Deduction optimization is a critical aspect of tax planning and tax optimization that can help you keep more of your hard-earned money. By making strategic decisions about your expenses, you can greatly reduce your taxable income.

Here’s a quick snapshot to kickstart your deduction optimization journey:

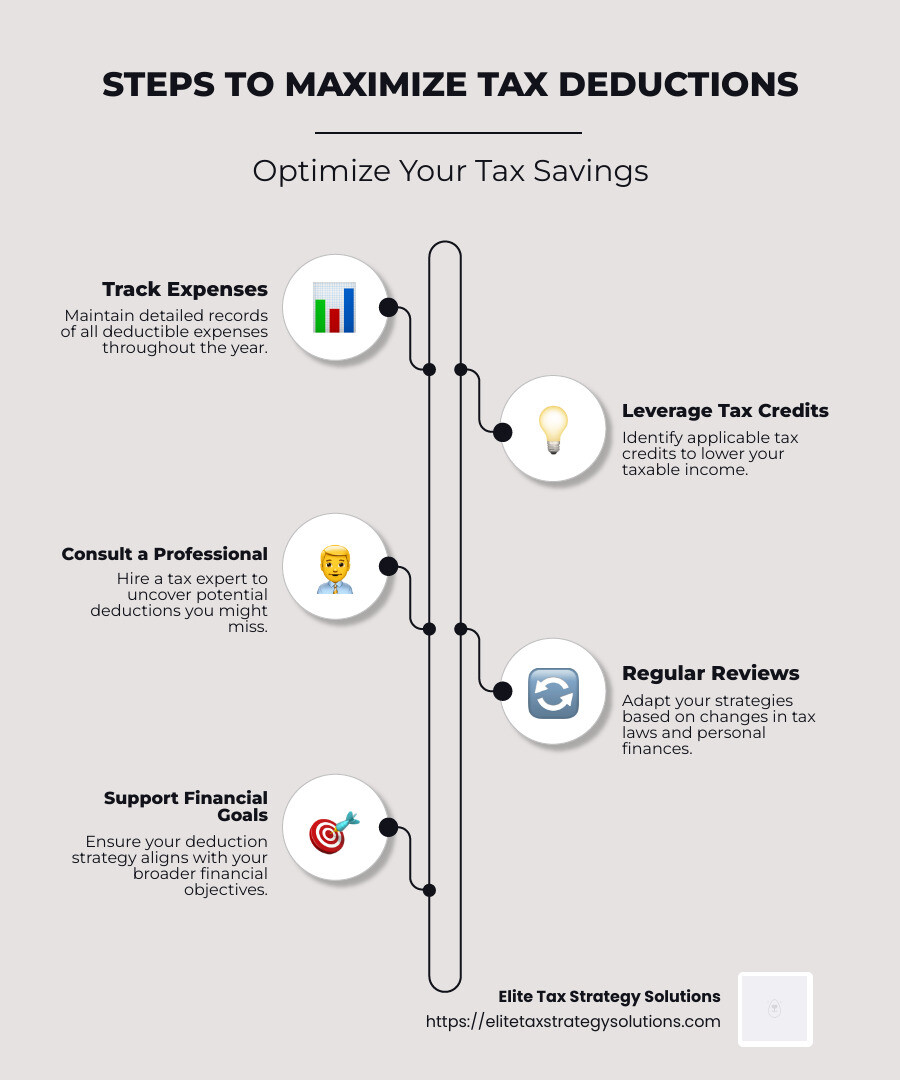

- Track Expenses: Keep a detailed record of all deductible expenses.

- Leverage Tax Credits and Deductions: Understand which apply to you and claim them.

- Consult a Professional: A tax expert can uncover deductions you might miss.

- Regular Reviews: Update your strategies as tax laws and personal finances change.

Maximizing deductions isn’t just about saving money—it’s about crafting a strategy that supports your financial goals.

I’m David Fritch. With over 40 years of experience in tax law and financial planning, I’ve helped many steer the intricacies of deduction optimization to maximize savings and achieve fiscal predictability.

Essential deduction optimization terms:

– comprehensive financial planning

– tax planning for businesses

Understanding Tax Deductions

Tax deductions are a powerful tool to reduce your taxable income, which in turn lowers your tax bill. They are expenses the IRS allows you to subtract from your total income, reducing the amount of income that’s subject to taxation.

Standard vs. Itemized Deductions

When it comes to deductions, you have two main options: standard and itemized deductions. The choice between them can significantly impact your tax savings.

-

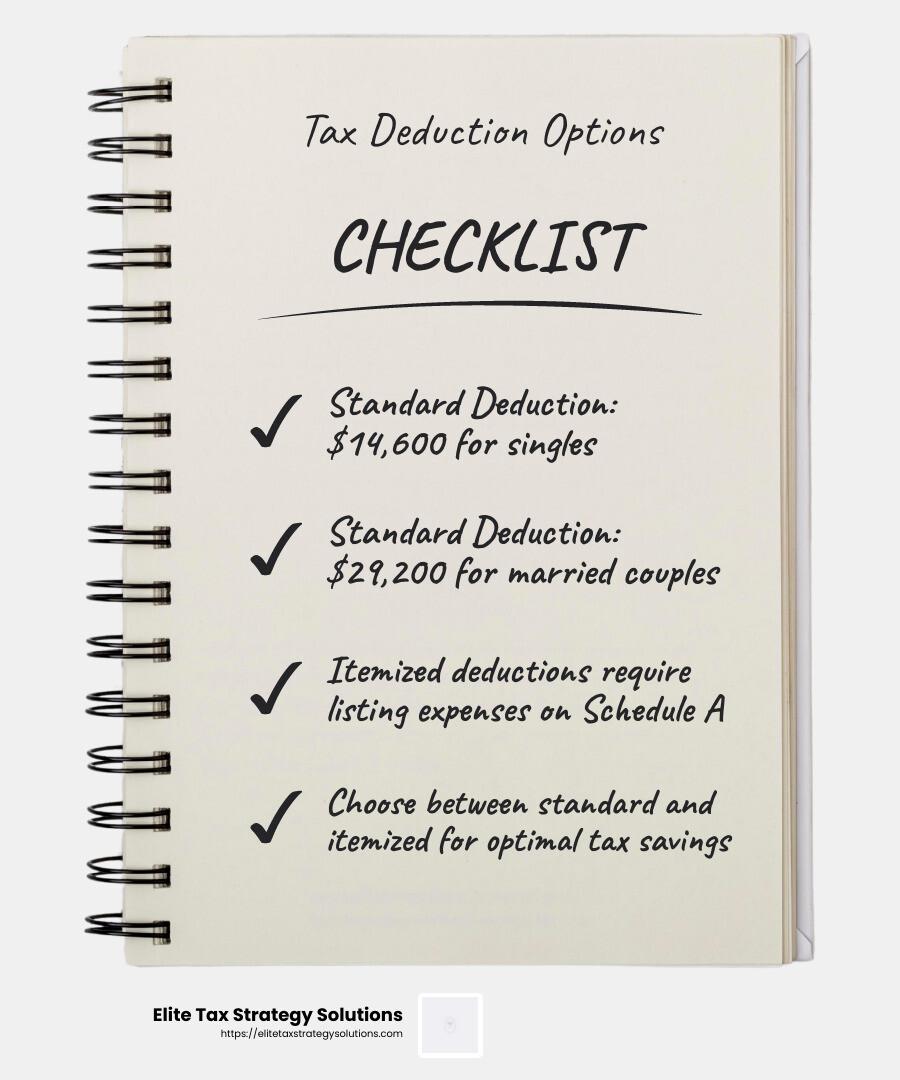

Standard Deduction: This is a fixed dollar amount that reduces your taxable income. For 2024, the standard deduction is $14,600 for single filers and $29,200 for those married filing jointly. It’s a straightforward way to lower your taxes without needing to track individual expenses.

-

Itemized Deductions: If your deductible expenses exceed the standard deduction, itemizing may be the better option. This requires listing all eligible expenses, like mortgage interest, medical expenses, and charitable contributions, on Schedule A of your tax return.

Choosing Between Standard and Itemized

The decision to itemize or take the standard deduction depends on your personal financial situation. For many, the increase in the standard deduction under the Tax Cuts and Jobs Act makes it unnecessary to itemize. However, if you have significant deductible expenses, itemizing could lead to greater tax savings.

Common Itemized Deductions

Some of the most common itemized deductions include:

- Homeownership Costs: Mortgage interest and property taxes can be deducted if you itemize.

- Medical Expenses: You can deduct medical expenses that exceed 7.5% of your adjusted gross income.

- Charitable Contributions: Donations to qualified organizations can be deducted, typically up to 60% of your adjusted gross income.

Above-the-Line Deductions

These are deductions you can take even if you don’t itemize. They reduce your adjusted gross income and include things like student loan interest and contributions to health savings accounts (HSAs).

Understanding and choosing the right deductions is a key part of deduction optimization. This ensures you’re not paying more in taxes than you have to, keeping more money in your pocket for savings and investments.

Deduction Optimization Strategies

Deduction Optimization is about getting the most out of your tax deductions to save money. It’s a key part of tax planning that can help you reduce your tax bill and keep more cash in your pocket.

Maximize Your Deductions

To optimize deductions, you need to maximize what you can claim. This means knowing all the deductions available to you and ensuring you qualify for them.

-

Bunching Deductions: If you have expenses that are close to the deductible threshold, consider bunching them into one tax year. For example, if your medical expenses are just below the deductible limit, try to pay for upcoming procedures within the same year to exceed the threshold.

-

Keep Detailed Records: Always keep track of your expenses. A simple spreadsheet or app can help you record expenses like travel, home office, or vehicle use. This way, you won’t miss out on any deductions when tax season comes around.

-

Use a Checklist: A checklist of allowable deductions can prevent you from missing out on potential savings. Consider categories like medical expenses, charitable contributions, and business expenses.

Use Tax Credits

Tax credits are often more valuable than deductions because they directly reduce the amount of tax you owe. Here are some credits to consider:

-

Earned Income Tax Credit (EITC): This is for low- to moderate-income earners and can significantly reduce your tax bill.

-

Childcare Credit: If you have children under 17, you could be eligible for a credit of up to $2,000 per child in 2024.

-

Small Business Health Insurance Premiums Credit: If you’re a small business owner with fewer than 25 employees, you might qualify for this credit if you pay at least 50% of your employees’ health insurance premiums.

Strategic Tax Planning

Effective tax planning involves looking at your overall financial picture and making strategic decisions to minimize taxes.

-

Retirement Contributions: Max out your 401(k) or traditional IRA contributions. These not only prepare you for the future but also reduce your taxable income now.

-

Health Savings Accounts (HSAs): If you have a high-deductible health plan, contribute to an HSA. Contributions are tax-deductible, and withdrawals for medical expenses are tax-free.

-

Charitable Donations: Consider making charitable donations in a year when you plan to itemize deductions. This can help reduce your taxable income significantly if you donate to qualified organizations.

Stay Informed

Tax laws change frequently, so staying informed is crucial. Regularly check for updates from trusted sources like the IRS website or consult with a tax professional to ensure you’re taking full advantage of available deductions and credits.

By understanding and applying these deduction optimization strategies, you can effectively manage your tax obligations and improve your financial health.

Top Quick Deductions to Maximize Savings

To keep more of your hard-earned money, understand some of the top deductions that can help you maximize savings. Here’s a quick rundown of key areas where you can optimize your deductions:

Charitable Donations

Giving to charity not only helps those in need but can also provide you with a tax break. When you donate to a qualified charity, you can deduct the value of your donation from your taxable income. Make sure you get a receipt for every donation and keep a detailed record. For donations over $500, you’ll need to fill out IRS Form 8283, and if it’s over $5,000, an official appraisal is required.

Tip: Consider donating household goods. You can deduct their current market value, and it’s a great way to declutter your home while supporting a good cause.

Retirement Contributions

Contributing to retirement accounts like a 401(k) or IRA is a smart way to save for the future and lower your taxable income. For 2024, you can contribute up to $23,000 to a 401(k) if you’re under 50, and an additional $7,500 if you’re 50 or older. If you don’t have access to a workplace retirement plan, consider a traditional IRA, where you can contribute up to $7,000 ($8,000 for those 50 and older).

Business Expenses

If you own a business or are self-employed, many of your everyday expenses can be deducted. This includes costs like office supplies, travel, and even a portion of your home expenses if you have a home office. The IRS requires that these expenses be ordinary and necessary for your business, so keep thorough records to back up your claims.

Note: Health insurance premiums are also deductible for self-employed individuals, which can be a significant saving.

Health Savings Accounts (HSAs)

HSAs offer a triple tax advantage: contributions are tax-deductible, the account grows tax-free, and withdrawals for qualified medical expenses are tax-free. In 2024, individuals can contribute up to $4,150, and families up to $8,300. If you’re 55 or older, you can make an additional $1,000 catch-up contribution.

Pro Tip: Use your HSA to pay for out-of-pocket medical expenses, and save the receipts. This way, you can reimburse yourself tax-free at any time, even years down the line.

By focusing on these deduction optimization opportunities, you can significantly reduce your taxable income and improve your financial well-being. Up next, we’ll tackle some frequently asked questions about maximizing deductions.

Frequently Asked Questions about Deduction Optimization

Is tax optimization legal?

Absolutely! Tax optimization is a legal mechanism that allows individuals and businesses to reduce their tax liabilities by leveraging the tax code’s allowances. The key is to stay within the boundaries set by the law. This involves using available deductions, credits, and other strategies to minimize taxes owed. The IRS provides clear guidelines on what is permissible, so as long as you adhere to these, you’re on solid ground.

Fact: According to the Legal Information Institute, tax optimization is not only legal but also a smart way to improve financial efficiency.

How to maximize deductions on taxes?

To maximize deductions, focus on both deductions and tax credits. While deductions reduce your taxable income, tax credits directly reduce the amount of tax you owe. Here are some strategies:

-

Itemize vs. Standard Deduction: Evaluate whether itemizing your deductions exceeds the standard deduction. This includes expenses like mortgage interest, state taxes, and charitable contributions.

-

Bunch Deductions: Consider bunching expenses into one tax year to surpass the deduction thresholds. For example, if you have medical expenses, try to schedule treatments within the same year to maximize deductibility.

-

Tax Credits: Use credits such as the child tax credit and earned income tax credit. These credits can significantly reduce your tax bill.

Tip: Keep a checklist of allowable deductions to ensure you don’t miss out on potential savings. Source: TurboTax

What is deduction in the OTC process?

In the context of accounts receivable, deduction management is crucial. It involves tracking and resolving deductions taken by customers, often due to discrepancies in billing or delivery. Effective deduction management can improve cash flow and reduce outstanding receivables.

- Accounts Receivable: This refers to the money owed to a company by its customers. Managing deductions in this process ensures that the company accurately accounts for any reductions in payment and quickly addresses any disputes.

Note: Deduction management is a part of the broader financial strategy to ensure accurate financial reporting and maintain healthy cash flow.

By understanding these aspects of deduction optimization, you can better steer the tax landscape and improve your financial strategy.

Conclusion

At Elite Tax Strategy Solutions, we believe that tax savings are not just a benefit—they are a crucial component of achieving long-term financial stability. Our mission is to guide high earners and closely held businesses through the intricate maze of the tax code, ensuring they maximize every opportunity for savings.

By offering over 100 custom tax-saving strategies, we empower our clients to not only reduce their tax liabilities but also align their tax planning with their broader financial goals. Our approach is thorough and proactive, ensuring compliance while optimizing each client’s unique financial situation.

Deduction optimization plays a pivotal role in this process. By leveraging strategic deductions and credits, we help our clients retain more of their hard-earned money. Whether it’s through charitable donations, retirement contributions, or managing business expenses, the right deductions can significantly impact your financial health.

In today’s ever-changing tax landscape, staying informed and adaptable is key. Our team of seasoned tax professionals is committed to keeping you ahead of the curve, providing expert guidance and innovative solutions.

Join us at Elite Tax Strategy Solutions and take the first step toward a more secure financial future. By embracing strategic tax planning, you can achieve not just savings, but true financial freedom.