Strategic Tax Planning for Small Businesses

When you’re running a business, every dollar counts. That’s why implementing effective small business tax savings strategies isn’t just smart—it’s essential for your company’s long-term health and profitability.

As someone who’s worked with entrepreneurs for decades, I’ve seen how the right tax approach can transform a struggling business into a thriving one. The difference often comes down to knowing which strategies align with your specific situation.

Most business owners I meet are experts in their field—whether that’s construction, consulting, or creative services—but tax planning isn’t typically their passion or strength. And that’s perfectly okay! You shouldn’t have to become a tax expert to run a successful business.

What you do need is awareness of the major opportunities to legally reduce your tax burden. The most impactful small business tax savings strategies include selecting the right business entity (S-Corporation, LLC, or C-Corporation), claiming home office deductions (which can save $1,500-$2,000 annually), and maximizing vehicle expense deductions at 67¢ per mile in 2024.

Beyond these basics, you can leverage Section 179 to write off up to $1.22 million in qualifying equipment purchases this year, contribute up to $69,000 to tax-deferred retirement accounts like SEP IRAs or Solo 401(k)s, and use Health Savings Accounts to deduct up to $8,300 for family coverage.

Effective tax planning isn’t a once-a-year scramble in April—it’s an ongoing process that should inform your business decisions throughout the year.

I’m David Fritch, and after 40+ years as both a CPA and small business owner myself, I’ve helped countless entrepreneurs implement strategies that keep more money in their pockets while staying fully compliant with tax laws. My approach focuses on practical solutions custom to your specific business needs.

The most frustrating situations I encounter are when business owners come to me after overpaying thousands in taxes simply because they weren’t aware of legitimate deductions available to them. With proper planning, those funds could have been reinvested in growing their business or saved for retirement.

Tax planning isn’t just about minimizing what you owe—it’s about creating financial stability and building wealth for the future. By understanding how your business decisions affect your tax situation, you can avoid unwelcome surprises and make choices that support your long-term goals.

Ready to learn more about specific small business tax savings strategies? Explore our resources on business expense categories, tax risk management, and tax filing assistance to deepen your understanding of how to keep more of what you earn.

Mastering Small Business Tax Savings Strategies

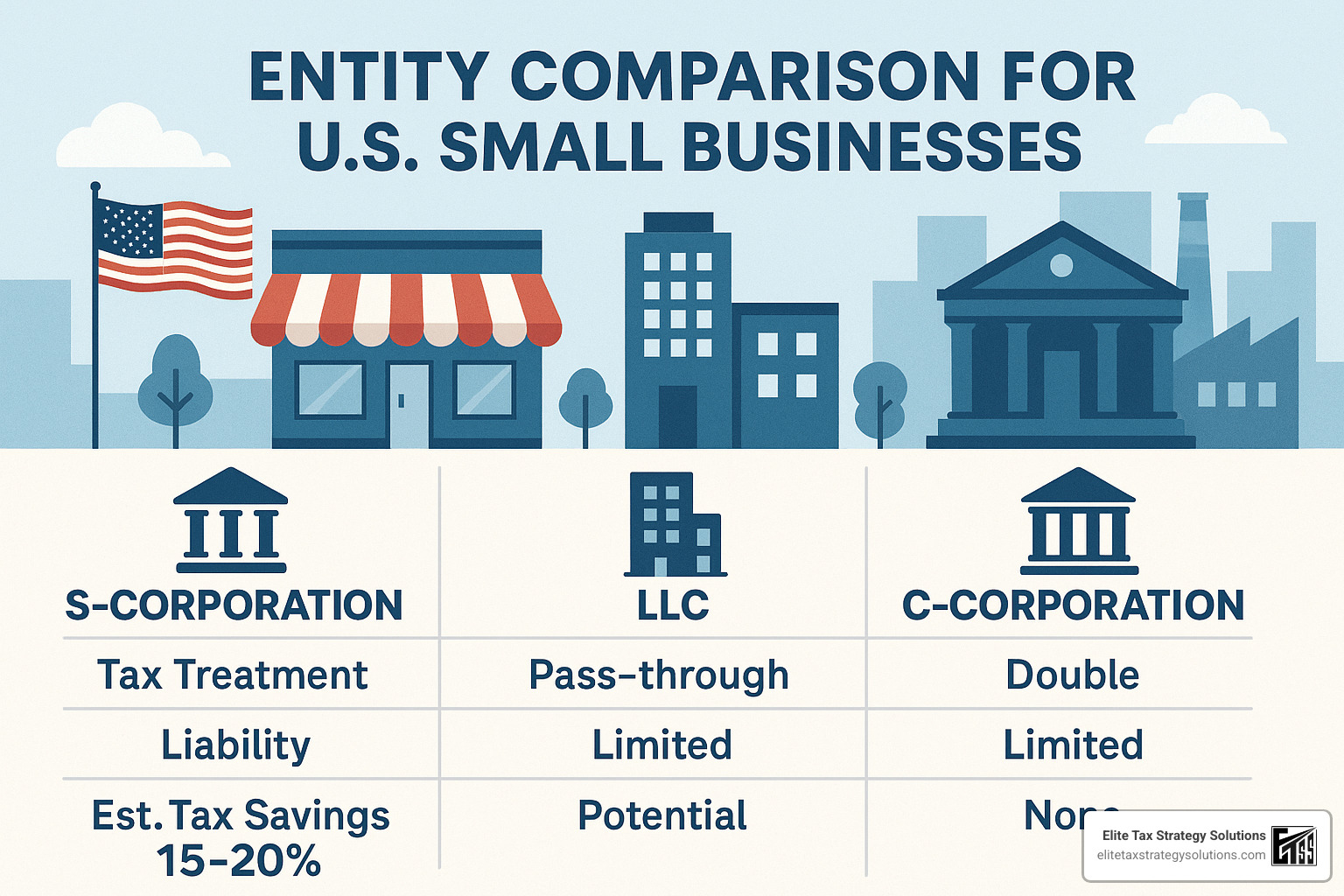

When it comes to tax planning, your choice of business entity is perhaps the most foundational decision you’ll make. This choice affects everything from your personal liability to how much you’ll pay in taxes.

Why Elect an S-Corporation?

Let me share one of the most powerful small business tax savings strategies that I’ve seen transform my clients’ tax situations: electing S-Corporation status.

Here’s the beauty of an S-Corporation: you get to wear two hats—both employee and owner. This dual role creates a significant tax advantage. You’ll pay yourself a “reasonable salary” that’s subject to employment taxes (Social Security and Medicare), but then you can take additional profits as distributions that aren’t subject to self-employment tax.

This strategy isn’t just theoretical—it typically saves business owners between $5,000 and $10,000 annually, depending on their profit levels.

Let me put this in real terms: Imagine your business nets $150,000 this year. As a sole proprietor, you’d pay self-employment tax on every dollar of that $150,000. Ouch! But as an S-Corp owner, if you pay yourself a reasonable salary of $75,000, you’d only pay employment taxes on that amount. The remaining $75,000 could be taken as distributions, saving you approximately $10,575 in self-employment taxes.

One of my clients recently told me, “Finally learned how LLCs can help protect my personal savings and how S-Corps can help me pay lower taxes.” That lightbulb moment is what we aim for with every client.

A word of caution, though: The IRS keeps a close eye on what constitutes a “reasonable” salary. Your compensation should reflect industry standards for someone in your position and location. Setting it too low is a red flag that could trigger an audit.

Pass-Through vs. C-Corp Decision Points

Since the Tax Cuts and Jobs Act lowered the corporate tax rate to a flat 21%, C-Corporation status has become more attractive for some businesses. Let’s break down what to consider:

C-Corporations shine with their flat 21% tax rate on all profits, more deductible fringe benefits, and the ability to retain earnings for growth more easily. However, they come with a significant drawback: double taxation. Your profits get taxed at the corporate level, and then shareholders pay taxes again on any dividends received. They also require more complex compliance and typically create a higher overall tax burden for businesses that distribute most of their profits.

On the flip side, pass-through entities like S-Corps, LLCs, and Partnerships offer a single layer of taxation, the valuable Qualified Business Income deduction (up to 20% of business income), and greater flexibility in allocating income and losses among owners.

The TCJA provisions are scheduled to sunset after 2025, which could significantly change this calculation. I recommend sitting down with a tax professional annually to review your entity choice, especially as your business grows and tax laws evolve.

Qualified Business Income (QBI) Deduction & Phase-outs

The Section 199A deduction, commonly called the QBI deduction, is like finding money you didn’t know you had. This valuable benefit allows eligible pass-through businesses to deduct up to 20% of their qualified business income—essentially giving you a tax break on one-fifth of your business profits.

But like many good things in the tax code, there are limits to understand:

For 2024, the deduction begins to phase out at $191,950 for single filers and $383,900 for joint filers. If you’re in a Specified Service Trade or Business (SSTB)—which includes health, law, consulting, and financial services—these limitations hit harder. And for higher-income businesses, the deduction becomes limited based on W-2 wages paid and/or qualified property owned.

To see the impact, consider a construction company with $300,000 in qualified business income. They could potentially deduct $60,000 (20% of QBI), substantially reducing their taxable income and keeping more money in the business for growth.

I’ve helped dozens of business owners restructure their operations to maximize this deduction, often finding ways to qualify even when initial review suggested they might be excluded. This is where personalized small business tax savings strategies really make a difference in your bottom line.

Home, Wheels & Gear: Big-Ticket Deduction Plays

Some of the most valuable small business tax savings strategies involve the essential big-ticket items every business needs: your workspace, transportation, and equipment. These deductions can dramatically reduce your tax bill when handled correctly.

Home Office Deduction Requirements & Myths

If you’re like many entrepreneurs who work from home, the home office deduction can put an extra $1,500 to $2,000 back in your pocket each year. But this valuable deduction comes with clear rules you need to follow:

You must have regular and exclusive use of the space for business purposes (no working from the family dining table), and it must be your principal place of business or where you regularly meet clients.

Let’s bust a common myth right away: taking a legitimate home office deduction doesn’t automatically trigger an IRS audit. As long as you’re following the rules and keeping good records, you can claim this deduction with confidence.

You have two ways to calculate your deduction:

With the Simplified Method, you’ll claim $5 per square foot (up to 300 square feet) for a maximum deduction of $1,500. It’s quick and easy, but you can’t claim depreciation or carry over unused deductions.

The Regular Method takes more record-keeping but often results in bigger savings. You’ll calculate what percentage of your home is used for business, then apply that percentage to eligible expenses like mortgage interest or rent, utilities, insurance, and repairs. You can even include depreciation.

I worked with a client who runs an online store from her home. By properly documenting her dedicated 200 square foot office (12% of her home), she saved over $2,200 using the regular method. She applied this percentage to her mortgage interest, utilities, insurance, and added depreciation for a substantial deduction.

Want more details? Check out the IRS Home Office Guide.

Two Ways to Deduct Your Business Vehicle

Your business vehicle expenses represent another significant deduction opportunity. For 2024, you have two options:

The Standard Mileage Rate gives you 67¢ per mile for business use. Just track your business miles, multiply by the rate, and you’re done. This rate covers everything—gas, insurance, maintenance, and even depreciation.

The Actual Expense Method requires more detailed record-keeping but can be worth it for newer, more expensive vehicles. You’ll track all vehicle expenses, calculate what percentage was for business use, and apply that percentage to your total expenses.

| Comparison | Standard Mileage | Actual Expenses |

|---|---|---|

| Record-keeping | Simpler (track miles only) | More complex (all expenses) |

| Best for | Lower-cost vehicles, high mileage | Newer, expensive vehicles |

| Special benefits | Can switch methods later | Accelerated depreciation options |

| 2024 rate | 67¢ per mile | Varies based on actual costs |

Here’s an insider tip about the “heavy vehicle loophole”: Vehicles weighing over 6,000 pounds qualify for more generous depreciation rules. This is why you’ll notice many business owners driving larger SUVs and trucks—they can potentially write off the entire purchase price in the first year using Section 179 expensing (limited by business-use percentage, of course).

I recently helped a landscaping business owner save over $15,000 in taxes by properly documenting his 22,000 business miles in a year. At the 2023 rate of 65.5¢ per mile, this created a $14,410 deduction that significantly reduced his tax bill.

Smart vs. Not-So-Smart Equipment Purchases

Section 179 and bonus depreciation are powerful tools that allow your business to immediately deduct equipment purchases rather than spreading the deduction over several years.

For 2024, the Section 179 limit is a generous $1.22 million (though it phases out dollar-for-dollar once you hit $3.05 million in purchases). Meanwhile, Bonus Depreciation sits at 60% for 2024—down from 80% in 2023, and continuing to decrease through 2026.

Smart equipment purchases include assets that genuinely improve your productivity or reduce costs, purchases timed to offset high-income years, and qualifying property placed in service before December 31st.

Not-so-smart equipment purchases include buying solely for tax deductions without a real business need, making large purchases that strain your cash flow, or failing to consider the declining bonus depreciation rates in your long-term planning.

As one workshop attendee shared, “The workshop provided actionable details on how to save money on taxes.”

Don’t forget that off-the-shelf software also qualifies for Section 179 expensing, making it a valuable deduction for technology-focused businesses. I’ve seen many clients save thousands by properly timing their software investments to maximize tax benefits while improving their operations.

Retirement & Health: Deferring Taxes While Building Wealth

Let’s talk about something that makes most business owners smile: strategies that cut your taxes today while building your wealth for tomorrow. These are some of my favorite small business tax savings strategies to share with clients because they deliver both immediate and long-term benefits.

Choosing the Right Small-Biz Retirement Plan

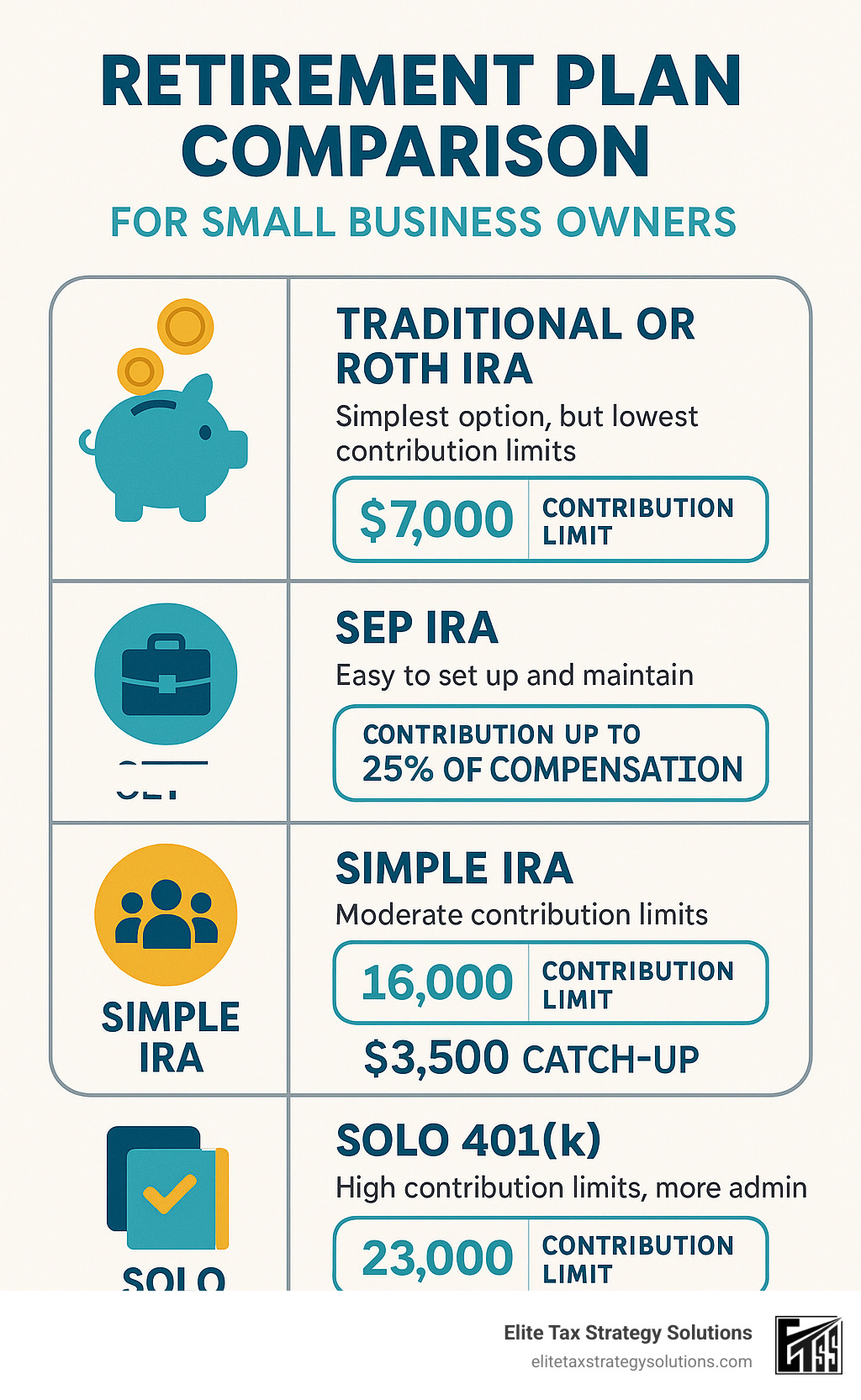

As a small business owner, you have seven different retirement plan options in your toolkit. Think of these as different vehicles that can get you to the same destination (retirement), but with different features and speed limits.

The humble Traditional or Roth IRA is like the bicycle of retirement plans – accessible to everyone, but with limited carrying capacity. With contribution limits of just $7,000 in 2024 (plus $1,000 extra if you’re 50+), it’s usually not enough for most business owners.

Moving up to a SEP IRA is like upgrading to a pickup truck. It’s still fairly simple to maintain but offers much more storage space – you can contribute up to 25% of your compensation or $69,000 (2024), whichever is less. The catch? Only you as the employer contribute, and you must cover all eligible employees at the same percentage of compensation.

The SIMPLE IRA works well for businesses with fewer than 100 employees. It’s like a minivan – practical and accommodating. Employees can contribute $16,000 (2024), plus $3,500 more if they’re 50+. As the employer, you’ll need to make either matching contributions or non-elective contributions for eligible employees, but the paperwork is much simpler than a 401(k).

For solo entrepreneurs, the Solo 401(k) is the sports car of retirement plans. With a combined limit of $69,000 (2024), you get to wear both hats – as an employee, you can contribute up to $23,000 (plus $7,500 catch-up if 50+), and as the employer, you can add up to 25% of your compensation. You can even build in loan provisions if needed.

If you’ve got employees, a Traditional 401(k) might be your SUV – more expensive to maintain but offering flexibility and comfort for everyone. It has the same contribution limits as the Solo 401(k) but comes with various vesting and matching options to help attract and retain talent.

For high-income business owners nearing retirement, a Defined Benefit Plan is like a luxury yacht – expensive to maintain but with incredible capacity. These plans can potentially allow contributions of $300,000+ annually, though they require complex administration and actuarial calculations.

The Cash Balance Plan offers a hybrid approach – think of it as a convertible that functions as both a sports car and luxury vehicle. It combines features of both defined benefit and defined contribution plans, with high contribution limits based on age and income, but more flexibility than traditional defined benefit plans.

I recently worked with a surgeon in her late 50s who was able to shelter over $200,000 in a defined benefit plan. Not only did this dramatically reduce her current tax bill, but it also turbocharged her retirement savings during her peak earning years.

Maximizing Health Savings Accounts (HSAs)

If retirement plans are the main course of tax-advantaged savings, Health Savings Accounts are the delicious dessert with a cherry on top. HSAs offer what I call the “triple tax advantage” – a rare treat in the tax world:

- Your contributions are tax-deductible

- Your investments grow tax-free

- Your withdrawals for qualified medical expenses are tax-free

For 2024, self-employed individuals can contribute $4,150 for individual coverage or $8,300 for family coverage. If you’re 55 or older, you can add another $1,000 as a catch-up contribution.

The only ticket for admission to this tax-saving party is enrollment in a high-deductible health plan (HDHP). These plans typically have lower premiums but higher deductibles, making them a good fit for many healthy business owners.

What many people don’t realize is that HSAs can be powerful retirement planning tools too. After age 65, you can withdraw funds for non-medical expenses without penalty. You’ll pay ordinary income tax on these withdrawals (similar to a traditional IRA), but you’ll have enjoyed decades of tax-free growth.

I often advise clients to max out their HSA contributions and, if possible, pay medical expenses out-of-pocket while leaving the HSA funds invested. This approach transforms your HSA into a stealth retirement account with best tax benefits.

One client followed this strategy for just five years and accumulated over $40,000 in his HSA – money that will either cover future medical expenses tax-free or supplement his retirement income after 65.

These retirement and health strategies aren’t just about saving taxes today – they’re about building financial security for tomorrow while keeping more of your hard-earned money out of Uncle Sam’s pocket.

Smart Accounting & Timing Moves

When it comes to saving on taxes, sometimes it’s not just what you do—it’s when you do it. The timing of your income and expenses can dramatically impact your tax bill, often by thousands of dollars. Let’s explore how you can use smart accounting and timing strategies to keep more money in your business.

Cash vs. Accrual—Which Saves More?

Most small business owners I work with use the cash method of accounting, and for good reason. The cash method gives you more control over your tax situation and tends to be simpler to manage.

With the cash method, you only record income when you actually receive payment, and you only record expenses when you actually pay them. This simplicity offers tremendous flexibility for year-end tax planning.

For example, if you’re having a particularly profitable year, you might delay sending December invoices until January, pushing that income into the next tax year. Or you might accelerate expenses by buying supplies in December rather than waiting until January.

The accrual method, on the other hand, records income when it’s earned and expenses when they’re incurred—regardless of when money changes hands. While this gives you a more accurate picture of your business performance, it offers less flexibility for tax planning.

Good news for small businesses: Even if you have inventory, you may still qualify to use the cash method if your average annual gross receipts for the past three years don’t exceed $27 million. This is a significant advantage created by the Tax Cuts and Jobs Act.

If you want to change your accounting method, you’ll need to file Form 3115 with the IRS. It requires some paperwork, but the tax planning flexibility can save you significant money over time.

Year-End Income Shifts & Expense Acceleration

One of my favorite small business tax savings strategies involves careful timing of income and expenses before December 31st. These moves can sometimes reduce your current year’s tax bill by thousands.

To defer income (if you’re a cash-basis taxpayer), consider:

– Waiting until late December to send invoices, knowing payment likely won’t arrive until January

– Scheduling service completion for January instead of December

– Delaying year-end bonuses to yourself until January (if you’re an S-corporation owner)

If you’re on the accrual basis, you can still defer certain income using the 12-month rule for advance payments, which allows you to postpone recognition of some prepayments until the following tax year.

To accelerate expenses before year-end, think about:

– Prepaying up to 12 months of expenses like rent, insurance, or professional subscriptions

– Stocking up on office supplies, materials, or other necessities

– Paying employee bonuses before December 31

– Making planned charitable contributions

– Purchasing needed equipment that qualifies for Section 179 expensing

I recently worked with a retail client who saved over $4,000 in taxes by strategically accelerating $15,000 in expenses into December and delaying $10,000 in income until January. These weren’t artificial moves—they were legitimate business transactions that we simply timed strategically.

Don’t forget about bad debt write-offs before year-end. If you have customers who simply aren’t going to pay, you can potentially write off these uncollectible accounts. Just be sure to document your collection attempts and formally recognize the debt as uncollectible in your accounting records.

The 12-month rule is particularly helpful—it allows you to deduct expenses you’ve paid in advance as long as the benefit period doesn’t extend more than 12 months beyond payment. This means you could prepay your office rent in December for the entire next year and deduct it all in the current year.

“Most helpful training I’ve ever been to! The instructor provided valuable information clearly, no fluff – all practical and doable.” – Workshop attendee

These timing strategies work best when they align with your actual business operations. The IRS may scrutinize transactions that appear to have no business purpose beyond tax avoidance. The key is to make smart business decisions that also happen to be tax-efficient.

Compliance, Credits & Avoiding Costly Penalties

Let’s face it—nobody gets excited about tax compliance, but understanding this area can actually put money back in your pocket. While deductions are great for trimming your taxable income, tax credits are even better because they reduce your tax bill dollar-for-dollar. Think of credits as the VIP pass of the tax world!

Key Federal, State (WA) & Local Taxes to Track

As a small business owner, you’re juggling multiple layers of taxation, which can sometimes feel like spinning plates. Here’s what you need to keep an eye on:

At the federal level, you’re dealing with income tax (which varies depending on whether you’re an S-Corp, LLC, or other entity type), self-employment tax (that hefty 15.3% that sole proprietors and partners face), employment taxes if you have team members, and possibly excise taxes for certain industries.

Here in Washington State, we have our own unique tax structure. Instead of income tax, businesses face the Business & Occupation (B&O) tax based on your gross receipts. You’ll also need to collect and remit sales tax, pay use tax on out-of-state purchases, and handle employment taxes for your team.

Don’t forget about local taxes! Many Washington cities have their own B&O taxes, plus there are property taxes and special assessments that vary by location.

One of my clients, a coffee shop owner in Seattle, was surprised to find she was subject to four different B&O tax classifications for different parts of her business. Getting this right saved her from potential penalties and back taxes.

Staying Ahead of Deadlines & 1099/W-2 Penalties

Missing tax deadlines is like missing a flight—it’s stressful and expensive. Here are the key dates to mark in your calendar:

Your estimated tax payments are due quarterly on April 15, June 15, September 15, and January 15. W-2s and 1099s must be submitted by January 31. Partnership and S-Corporation returns are due March 15, while C-Corporation and individual returns are due April 15.

The penalties for missing these deadlines can be painful. Failing to file 1099s will cost you $290 per form in 2024. The same penalty applies if you don’t provide W-2s to employees on time. And if the IRS determines you intentionally disregarded these requirements? That penalty doubles to $580 per form.

I recommend using electronic filing whenever possible—EFTPS for federal tax deposits and e-file for returns. Not only does this help ensure timely compliance, but it also provides confirmation that you’ve filed, which can be a lifesaver if questions arise later.

Under-Used Credits Every Small Business Should Check

Here’s where many business owners leave money on the table. These small business tax savings strategies involving credits are often overlooked but can be incredibly valuable:

The Research & Development (R&D) Credit isn’t just for scientists in lab coats. If you’re developing new products, processes, or software, you might qualify. This credit can offset your income tax or even payroll tax for startups. One manufacturing client saved over $45,000 by claiming this credit for process improvements they’d been making for years!

Energy Efficiency Credits are worth exploring if you’ve upgraded your commercial building with energy-efficient improvements, installed electric vehicle charging stations, or invested in solar or renewable energy systems.

The Work Opportunity Tax Credit can cover up to 40% of first-year wages when you hire from certain targeted groups, including veterans and the long-term unemployed. This is both good for society and your bottom line.

If you’re just starting a retirement plan, don’t miss the Retirement Plan Startup Credit. It covers 50% of costs to establish and administer a qualified plan (up to $5,000 per year for three years), with an additional credit if you include automatic enrollment.

Many states now offer Pass-Through Entity (PTE) Tax Elections, creating a workaround for the $10,000 SALT deduction cap. This can result in significant federal tax savings for many business owners.

Want to learn more about these credits and other small business tax savings strategies? Consider attending a SCORE workshop on tax savings where you can get personalized advice.

Being compliant doesn’t just help you avoid penalties—it often opens doors to credits and deductions you might otherwise miss. At Elite Tax Strategy Solutions, we believe in turning tax compliance from a burden into an opportunity for savings.

Frequently Asked Questions About Small Business Tax Savings Strategies

What counts as a deductible business expense—and what doesn’t?

When I sit down with new clients, this is often their first question. The IRS uses two main criteria for business deductions: they must be both ordinary (common in your industry) and necessary (helpful for your business).

Think of it this way—if the expense helps you make money in your business, it’s probably deductible. Office rent, employee wages, business insurance, and marketing costs all clearly fall into this category.

Most business owners are surprised to learn that business meals are still 50% deductible (though sadly, entertainment expenses generally aren’t). And yes, that business education course that helps you serve clients better? That’s deductible too.

What trips up many entrepreneurs is the gray area between business and personal. Your daily commute to your office isn’t deductible, but travel between client sites is. That new suit for client meetings? Generally not deductible, even though it feels like a business expense.

The most important thing is keeping business and personal finances separate. I’ve seen too many audit nightmares begin with commingled funds in a single checking account. A dedicated business account and credit card will save you countless headaches.

How do I know if I’m self-employed, an independent contractor, or a statutory employee?

Your classification matters tremendously for small business tax savings strategies because it determines which forms you’ll file and which deductions you can claim.

If you’re running your own business and calling the shots, you’re self-employed (or a sole proprietor). You’ll report everything on Schedule C, pay that double-whammy of self-employment tax (both the employer and employee portions of Social Security and Medicare), but you’ll be eligible for that valuable QBI deduction we discussed earlier.

As an independent contractor, you’re essentially self-employed, but you’re providing services to other businesses. The key distinction is that while you might have clients or customers, they don’t control how you perform your work. You’ll receive 1099-NEC forms instead of W-2s, and you’ll file taxes just like someone who’s self-employed.

The statutory employee category confuses everyone. You’re in this somewhat rare middle ground where your employer withholds Social Security and Medicare taxes (you’ll see the “Statutory Employee” box checked on your W-2), but you can still deduct business expenses on Schedule C. Delivery drivers, life insurance agents, and certain traveling salespeople often fall into this category.

The IRS actually has a 20-factor test to determine worker classification, and getting it wrong can be costly. I’ve seen businesses hit with five-figure penalties for misclassifying employees as contractors. When in doubt, it’s worth consulting a tax professional.

When are quarterly estimated taxes due, and what happens if I miss a payment?

The quarterly estimated tax schedule trips up even experienced business owners because the quarters aren’t equal:

First quarter payment: April 15

Second quarter payment: June 15 (just two months later!)

Third quarter payment: September 15

Fourth quarter payment: January 15 of the following year

To avoid penalties, you need to pay in the smaller of:

– 90% of your current year tax liability, or

– 100% of your previous year’s tax (which jumps to 110% if your AGI was over $150,000)

Missing a payment doesn’t mean immediate disaster, but it will cost you. The IRS charges a penalty based on the federal short-term rate plus 3 percentage points, applied to whatever you underpaid for however long it remains unpaid.

I had a client who completely missed two quarters during a chaotic year of business growth. We requested penalty abatement for reasonable cause, explaining the circumstances, and the IRS granted it. Another option is using Form 2210 to show that your income came in unevenly throughout the year (especially helpful for seasonal businesses).

The best approach? Set calendar reminders well before each due date and keep a separate savings account where you deposit a portion of each payment you receive. When the quarterly deadline arrives, you’ll be prepared rather than panicked.

These quarterly payments aren’t just a bureaucratic headache—they’re actually designed to put you on equal footing with employees who have taxes withheld from every paycheck. Think of them as your way of “paying as you go” rather than facing a massive bill in April.

Conclusion

Implementing effective small business tax savings strategies isn’t a once-a-year scramble—it’s a year-round commitment that pays dividends in both immediate savings and long-term financial stability. At Elite Tax Strategy Solutions, we’ve seen how proactive planning transforms the financial trajectory of small businesses in Jasper, Indiana and surrounding suburban areas.

Think of tax planning as preventive medicine for your business’s financial health. Just as you wouldn’t wait until you’re seriously ill to see a doctor, you shouldn’t wait until tax season to think about tax strategies. The most powerful tax-saving opportunities often disappear once the calendar year ends.

Our comprehensive approach starts with understanding your unique business situation and goals. We help you steer the complexities of the tax code through:

- Entity optimization that could save thousands in self-employment taxes

- Strategic timing of income and expenses to minimize your tax burden

- Identification of overlooked deductions and credits that directly reduce what you owe

- Retirement and benefits planning that builds wealth while reducing taxes

- Documentation practices that protect you in case of an audit

I remember working with a construction company owner who came to us frustrated after years of significant tax bills. By restructuring his business as an S-Corporation, implementing a targeted retirement plan, and properly documenting his vehicle expenses, we reduced his tax burden by over $22,000 in the first year alone. More importantly, he gained peace of mind knowing he had a sustainable tax strategy aligned with his business goals.

The tax code is a labyrinth of rules that changes constantly. What worked last year might not be optimal this year. That’s why we emphasize building a relationship with our clients that extends beyond tax season—we want to be your first call when you’re making important business decisions that have tax implications.

You’ve worked too hard building your business to leave money on the table at tax time. Whether you’re just starting out or have been in business for decades, a personalized tax roadmap can help ensure more of your hard-earned money stays where it belongs—with you and your business.

For more information about our comprehensive tax planning services and how we can help you implement these small business tax savings strategies in your specific situation, visit Elite Tax Strategy Solutions.

In taxes, being proactive isn’t just smart—it’s profitable.