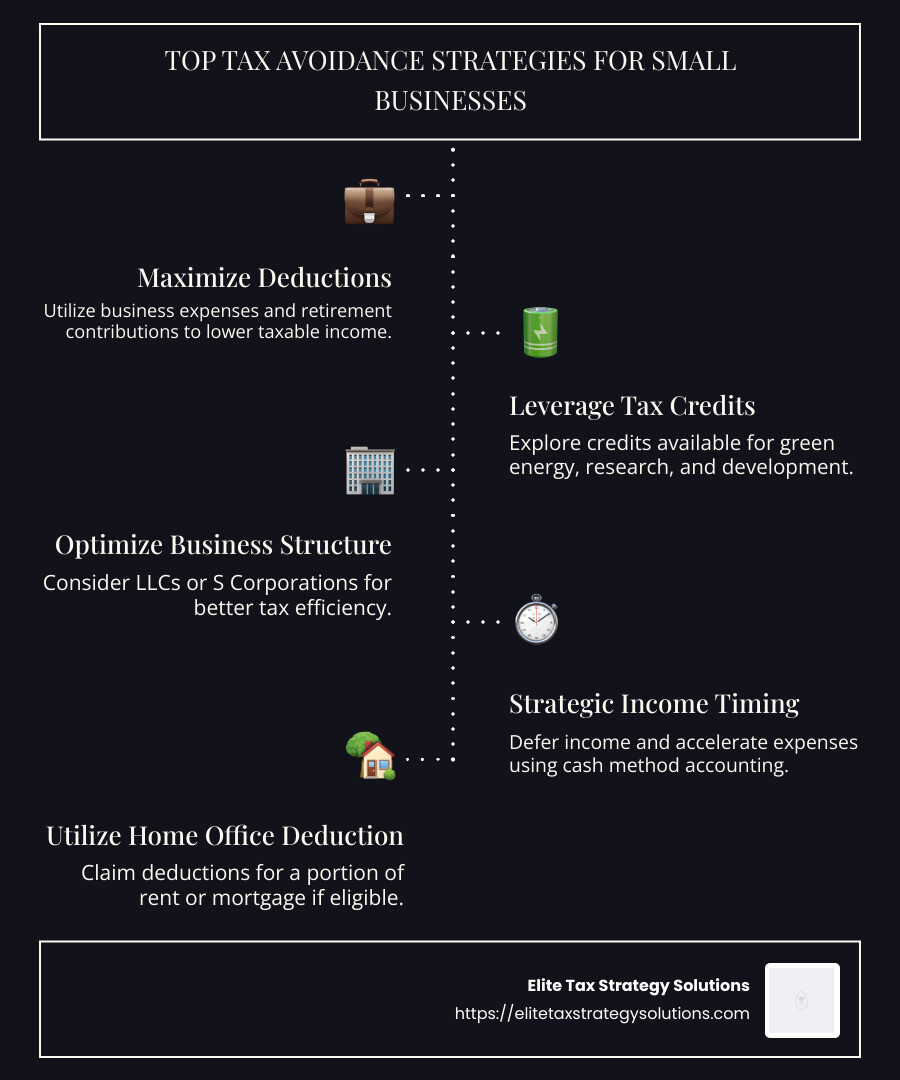

Tax avoidance strategies for small business are essential tools that can help entrepreneurs lower their taxable income legally, ultimately bolstering their financial stability and enabling growth. By utilizing these strategies, business owners can:

- Maximize deductions like business expenses and retirement contributions

- Leverage optimal tax credits available for various activities and investments

- Strategically time income and expenses to align with annual tax goals

These tactics aren’t about evading taxes illegally but strategically planning around existing laws to manage obligations effectively.

In today’s changing tax landscape, understanding the nuances of tax planning can be daunting, especially for small business owners dealing with tight margins and fluctuating revenues. Ensuring your tax strategy is optimized can be a game-changer, enhancing your business’s financial health significantly.

As David Fritch, with over 40 years of experience in tax law and business consulting, I’ve helped countless small businesses steer tax regulations. At Elite Tax Strategy Solutions, we specialize in tailoring tax avoidance strategies for small business needs, ensuring compliance and crafting approaches that align with long-term financial objectives.

Know your tax avoidance strategies for small business terms:

– small business tax planning strategies

– tax liability reduction

– tax risk management

Understanding Tax Evasion vs. Tax Avoidance

Tax evasion and tax avoidance are terms often used interchangeably, but they couldn’t be more different. Understanding these differences is crucial for any small business looking to remain compliant with tax laws while minimizing tax liabilities.

Legal Strategies vs. Illegal Practices

Tax avoidance is perfectly legal. It involves using the tax code to your advantage, employing strategies like deductions, credits, and deferrals to reduce what you owe. For example, contributing to a qualified retirement plan or claiming tax credits for energy-efficient equipment are common avoidance strategies. These are smart moves that keep more money in your business’s pocket.

On the other hand, tax evasion is illegal. It includes actions like underreporting income, inflating deductions, or hiding money in offshore accounts. These practices can lead to severe penalties, including fines and imprisonment.

Compliance: The Key to Effective Tax Planning

Staying compliant is the cornerstone of any effective tax strategy. While tax avoidance strategies for small business can significantly reduce your tax burden, they must be executed within the boundaries of the law. This means:

- Documenting all deductions and credits: Keep thorough records to substantiate your claims.

- Staying updated on tax law changes: The tax landscape changes frequently, and what was legal last year might not be this year.

- Consulting with tax professionals: Experts like those at Elite Tax Strategy Solutions can guide you through complex situations and ensure your strategies are both effective and legal.

Real-World Example

Consider a small business owner who strategically uses tax credits for installing solar panels. This move not only reduces their environmental impact but also lowers their tax liability, demonstrating a legal and smart approach to tax planning.

In contrast, a business owner who hides income from these panels to avoid taxes is engaging in evasion, risking severe consequences.

By understanding these differences and focusing on legal tax avoidance strategies, small businesses can optimize their tax positions without crossing into illegal territory. This not only safeguards them from penalties but also supports long-term financial health.

Tax Avoidance Strategies for Small Business

When it comes to tax avoidance strategies for small business, the goal is simple: legally minimize your tax burden while maximizing your financial health. Let’s explore some effective strategies that can help you achieve this.

Retirement Plans: Save for the Future and Reduce Taxes

Setting up a retirement plan is a win-win for small business owners. Not only does it help you save for the future, but it also provides immediate tax benefits. Options like a SIMPLE IRA, SEP IRA, or a solo 401(k) allow you to contribute pre-tax dollars, reducing your taxable income.

For instance, a SEP IRA lets you contribute up to 25% of your compensation, capped at $69,000 for 2024. This means more money in your retirement account and less taxable income now. Plus, offering a retirement plan can make your business more attractive to potential employees.

Equipment Deductions: Invest in Growth and Cut Taxes

Investing in business equipment? You can benefit from Section 179 deductions, which allow you to deduct the full purchase price of qualifying equipment. For 2025, this deduction is up to $1,250,000 with a phase-out threshold of $3,130,000.

If you’ve maxed out your Section 179 deductions, consider Bonus Depreciation. You can deduct 40% of the cost in 2025, making it a great option for businesses looking to expand.

Timing is crucial. If you anticipate higher profits next year, consider delaying purchases to maximize deductions when you need them most.

Green Energy Credits: Go Green and Save Green

The federal government offers tax credits to businesses that invest in clean energy technologies. Under the Inflation Reduction Act, businesses can claim credits for installing solar panels, buying electric vehicles, or making other eco-friendly improvements.

These green energy credits not only lower your tax bill but also improve your brand’s eco-credentials. Check with your tax advisor to understand which credits apply to your business and how to claim them.

By leveraging these tax avoidance strategies for small business, you can effectively reduce your tax burden while investing in your business’s growth and sustainability. Properly implemented, these strategies not only improve your financial health but also improve your business’s long-term prospects.

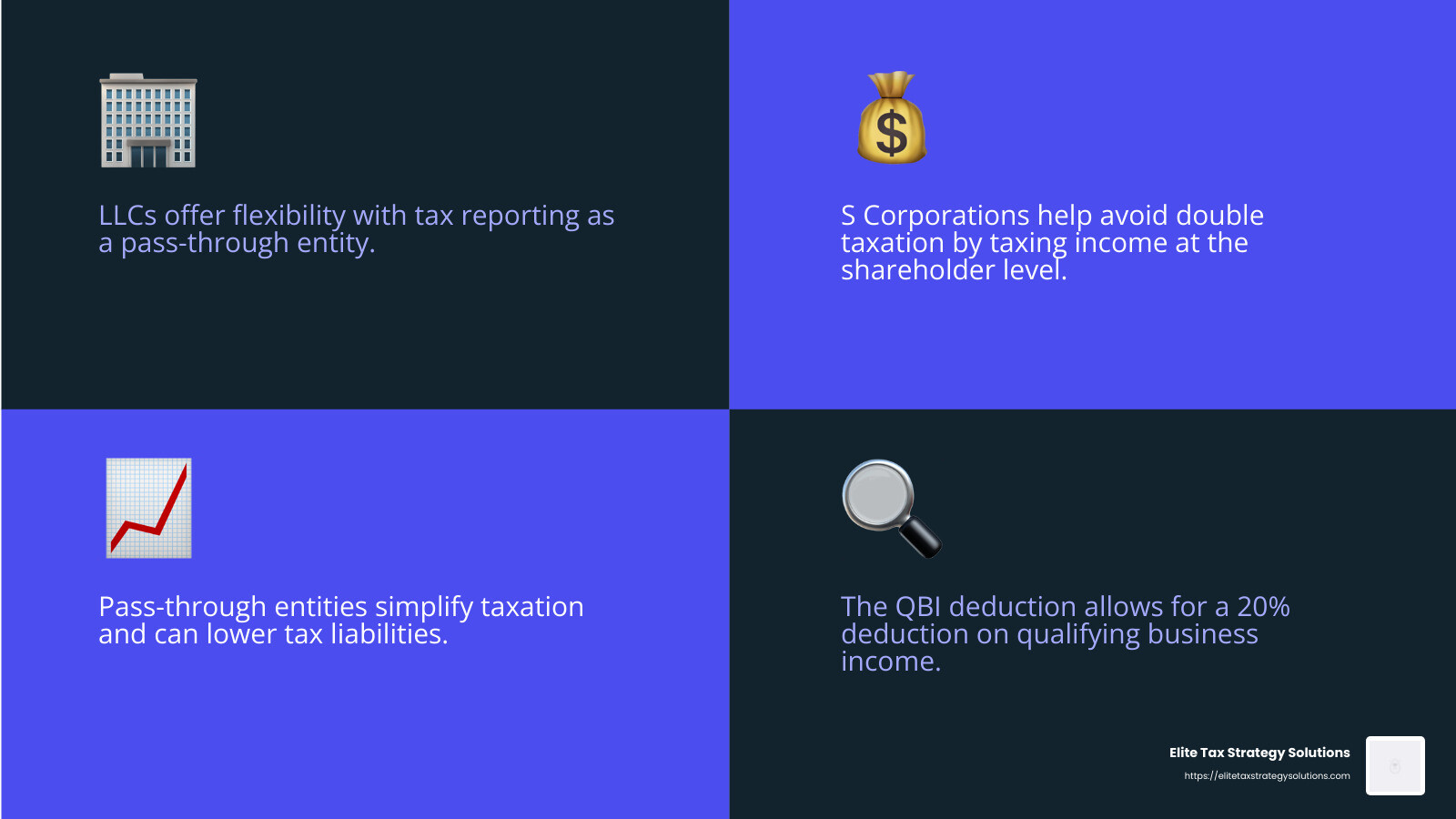

Optimize Business Structure for Tax Efficiency

Choosing the right business structure is crucial for minimizing taxes and optimizing your financial health. Let’s explore how different structures like LLCs, S Corporations, and pass-through entities can impact your tax efficiency.

LLC: Flexibility and Simplicity

A Limited Liability Company (LLC) offers a flexible structure with significant tax benefits. As a pass-through entity, an LLC’s income is reported on the owner’s personal tax return, avoiding double taxation. This means you only pay taxes on profits once, unlike a traditional corporation.

In many states, including Utah and Indiana, LLCs can elect to be taxed as S Corporations, potentially saving on self-employment taxes. This flexibility makes LLCs an attractive option for small business owners looking to optimize their tax situation.

S Corporation: Avoid Double Taxation

S Corporations provide another excellent way to avoid double taxation. Like LLCs, they are pass-through entities, meaning income is taxed at the shareholder level. This structure can be beneficial if your business generates significant profits.

One advantage of an S Corporation is the ability to pay yourself a reasonable salary and take the remaining profits as distributions. These distributions are not subject to self-employment taxes, leading to potential savings.

However, S Corporations have specific rules and limitations, such as a cap on the number of shareholders. It’s essential to consult with a tax advisor to determine if this structure aligns with your business goals.

Pass-Through Entities: Simplifying Taxation

Pass-through entities, including sole proprietorships, partnerships, LLCs, and S Corporations, are designed to pass income directly to owners, who then report it on their personal tax returns. This structure simplifies taxation and can result in lower tax liabilities.

Under the Qualified Business Income (QBI) deduction, pass-through entities may qualify for a deduction of up to 20% of business income. This deduction can significantly reduce your taxable income, offering substantial savings.

For example, a small business in Jasper, Indiana, structured as a pass-through entity, can leverage state-specific tax benefits while maximizing federal deductions.

Choosing the right business structure is a key step in your tax planning strategy. By understanding the benefits of LLCs, S Corporations, and pass-through entities, you can make informed decisions that align with your business goals and optimize your tax efficiency.

Leverage Tax Deductions and Credits

Tax deductions and credits are powerful tools for small businesses to lower their tax burden. Let’s explore some effective strategies, including the Qualified Business Income (QBI) deduction, home office deduction, and fringe benefits.

Qualified Business Income (QBI) Deduction: A Big Saver

The QBI deduction is a significant tax break for small business owners. It allows pass-through entities like LLCs and S Corporations to deduct up to 20% of their qualified business income. However, there are important rules to follow.

For businesses categorized as specified service trades or businesses (SSTBs), the QBI deduction starts to phase out if your total taxable income exceeds $191,950 (single) or $383,900 (married filing jointly) in 2024. Once your income surpasses $241,950 (single) or $483,900 (married), the deduction is unavailable.

If your business isn’t an SSTB, you can still claim the deduction, but it is limited to either 50% of your share of W-2 wages or 25% of those wages plus 2.5% of your share of qualified property. It’s a bit complex, so consulting a tax professional is wise.

Home Office Deduction: Work from Home, Save on Taxes

If you work from home, the home office deduction can be a valuable tax-saving strategy. To qualify, you must use a part of your home regularly and exclusively for business. There are two ways to calculate this deduction:

- Simplified Method: Deduct $5 per square foot of your home used for business, up to 300 square feet.

- Actual Expenses Method: Calculate the percentage of your home used for business and deduct that portion of expenses like mortgage interest, rent, utilities, and repairs.

This deduction can make a big difference, especially for those running a business from a home office in places like Jasper, Indiana.

Fringe Benefits: More Than Just Perks

Offering fringe benefits is another excellent way to reduce your tax liability. Instead of increasing wages, which raises employment taxes, consider providing tax-exempt benefits. Some options include:

- Medical and dental insurance

- Childcare assistance

- Tuition reimbursement

- Employee meals

These benefits not only reduce your taxable income but also boost employee satisfaction.

By leveraging these tax deductions and credits, small business owners can significantly reduce their tax burden, keeping more money in their pockets to reinvest in their business. Up next, we’ll explore how timing your income and expenses can further optimize your tax strategy.

Timing Income and Expenses

Timing your income and expenses strategically can be a game-changer for small businesses. Let’s explore how deferring income, accelerating expenses, and using the cash method of accounting can help you save on taxes.

Defer Income: Push Earnings to the Next Year

One effective way to manage your tax bill is by deferring income. This means delaying the receipt of income until the next tax year. If you anticipate being in a lower tax bracket next year, this strategy can be particularly beneficial.

For example, if you performed services in December 2024 but haven’t billed your client yet, consider sending the invoice in January 2025. This way, the income is recognized in 2025, potentially lowering your 2024 tax liability. But be cautious—don’t delay billing clients who are slow payers, as this could affect your cash flow.

Accelerate Expenses: Bring Forward Deductions

On the flip side, you can accelerate expenses to reduce your taxable income for the current year. If you’re in a high tax bracket this year, this strategy can be especially advantageous.

Consider prepaying expenses like office rent or insurance premiums at the end of the year. According to IRS rules, you can deduct these expenses as long as the benefit period doesn’t exceed 12 months. Another option is to purchase necessary equipment or supplies before the year ends, allowing you to deduct those costs sooner.

Cash Method Accounting: Simple and Flexible

Many small businesses use the cash method of accounting because it’s straightforward. Under this method, you report income when you receive it and expenses when you pay them. This allows for greater flexibility in timing income and expenses.

For instance, if you expect next year’s tax rates to rise, you might want to accelerate income into the current year by sending out invoices promptly and encouraging clients to pay early. Conversely, if you anticipate lower income next year, deferring income and accelerating expenses can help manage your tax burden effectively.

By leveraging these tax avoidance strategies for small business, you can optimize your tax position. Up next, we’ll answer some frequently asked questions about these strategies to further clarify how they can benefit your business.

Frequently Asked Questions about Tax Avoidance Strategies

How can small businesses avoid owing taxes?

Small businesses can avoid owing taxes by leveraging various tax deductions and credits. One effective approach is to take advantage of retirement plans like a SEP IRA or a SIMPLE IRA. These plans not only help business owners save for the future but also provide significant tax deductions.

Another strategy is to use itemized deductions. If your deductible expenses exceed the standard deduction, itemizing can reduce your taxable income. Keep track of expenses like mortgage interest, medical expenses, and charitable contributions to see if itemizing would benefit you.

How to pay no taxes for a small business?

While it’s challenging to pay no taxes at all, small businesses can significantly reduce their tax liability through tax exemptions and timely renewals. For instance, certain startup expenses can be exempt from taxes, and staying on top of deadlines for renewing licenses and permits can prevent unnecessary penalties.

Additionally, exploring tax credits like the Research and Development (R&D) Credit or green energy credits can further lower your tax bill. Unlike deductions that reduce taxable income, credits directly reduce the amount of tax owed, making them highly valuable.

Which is an example of a tax avoidance strategy?

A classic example of a tax avoidance strategy is leveraging equipment deductions. Under the Section 179 Deduction, businesses can deduct the full purchase price of qualifying equipment or software purchased during the tax year. This deduction is designed to encourage businesses to invest in themselves and grow.

Another example is timing income and expenses. By carefully managing when you recognize income and pay expenses, you can optimize your tax situation. For instance, deferring income to the next year or accelerating expenses into the current year can help align your tax liability with your financial goals.

These strategies, when used wisely, can help small businesses minimize their tax burden and keep more money working for them. Up next, we’ll explore how optimizing your business structure can further improve tax efficiency.

Conclusion

At Elite Tax Strategy Solutions, we know that tax planning isn’t just about numbers—it’s about creating a roadmap to financial success. Our personalized tax planning services are designed to help small businesses maximize their tax savings and achieve long-term financial stability.

Proactive planning is at the heart of what we do. We don’t just react to tax changes; we anticipate them. By staying ahead of the curve, we ensure that your business is always in the best possible position to take advantage of tax-saving opportunities.

Whether you’re looking to optimize your business structure, leverage deductions and credits, or time your income and expenses effectively, our team is here to guide you every step of the way. We specialize in helping high earners and closely held businesses steer the complexities of tax regulations with confidence and ease.

Let us help you open up the full potential of your business with a tax strategy custom to your unique needs. Find how our personalized tax planning solutions can transform your financial future. Contact us today to get started on your journey to smarter tax planning and greater financial stability.