credits like the Earned Income Tax Credit can result in a refund even if you owe no taxes.

By understanding these elements, you can effectively reduce your tax burden and keep more of your hard-earned money. Next, we’ll explore how proactive tax optimization can help achieve long-term financial success.

Conclusion

Proactive tax optimization is more than just a buzzword—it’s a powerful strategy to save money on taxes and achieve financial stability. At Elite Tax Strategy Solutions, we specialize in helping high earners and closely held businesses steer the complex world of tax planning. Our approach is thorough and personalized, ensuring that every client maximizes their tax savings while staying compliant with ever-changing tax laws.

Why Choose Us?

Our team of seasoned professionals is dedicated to finding the best strategies custom to your unique financial situation. Whether it’s maximizing deductions, leveraging tax credits, or exploring advanced tax-saving techniques, we’re here to guide you every step of the way.

-

Maximize Tax Savings: We help you identify and implement strategies that align with your financial goals.

-

Stay Compliant: Navigating tax laws can be daunting. We ensure you stay on the right side of the IRS with our compliance-first approach.

-

Achieve Financial Stability: By integrating tax planning with your broader financial objectives, we help you work towards long-term success.

Ready to optimize your taxes? Visit our Tax Planning for Small Businesses page to learn more about how we can help you achieve your financial goals. Let’s take the complexity out of tax planning and put more money back in your pocket.