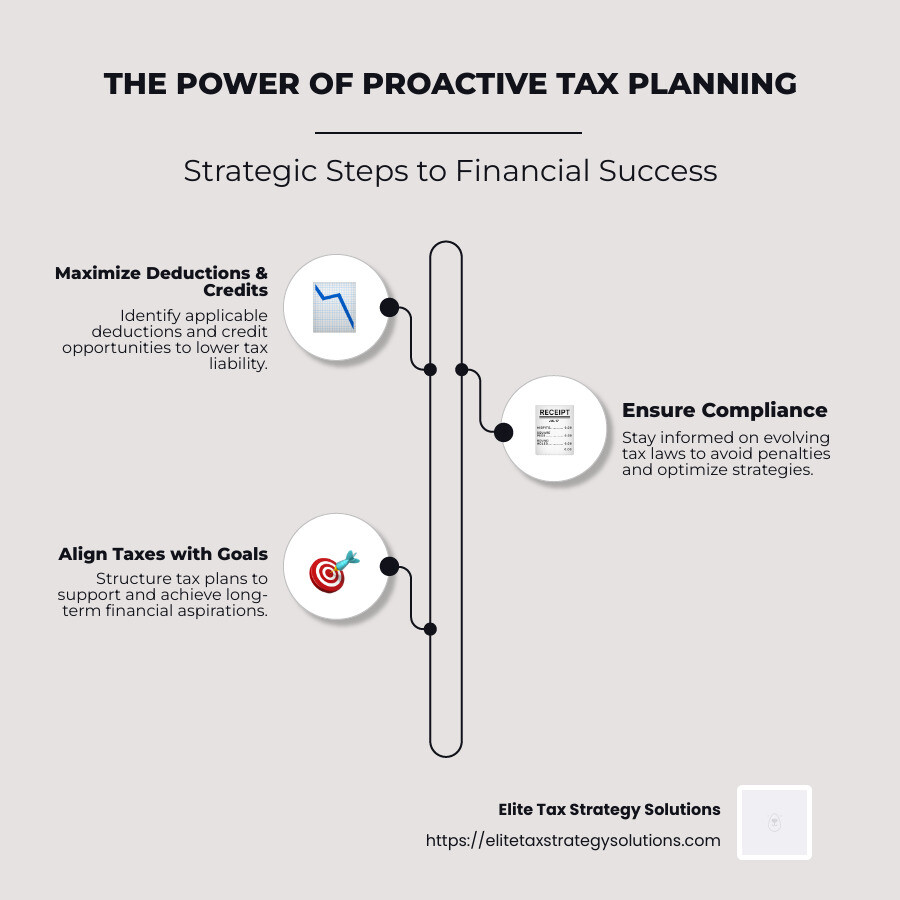

Proactive tax planning is more than just a task to check off your financial to-do list; it’s a strategic approach designed to optimize your taxes, ensure financial stability, and align with long-term financial goals. By focusing on proactive tax strategies, you can:

- Maximize deductions and credits to reduce tax liability.

- Ensure compliance with evolving tax laws.

- Avoid unexpected tax bills by aligning your taxes with financial aspirations.

Incorporating proactive tax planning can ease the burden of tax season, providing a smoother path to achieving your financial goals.

I’m David Fritch, with over 40 years of experience in proactive tax strategies and financial planning. My focus has been on helping high-income earners and small business owners optimize their tax outcomes and achieve financial stability.

Proactive tax word guide:

– benefits of tax planning

– business tax savings strategies

– tax planning for high earners

Understanding Proactive Tax Planning

Proactive tax planning is all about looking ahead and making smart decisions to minimize your tax obligations. Instead of waiting until tax season to think about your taxes, you’re planning throughout the year. This approach not only helps you save money but also aligns your tax strategy with your overall financial goals.

Tax Planning: More Than Just Filing

Tax planning is more than just filing your taxes every April. It’s about understanding the tax laws and using them to your advantage. The U.S. tax code is complex, but within it are many opportunities to save. By understanding your tax bracket and how changes in income can affect your taxes, you can make informed decisions to keep more of your earnings.

Seizing Tax Law Opportunities

Tax laws are always changing, and what worked last year might not work this year. Staying informed about these changes is crucial. For instance, contributing to a 401(k) or IRA can reduce your taxable income, which means you pay less in taxes now while saving for retirement.

Tip: Maximizing contributions to retirement accounts not only lowers your taxable income but also helps your savings grow tax-deferred. This is a key strategy for long-term financial health.

Minimizing Tax Obligations

One way to minimize tax obligations is by maximizing deductions and credits. This might include deductions for mortgage interest, student loans, or medical expenses. Credits, such as the Earned Income Tax Credit, directly reduce the amount of tax you owe and can be even more beneficial than deductions.

Another strategy is tax-loss harvesting, where you sell investments at a loss to offset any gains you might have. This can lower your taxable income and reduce your tax bill.

Remember: Being proactive with your taxes means planning ahead, not just reacting at the end of the year. This approach helps you avoid surprises and ensures you’re making the most of the tax laws to benefit your financial situation.

By understanding these concepts and integrating them into your financial strategy, you can achieve significant tax savings and work towards your long-term financial goals.

Key Strategies for Proactive Tax Planning

When it comes to proactive tax planning, understanding and utilizing key strategies can make a big difference in your financial outcomes. Let’s explore some essential tactics.

Understanding Tax Brackets

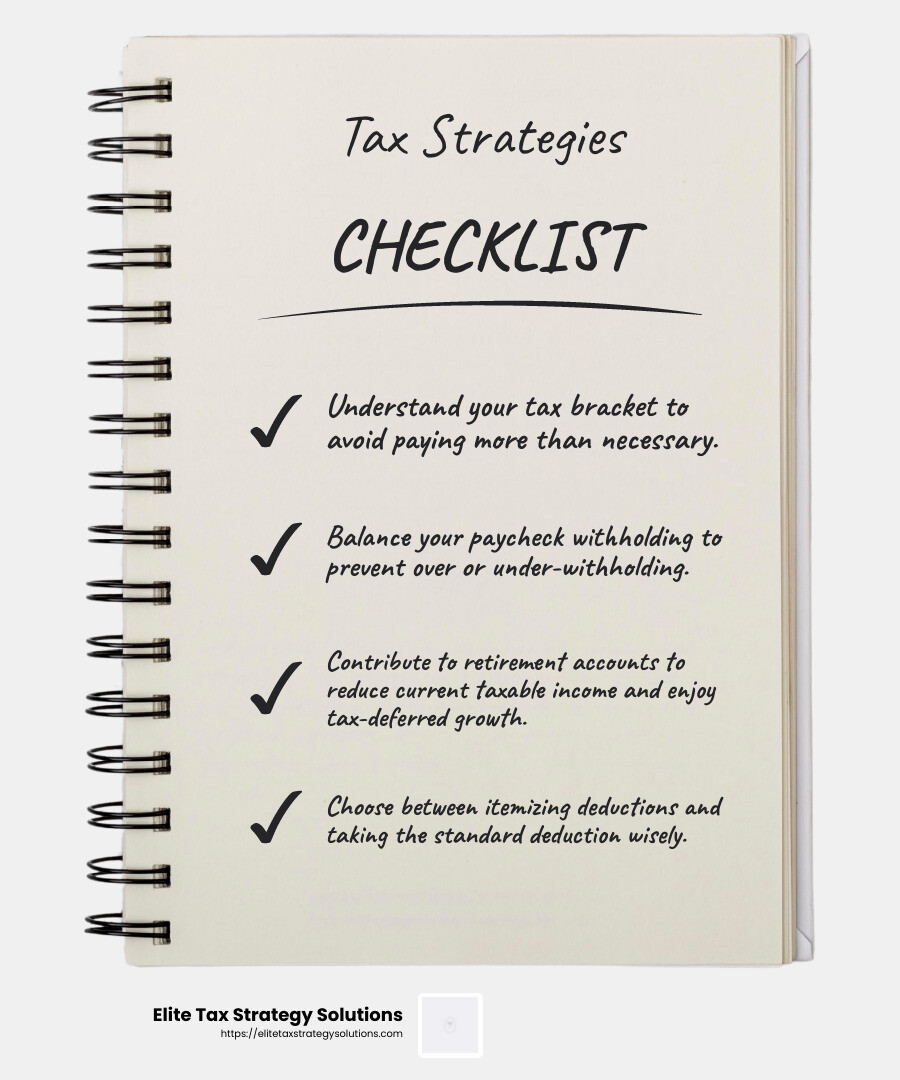

The U.S. has a progressive tax system, which means your tax rate increases as your income rises. There are seven federal income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Knowing your tax bracket helps you plan effectively. If you’re on the cusp of a higher bracket, strategic decisions can keep you from paying more taxes than necessary.

Withholding Strategies

Withholding the right amount from your paycheck is crucial. If you withhold too much, you’re giving the government an interest-free loan. Withhold too little, and you might face a hefty bill come tax time. The IRS tax withholding estimator can help you find the right balance, ensuring you’re not over or under-withholding.

Reducing Taxable Income

Reducing your taxable income is a smart way to lower your tax bill. Contributing to retirement accounts like a 401(k) or IRA is a common method. These contributions reduce your income now and grow tax-deferred, making them a double win for your finances.

Estimated Tax Payments

If you’re self-employed or have significant non-wage income, you may need to make estimated tax payments. This involves paying taxes throughout the year on income not subject to withholding. It’s a proactive step to avoid penalties and manage cash flow.

Itemize vs. Standard Deductions

Choosing between itemizing deductions and taking the standard deduction can impact your tax liability. Itemizing allows you to deduct specific expenses, such as mortgage interest and medical expenses. However, if your itemized deductions don’t exceed the standard deduction, it’s better to take the standard amount.

Keeping Up with Tax Documentation

Good record-keeping is essential. Having organized tax documentation ensures you can take advantage of deductions and credits you’re entitled to. This includes keeping receipts, tracking expenses, and maintaining records of charitable donations.

In Summary: Proactive tax planning requires understanding your tax situation, making informed decisions, and staying organized throughout the year. By employing these strategies, you can optimize your tax obligations and work towards achieving your financial goals.

Benefits of Proactive Tax Planning

Taking a proactive tax approach isn’t just about numbers on a form—it’s about shaping your financial future. Let’s explore how this strategy can benefit you.

Tax Savings

The primary goal of proactive tax planning is to save money. By planning ahead, you can take advantage of deductions, credits, and other tax-saving opportunities. For instance, maximizing retirement contributions or utilizing tax-loss harvesting can significantly reduce your taxable income. These strategies ensure you’re not paying more taxes than necessary, keeping more money in your pocket.

Better Financial Decisions

Planning your taxes proactively gives you a clearer picture of your financial health. With an accurate understanding of your tax obligations, you can make informed financial decisions. Whether it’s deciding when to sell an asset or choosing the right investment strategy, having a proactive tax plan helps you align these decisions with your long-term financial goals.

Improved Cash Flow

Cash flow is crucial for both individuals and businesses. Proactive tax planning helps manage cash flow by avoiding unexpected tax bills. By estimating taxes throughout the year and adjusting withholdings or estimated payments, you ensure that your cash flow remains steady. This means fewer surprises and more control over your finances.

Wealth Preservation

Preserving wealth isn’t just about earning more; it’s also about keeping more of what you earn. Proactive tax planning plays a vital role in this. By minimizing tax liabilities and maximizing tax-efficient strategies, you protect your wealth from unnecessary erosion due to taxes. This preservation is essential for achieving long-term financial stability and growth.

Incorporating proactive tax planning into your financial strategy offers these and more benefits. It’s about taking control, optimizing your financial situation, and ensuring your hard-earned money works for you.

Frequently Asked Questions about Proactive Tax

What does it mean to be proactive in tax?

Being proactive in tax means planning ahead to optimize your tax situation. Instead of waiting until tax season, you actively manage your taxes throughout the year. This includes understanding your tax bracket and adjusting your withholding amounts to avoid surprises. By being proactive, you can take advantage of tax-saving opportunities and make informed financial decisions that align with your long-term goals.

What is proactive tax planning?

Proactive tax planning involves using available tax law opportunities to minimize your tax obligations. It’s about looking ahead and anticipating future tax events. For example, if you’re nearing a higher tax bracket, you might adjust your income or deductions to stay in a lower bracket. This future planning helps you avoid unexpected tax bills and ensures you’re not missing out on any benefits.

What is the difference between pre-tax and pro-tax?

Pre-tax refers to income or contributions made before taxes are deducted. For instance, contributions to a traditional 401(k) are made with pre-tax dollars, reducing your taxable income. These contributions grow tax-free until withdrawal. On the other hand, proactive tax planning is a broader strategy focusing on optimizing your entire tax situation. It includes actions like maximizing deductions and planning for qualified withdrawals to manage taxable income effectively.

By understanding these concepts, you can better steer the complexities of taxes and make informed decisions that support your financial well-being.

Conclusion

At Elite Tax Strategy Solutions, we believe that personalized services are key to effective tax planning. Our approach is custom to meet the unique needs of high earners and closely held businesses. We understand that managing substantial tax burdens requires more than just filling out forms—it’s about strategic planning and making smart financial decisions.

Our team specializes in helping clients maximize their tax savings and achieve financial stability. We work closely with you to develop a comprehensive plan that aligns with your long-term goals. Whether you’re a high-income earner or a business owner, our proactive tax strategies are designed to optimize your tax position and ensure compliance with ever-changing regulations.

Operating in locations like Jasper, Indiana, and other suburban areas near major cities, we are committed to being your trusted partner in navigating the complex tax landscape. Our goal is to provide you with the tools and knowledge you need to make informed decisions and preserve your wealth.

For more information on how our innovative tax planning services can benefit you, visit our Innovative Tax Planning page. Let us help you take control of your tax situation and secure your financial future.